Via the AFR:

The commitments made by the three LNG exporters that they will make enough gas available to fill the shortfall identified for 2018 are clearly welcome: Government, gas producers and buyers all agree.

But the producers will still be demanding a price that makes commercial sense. And they have privately made it clear that will not be at the prices deemed by the competition regulator as reasonable.

Therein lies the heart of the problem. Today’s price offers for gas to industrial customers of $10-$16 a gigajoule are a world away from the “benchmark prices” quoted by the Australian Competition and Consumer Commission of $5.87 in Queensland and $7.77 in Victoria.

In reality, prices much closer to the $10 mark are probably the best major Victorian manufacturers can expect, with smaller users a little higher.

LNG sources in Queensland quote about $6 a gigajoule for a marginal cost price from the “dry” – and so expensive – gas extracted from coal seam gas seams in the state, which has become the dominant source of available gas on the east coast.

When up to $3.50 a GJ of transportation costs to the south are added, the total still looks out of reach of some manufacturers.

…Industry sources point out that the regulator’s benchmark prices should in any case be based against the LNG contract market in Asia, where prices are indexed to crude oil and are several dollars higher than in the cheap, oversupplied spot market.

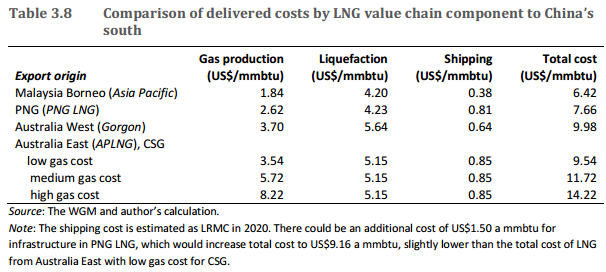

Here’s what it costs to extract gas in QLD, via BREE estimates for APLNG (the cheapest of the three):

Notice that most of the cost is in building the white elephant plant and shipping not extraction. Even for extraction, these are all-in costs, that included construction of pipelines and other infrastructure which is sunk cost and much of it already written off. The marginal cost to extract the gas today is more $1Gj. The cartel can definitely do an awful lot better than $6Gj.

The transport cost from QLD south should not always be $3.50 either. $2 is a more likely average. This is why producers could happily sell gas in the south for $3 in the past.

The ACCC prices were basically export net-back:

The ACCC has determined appropriate benchmark prices against which to assess current domestic prices and prices being offered to C&I users. These benchmark prices, based on international LNG spot prices, are $5.87/GJ in Queensland and up to $7.77/GJ in the rest of the east coast. This latter price takes into account the cost of transporting gas from Queensland to users in the south, as some domestic gas buyers in the south now have to rely on contracting with the Queensland LNG producers to meet their needs.

Today’s regional oil contract price with Brent at $57.30 is $8.40Gj

Subtract the shipping costs and we’re in the ball park.

But should we be aiming at export net-back? Why aren’t we reserving enough gas such that we are well below export net-back to preserve our cheap energy advantage. It would still only be reserving 4-5% of our total export gas. That’s what the US and pretty much every other oil and gas producer does. Do you think that Saudis pay the same price as you do to fill the petrol tank?

Do-nothing Malcolm had aimed at minimal returns on his policy and missed even those.