Via the AFR comes Franklin Templeton Investments head of equities Stephen Dover:

Around 30 per cent of the Aussie sharemarket is foreign-owned. That may sound like a lot, but it’s low for a developed market, Dover says. And what gives us our home bias also makes our sharemarket less attractive to foreigners.

Between the preferential tax treatment of our compulsory superannuation system and our dividend franking credit scheme, “the same stream of earnings [from an ASX-listed company] is more valuable to an Australian investor than it is to foreign investors – and that is unusual,” Dover explains.

“That makes Australian equities more expensive relative to equities in other markets, so it makes it less favourable to foreign investors.”

That’s the structural reason. The more cyclical one is that from a perch in New York, London or Frankfurt, Australia’s strong reliance on China is something to worry about.

And it’s not just the obvious mining link – as well all know, China is a massive consumer of our iron ore and coal, as well as many other natural resources. There’s also a link through the other major component of the ASX: the major banks.

“There is a lot of [Chinese] investing in Australian real estate, so there’s a strong correlation there,” Dover says.

In other words, the prospects of around 50 per cent of the ASX by market capitalisation hinges on China’s capacity to keep growing.

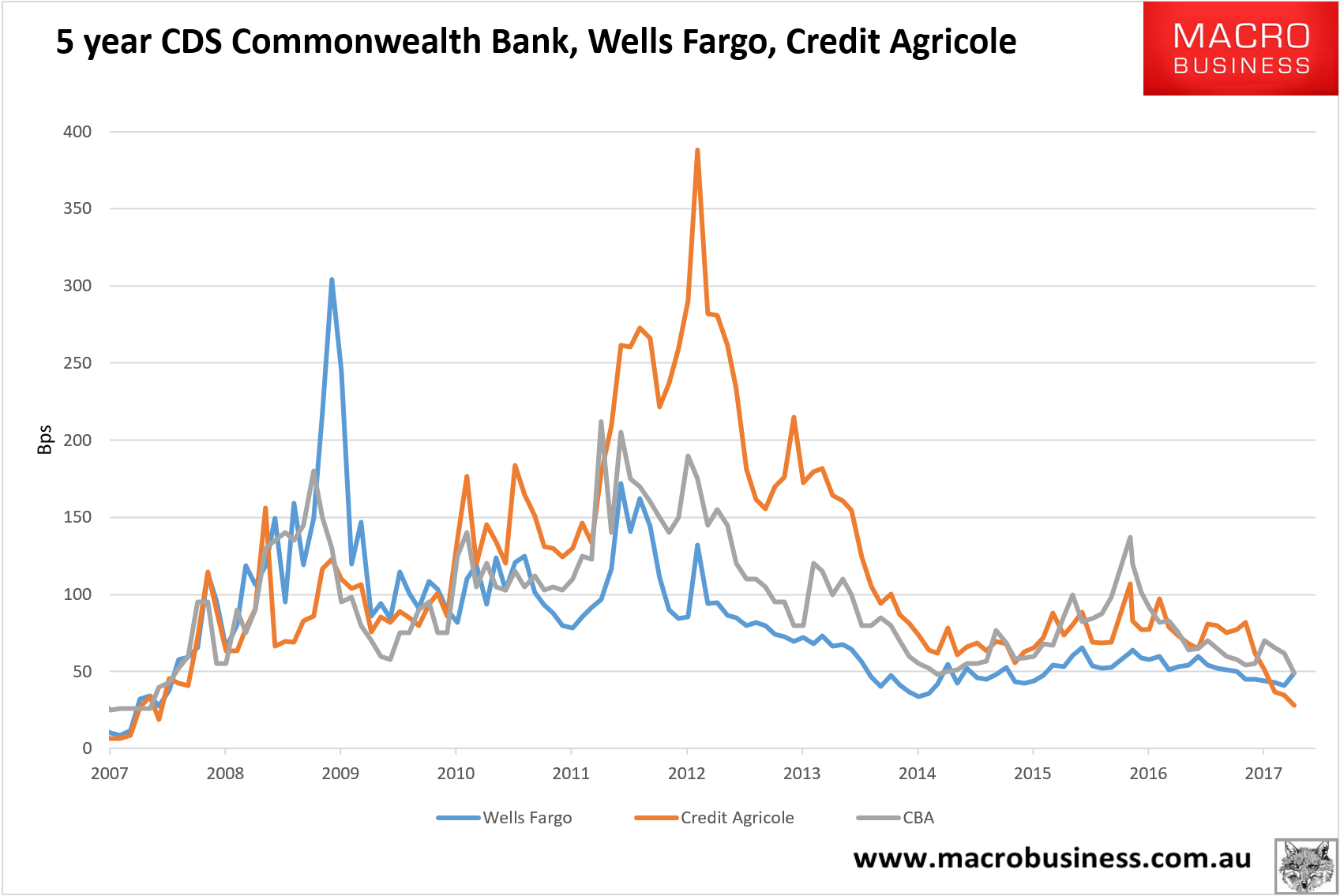

It’s worse than that, I’m afraid. The link between mining and banks also transpires via the sovereign which guarantees the bank’s offshore borrowing. When commodity prices fall so does the stability of the sovereign rating. That means that if China hits trouble there’s also a transmission mechanism to house prices via more expensive credit at the worst possible time, especially if you’re central bank has almost run out of rate cuts to absorb the higher bank funding costs.

We had a dry run of this last year when iron ore was crashing and bank funding costs soared:

Anyways, I don’t blame the fundies that hate the place, I hate it too, and think of the Aussie dollar as the best friend of every Australian investor given it will act as a natural hedge for any offshore share portfolio as China sinks.

————————————

David Llewellyn-smith is Chief Strategist at the MacroBusiness Fund which is currently allocated 70% offshore. The MacroBusiness Fund has been put together to help readers of the blog take advantage of its themes and put the power of MacroBusiness to work in their portfolio. To find out more click here.