Economic Outlook Improves But Rates Should Stay on Hold

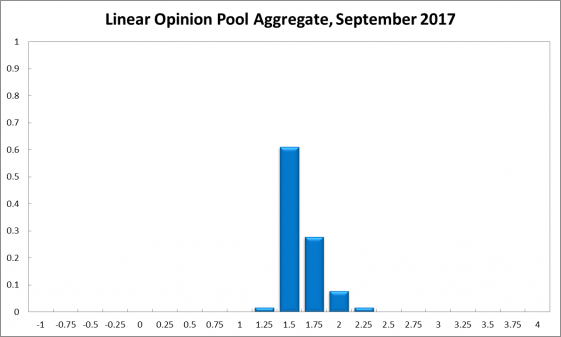

Solid employment figures, growing business confidence, and a brightening of the global economy suggest a slightly improved outlook for the Australian economy. The RBA Shadow Board continues to advocate a hold-and-wait policy. It attaches a 61% probability that this is the appropriate setting. The confidence attached to a required rate cut equals 2%, while the confidence in a required rate hike equals 37%.

Australia’s seasonally adjusted unemployment rate, at 5.6%, according to the Australian Bureau of Statistics, remains comparatively low, with the economy adding net 27,900 jobs but losing 20,300 full-time positions. The labour force participation rate rose slightly, for the fifth consecutive month, to 65.1%. On the surface, these numbers point to a tightening of the labour market, which may indicate inflationary pressures building slowly. On the other hand, the high rate of youth unemployment as well as part-time employment are signs of underemployment, which contains any inflationary pressures. This tension makes it hard to predict the implications of the labour market for inflation.

The Aussie dollar, relative to the US dollar, after strengthening in the previous month, has stabilised around 79 US¢ this month. Likewise, yields on Australian 10-year government bonds are largely unchanged, remaining just below 2.7%, and domestic share prices remain range-bound, with the S&P/ASX 200 stock index’s last reading at 5715.

The outlook for the global economy is improving, with US GDP growth revised up to 3% and Eurozone economic confidence measures hitting pre-crisis highs. The strengthening of demand on both sides of the Atlantic is also reflected in higher inflation rates there: Eurozone inflation rose to 1.5% and US inflation to 1.7%. Global share markets continue to trade near all-time highs. Taken together, these data may bode well for the health of the global economy but there is also a risk much of the demand, especially for assets, is debt-fuelled and unsustainable. Economic indicators for China paint a conflicting picture, with growth in the manufacturing sector gathering pace and in the service sector slowing. Australia continues to export more goods and services than it is importing, although the gap narrowed due to an unexpected increase in imports. The largest imminent risk on the global stage are the political tensions between the US and North Korea.

Business confidence are strengthening; both the services PMI and the manufacturing PMI improving markedly in July and August, respectively. Capacity utilization increased slightly but remains close to its long-run average, as di consumer confidence, which weakened marginally. The AIG/Housing Industry Association Performance of Construction Index jumped to 60.5, the highest reading since the indicator’s inception in 2005, yet building permits declined by 1.7% in the same period.

The Shadow Board’s policy preferences remain stable. It is 61% confident that keeping interest rates on hold is the appropriate policy, one percentage point up from August. It continues to attach a probability of 2% that a rate cut is appropriate and a 37% probability (38% in August) that a rate rise, to 1.75% or higher, is appropriate.

The probabilities at longer horizons are as follows: 6 months out, the estimated probability that the cash rate should remain at 1.50% equals 24%, one percentage point lower than in August. The estimated need for an interest rate decrease is 7% (unchanged), while the probability attached to a required increase equals 69% (68% in August). A year out, the Shadow Board members’ confidence that the cash rate should be held steady equals 16% (unchanged), while the confidence in a required cash rate decrease equals 9% (unchanged), and in a required cash rate 76% (unchanged).

No mention of house prices? That would also necessitate mentioning macroprudential which the shadow will not do under any circumstances!

Today’s meet is a no-brainer hold, no doubt with the happy idiot driving up the dollar.

David Llewellyn-Smith is Chief Strategist at the MB Fund and MB Super. David is the founding publisher and editor of MacroBusiness and was the founding publisher and global economy editor of The Diplomat, the Asia Pacific’s leading geo-politics and economics portal.

He is also a former gold trader and economic commentator at The Sydney Morning Herald, The Age, the ABC and Business Spectator. He is the co-author of The Great Crash of 2008 with Ross Garnaut and was the editor of the second Garnaut Climate Change Review.