[Trumps] package will make Australia even less attractive as a destination for such investment, which is bad news for business and jobs on this side of the Pacific, as the Business Council of Australia warned yesterday. That’s why our political class, especially Bill Shorten and his frontbench, whose “big taxing, big spending” class warfare mindset belongs to the less competitive world of a half-century ago, needs to start taking tax reform, especially corporate tax reform, seriously. The US remains by far the largest business investor in Australia, accounting for 27 per cent ($860 billion) of incoming investment last year, followed by Britain (16 per cent). Hong Kong ranked fifth place and China seventh. About 28 per cent of outbound investment from Australia went to the US. Nations such as France also are cutting their business taxes. Every such reduction, as BCA executive Jennifer Westacott said, was “a de facto tax increase in Australia and a disincentive for investors”.

In May, in his budget reply speech, the Opposition Leader could barely conceal his disdain for those who generated wealth and jobs, dismissing the Turnbull government’s vital corporate tax cut plan as “a $65bn giveaway for big business”. In maintaining that view, as opposition Treasury spokesman Chris Bowen did yesterday, Labor is disowning the legacy of the Hawke-Keating years when the then party of reform cut the company tax rate from 49 per cent to 33 per cent to boost incentive. It positioned the nation for decades of growth.

Amazingly, Robert Gottliebsen, of all people, has talked more sense in a separate article published today in The Australian:

As for Australia’s response, there will be the usual cries for lower company taxes but most of the arguments, like those from the Business Council, have been badly thought out.

Because of dividend imputation Australia’s tax rates are not that far above the US but they are much higher for overseas investors who don’t benefit from imputation. Any measures Australia takes needs to take into account imputation…

Gotti has touched on a vital issue that the Australian’s Editorial, the BCA, and the Turnbull Government never seems to address: that cutting Australia’s company tax rate to 25% from 30% would benefit foreign owners/shareholders, while leaving Australians worse-off.

Local owners of unincorporated businesses are essentially taxed at their personal tax rate, because of dividend imputation. Hence, lowering the company tax rate would provide local owners and shareholders with minimal benefits, since any reduction in company taxes would be offset by a commensurate reduction in imputation credits.

Therefore, the major beneficiaries from company tax cuts are foreign-owned corporations (or foreign investors) that are not subject to Australia’s dividend imputation system. For these foreign-owned business there would be no offset in the form of lower franking credits, therefore, a company tax cut would represent a financial windfall gift from Australian tax payers.

Former Treasurer and Prime Minister, Paul Keating, explained it best when he penned the following last year:

“Australia’s dividend imputation system works such that the company tax is, in effect, a withholding tax – a tax temporarily held by the Commonwealth which is returned to shareholders when their dividends are paid. So, whether the company tax is withheld by the Commonwealth at a rate of 30% or 25% is immaterial – the Commonwealth is going to return the money to shareholders anyway, regardless of the rate. But the shareholders who will receive a benefit are foreign shareholders”.

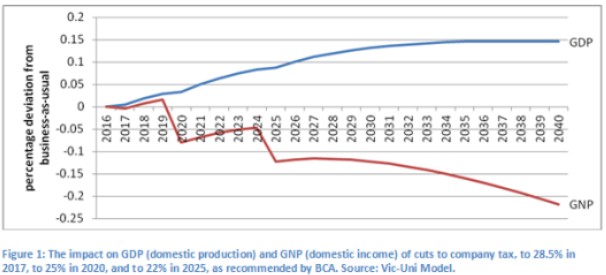

For this reason, modelling from Victoria University senior research fellow, Janine Dixon, found that cutting the company tax rate would actually lower national income (GNP) and living standards because of the benefits flowing offshore:

Paul Keating has also previously hit back hard when newspaper editorials like the one above try to claim that “Labor is disowning the legacy of the Hawke-Keating years when the then party of reform cut the company tax rate from 49 per cent to 33 per cent to boost incentive”. Here’s Keating taking The AFR to task last year for using a similar line of attack:

“Yes, I did cut the company tax rate from 49 per cent to 33 per cent but paid for those vast reductions by a massive broadening to the base of the tax system: capital gains taxation at full marginal rates, a comprehensive fringe benefits tax, the abolition of entertainment as a deduction, tax on company cars etc.

Tax reductions are desirable provided they are affordable. But I would never have countenanced a $50 billion impost on the budget balance with a discretionary unfunded tax cut.

The AFR has embarked upon this campaign in collusion with the Business Council of Australia, in the council’s camouflaged attempt to reduce the rate of company tax on foreign shareholdings. The AFR must be alone among national financial newspapers in urging so massive an impost on the national fiscal balance”.

Ultimately, there is one threshold issue that needs to be overcome in deciding whether to cut Australia’s company tax rate to 25% from 30%:

Would cutting company taxes generate enough investment, jobs and growth to justify the estimated $8.2 billion cost to the Budget each and every year, and are there better uses of scarce taxpayer money?

The Treasury’s own modelling has shown almost zero impact on either jobs or growth. Moreover, as Janine Dixon’s modelling above showed, there is the very real prospect that Australian national income could be reduced from cutting company taxes.

Regarding the second part of the question, there are plenty of better policy alternatives, including using some or all of the funds that would be spent on cutting company taxes to:

- undertaking critical infrastructure investment and restoring Australia’s dilapidated infrastructure stock;

- using direct measures to spur business investment, such as accelerated depreciation allowances, investment allowances, or some other measures; or

- boosting spending on education.

Any of these measures are likely to generate bigger pay-offs to the resident population than the Coalition’s clumsy plan to slash the company tax rate, which would merely gift billions of dollars to foreign owners/shareholders in the blind hope that they may increase investment.