By Martin North, cross-posted from the Digital Finance Analytics Blog:

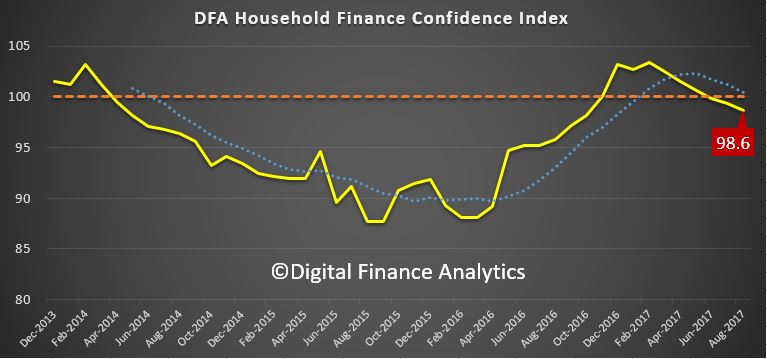

Digital Finance Analytics has released the August 2017 edition of our Household Finance Confidence index, which uses data from our 52,000 household surveys and Core Market Model to examine trends over time. Overall, households scored 98.6, compared with 99.3 last month, and this continues the drift below the neutral measure of 100. This is an average score, and there are significant variations within our various segments.

Watch the video to learn more, or read the transcript below:

Watch the video to learn more, or read the transcript below:

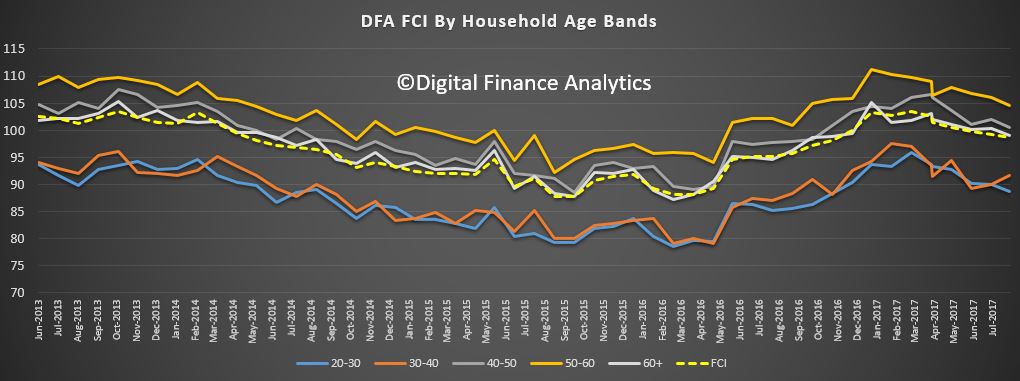

Younger households are overall less confident about their financial status, whilst those in the 50-60 years age bands are most confident. This is directly linked to the financial assets held, including property and other investments, and relative incomes. Households over 60 years track quite closely to the national averages.

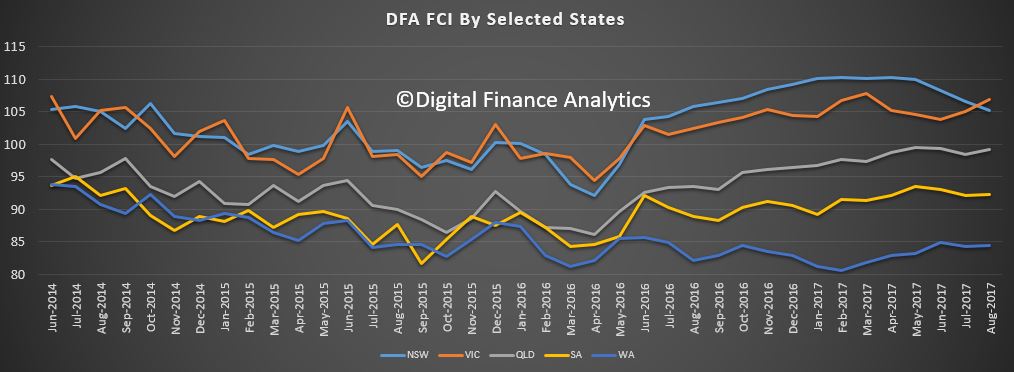

For the first time in more than a year, households in Victoria are more confident than those in NSW, while there was little relative change across the other states. One of the main reasons for the change in NSW can be traced directly to the state of the Investment Property sector, where we see a significant fall in the number of households intending to purchase in NSW, and more intending to sell. One significant observation is the rising number of investors selling in Sydney to lock in capital growth, and seeking to buy in regional areas or interstate. Adelaide is a particular area of interest.

For the first time in more than a year, households in Victoria are more confident than those in NSW, while there was little relative change across the other states. One of the main reasons for the change in NSW can be traced directly to the state of the Investment Property sector, where we see a significant fall in the number of households intending to purchase in NSW, and more intending to sell. One significant observation is the rising number of investors selling in Sydney to lock in capital growth, and seeking to buy in regional areas or interstate. Adelaide is a particular area of interest.

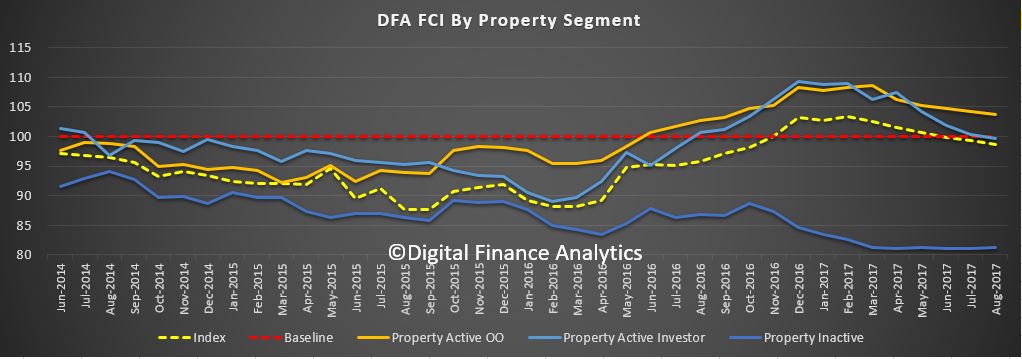

Consistent with our earlier analysis, a household’s property owing status has a significant impact on their relative financial confidence, with owner occupied households the most confident, ahead of property investors and those renting. That said, low rental growth rates mean more investors are underwater on a cash flow basis, especially in Victoria, where more than half are not covering the borrowing costs of their investment mortgage from rental receipts (but are still hopeful of capital gains, and they can offset the losses thanks to tax breaks). Actually returns are much stronger in QLD and TAS.

Consistent with our earlier analysis, a household’s property owing status has a significant impact on their relative financial confidence, with owner occupied households the most confident, ahead of property investors and those renting. That said, low rental growth rates mean more investors are underwater on a cash flow basis, especially in Victoria, where more than half are not covering the borrowing costs of their investment mortgage from rental receipts (but are still hopeful of capital gains, and they can offset the losses thanks to tax breaks). Actually returns are much stronger in QLD and TAS.

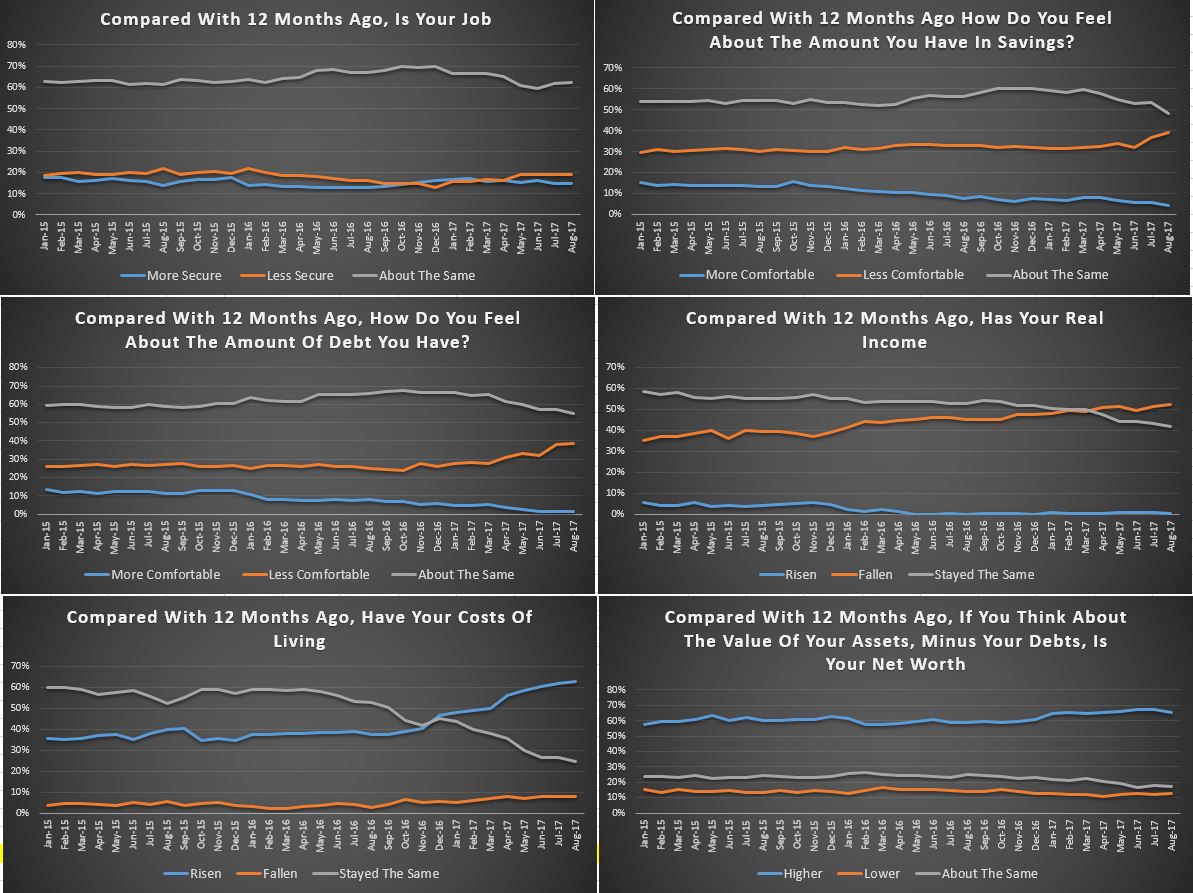

Looking at the scorecard, job security remained about the same this month, but there was a 1.7% fall in those more comfortable with their savings and a rise of 2.5% of those less comfortable – thanks to lower interest rates on deposits as banks seek to build margin. The debt burden remained a concern, with a small rise in those worried about meeting repayments on outstanding loans. Incomes are still under pressure, with more saying their incomes in real terms have been devalued, down 1%, to 52% of households. Costs of living continue to rise for 63% of households, and only 7% saw a fall. 65% of households said their overall net worth rose again, thanks mainly, to home prices rising. Some in WA, QLD and WA reported a fall, directly due to house values continuing to slip.

Looking at the scorecard, job security remained about the same this month, but there was a 1.7% fall in those more comfortable with their savings and a rise of 2.5% of those less comfortable – thanks to lower interest rates on deposits as banks seek to build margin. The debt burden remained a concern, with a small rise in those worried about meeting repayments on outstanding loans. Incomes are still under pressure, with more saying their incomes in real terms have been devalued, down 1%, to 52% of households. Costs of living continue to rise for 63% of households, and only 7% saw a fall. 65% of households said their overall net worth rose again, thanks mainly, to home prices rising. Some in WA, QLD and WA reported a fall, directly due to house values continuing to slip.

Given the fact that the dynamics of the economy seem to be locked in place with lower income growth, rising costs of living, and the property market adjusting to the new regulatory environment, we expect confidence to continue to drift lower in the months ahead. There is no obvious circuit breaker available in the current low interest rate, low growth environment. The leading indicators suggest that the recent positive momentum in the property market may be short lived.

Given the fact that the dynamics of the economy seem to be locked in place with lower income growth, rising costs of living, and the property market adjusting to the new regulatory environment, we expect confidence to continue to drift lower in the months ahead. There is no obvious circuit breaker available in the current low interest rate, low growth environment. The leading indicators suggest that the recent positive momentum in the property market may be short lived.

By way of background, these results are derived from our household surveys, averaged across Australia. We have 52,000 households in our sample at any one time. We include detailed questions covering various aspects of a household’s financial footprint. The index measures how households are feeling about their financial health. To calculate the index we ask questions which cover a number of different dimensions. We start by asking households how confident they are feeling about their job security, whether their real income has risen or fallen in the past year, their view on their costs of living over the same period, whether they have increased their loans and other outstanding debts including credit cards and whether they are saving more than last year. Finally we ask about their overall change in net worth over the past 12 months – by net worth we mean net assets less outstanding debts.

We will update the results again next month.