I don’t agree very often with Deutsche’s Tim Baker but today he has nailed my views beautifully:

In the wake of reporting season, and following a raft of macro developments, we revisit our strategy views:

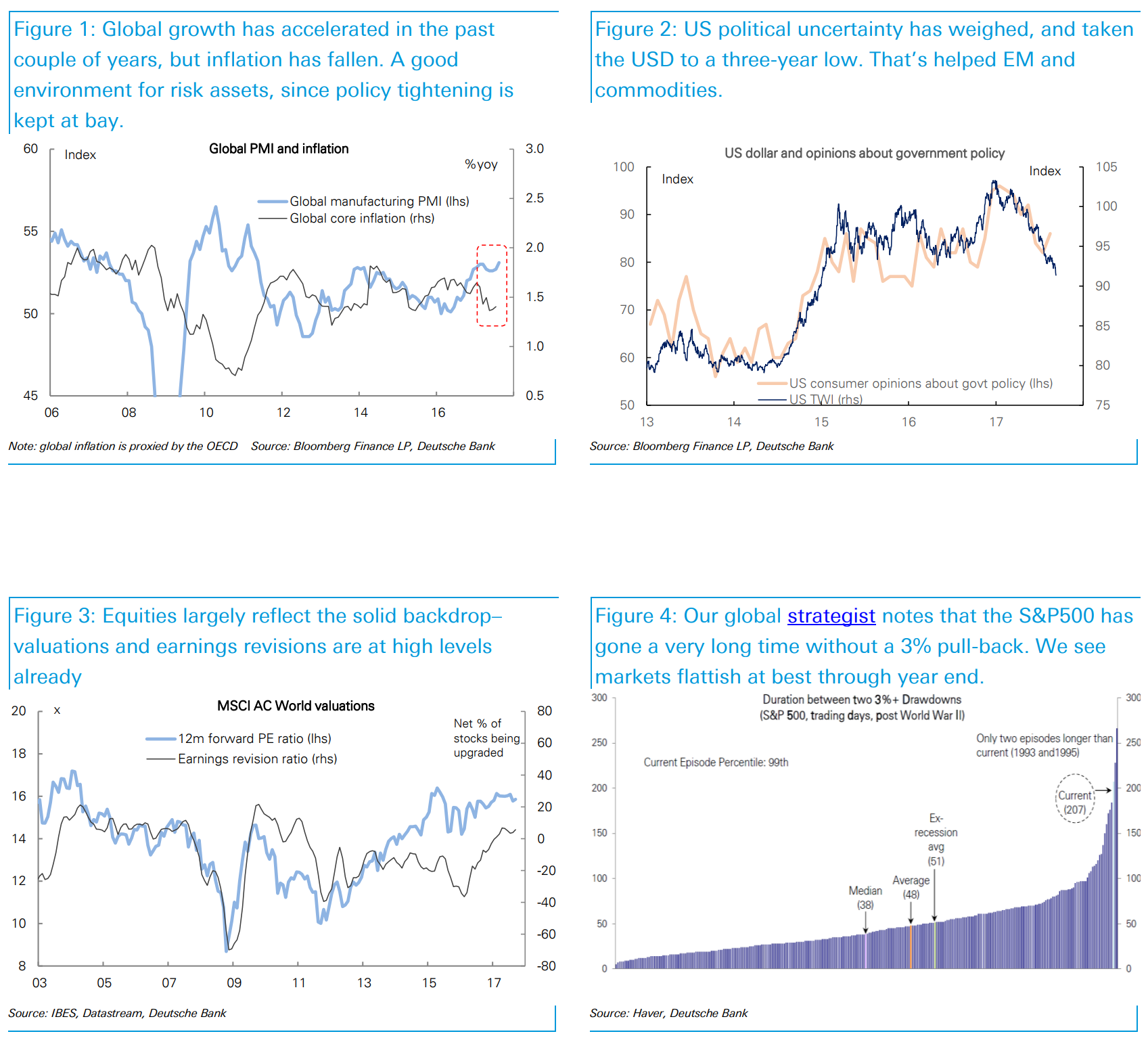

Global backdrop. Growth is the best and broadest we’ve seen in six years, yet inflation is contained. That’s positive for risk assets since it keeps policy tightening at bay. US political uncertainty lingers, though the resulting weaker USD has helped commodities and EM. Equities are reflecting the good backdrop already – PEs and earnings revisions are high, and it’s been a very long time since a sell-off. All up, it’s hard to see gains from here.

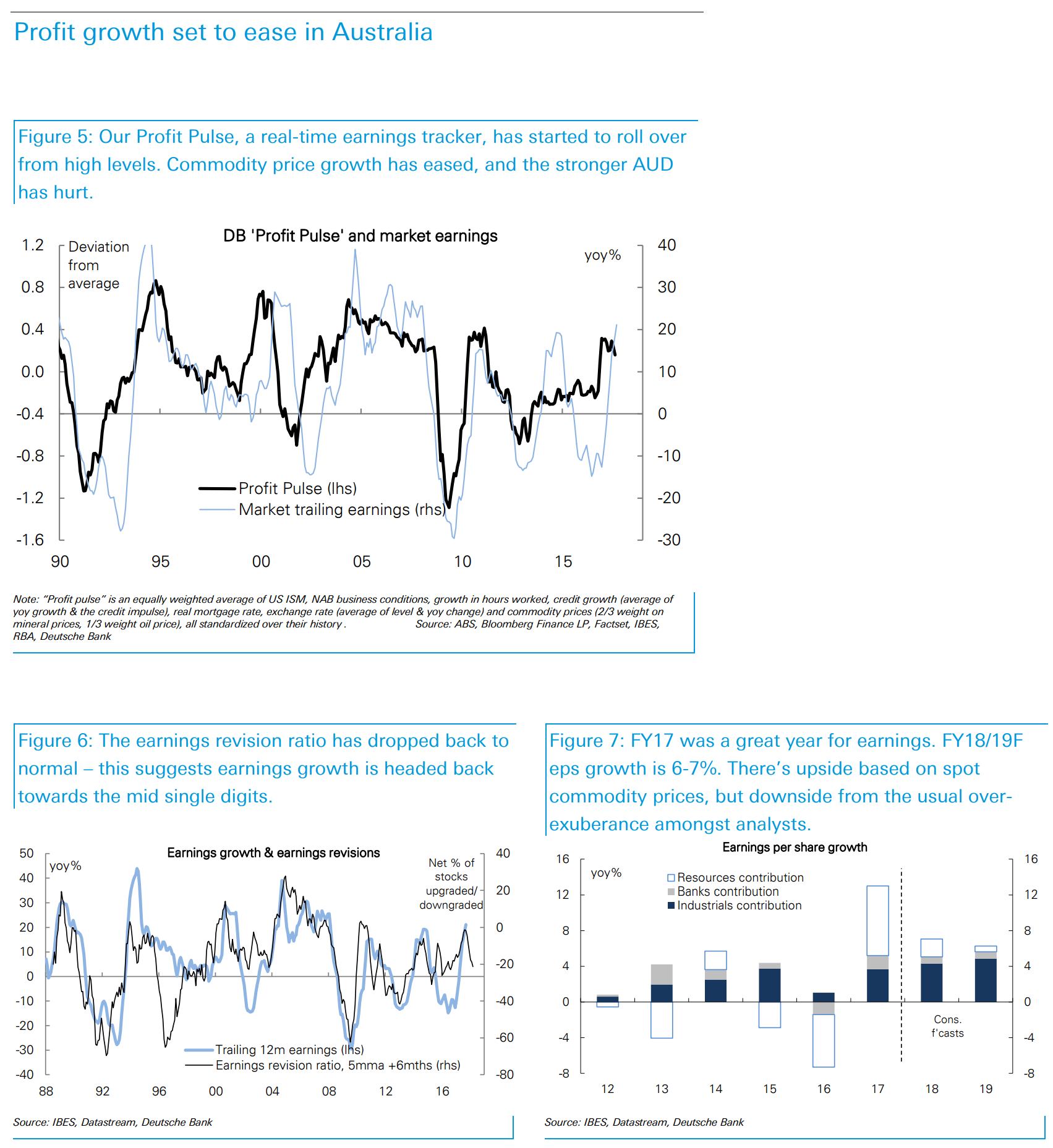

Australian equities. After a strong FY17, earnings growth is likely to return to normal. Both our Profit Pulse and the earnings revision ratio have rolled over already – mid single-digit growth seems likely. Valuations look fine at current levels – in line with our fair value model, and the cyclically-adjusted PE is at average. It’s tough to see Australia outperforming peers.

Resources. A combination of solid Chinese growth, easy monetary policy, and capacity consolidation (including in US shale) is supportive for commodity prices. Spot commodity prices imply earnings upgrades, and companies are already harvesting strong cash flows as capex has ended.

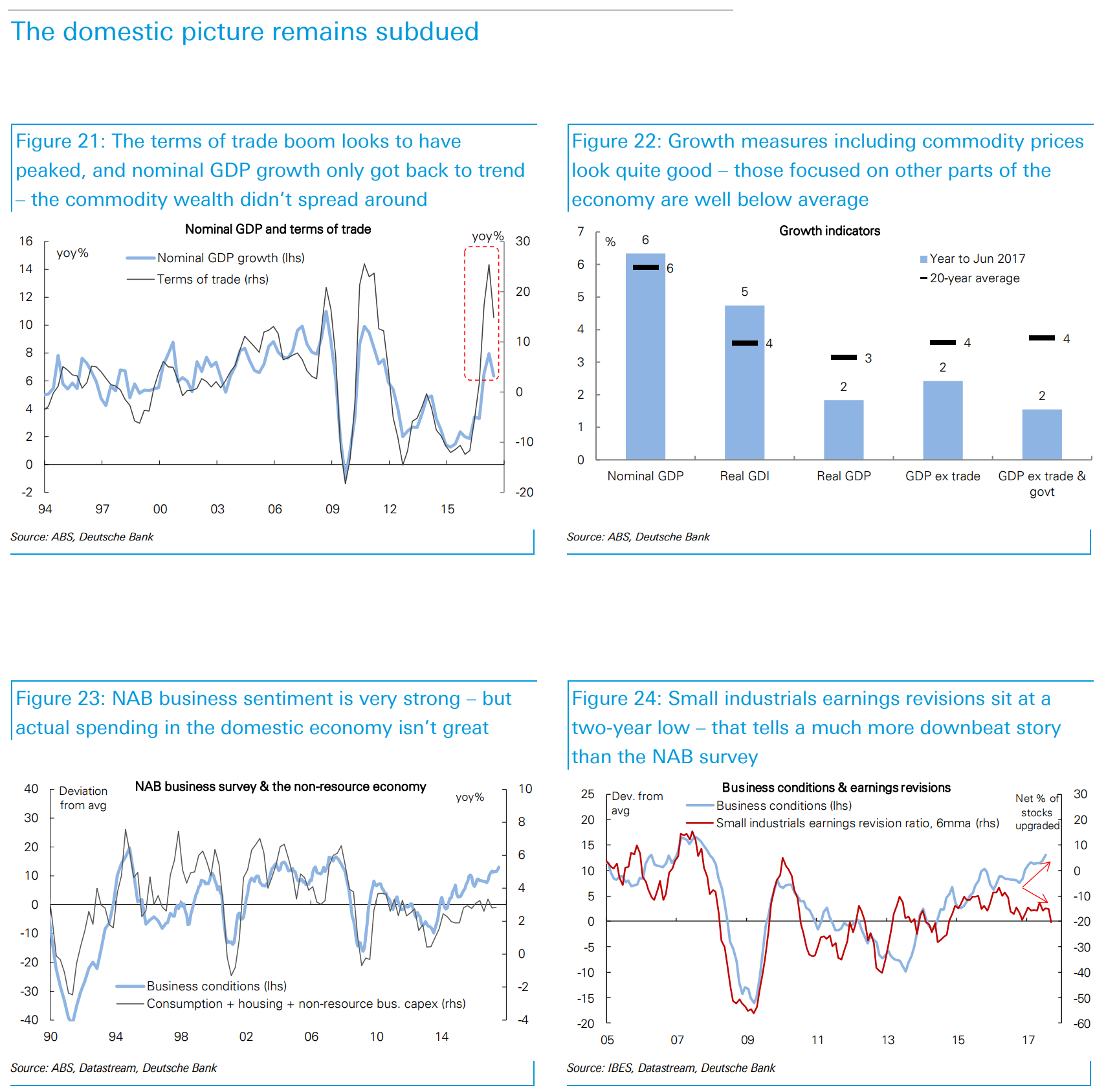

Domestic plays. The economy still looks soggy, with the resource wealth circulating less than before. The strong NAB survey is inconsistent with actual spending and the earnings pulse for Small Industrials. Consumer spend is growing a little, but it’s required a cut in the saving rate given poor wage growth. Housing is likely to stay more robust, and we see some value in sold-down retailers with exposure here.

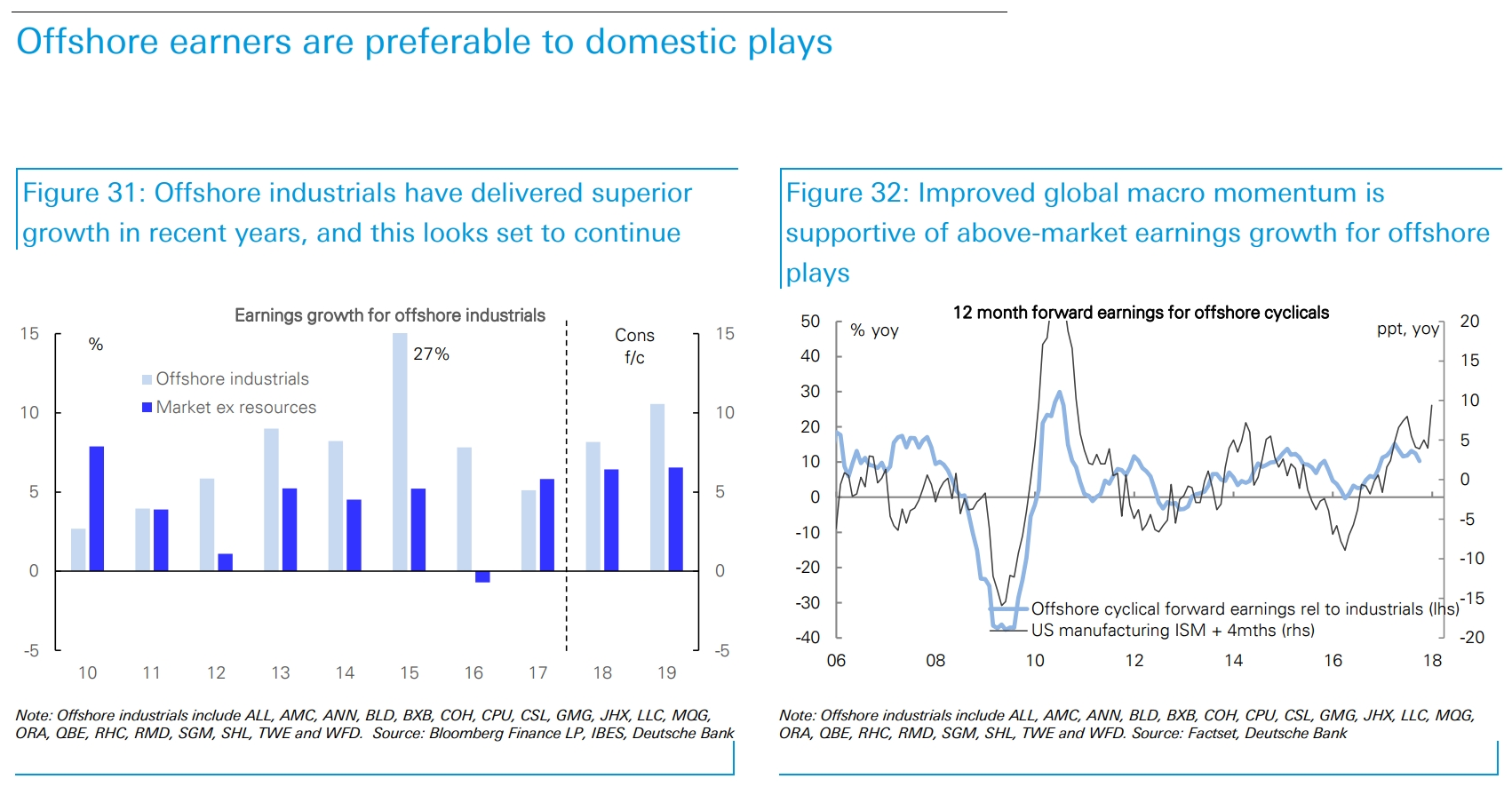

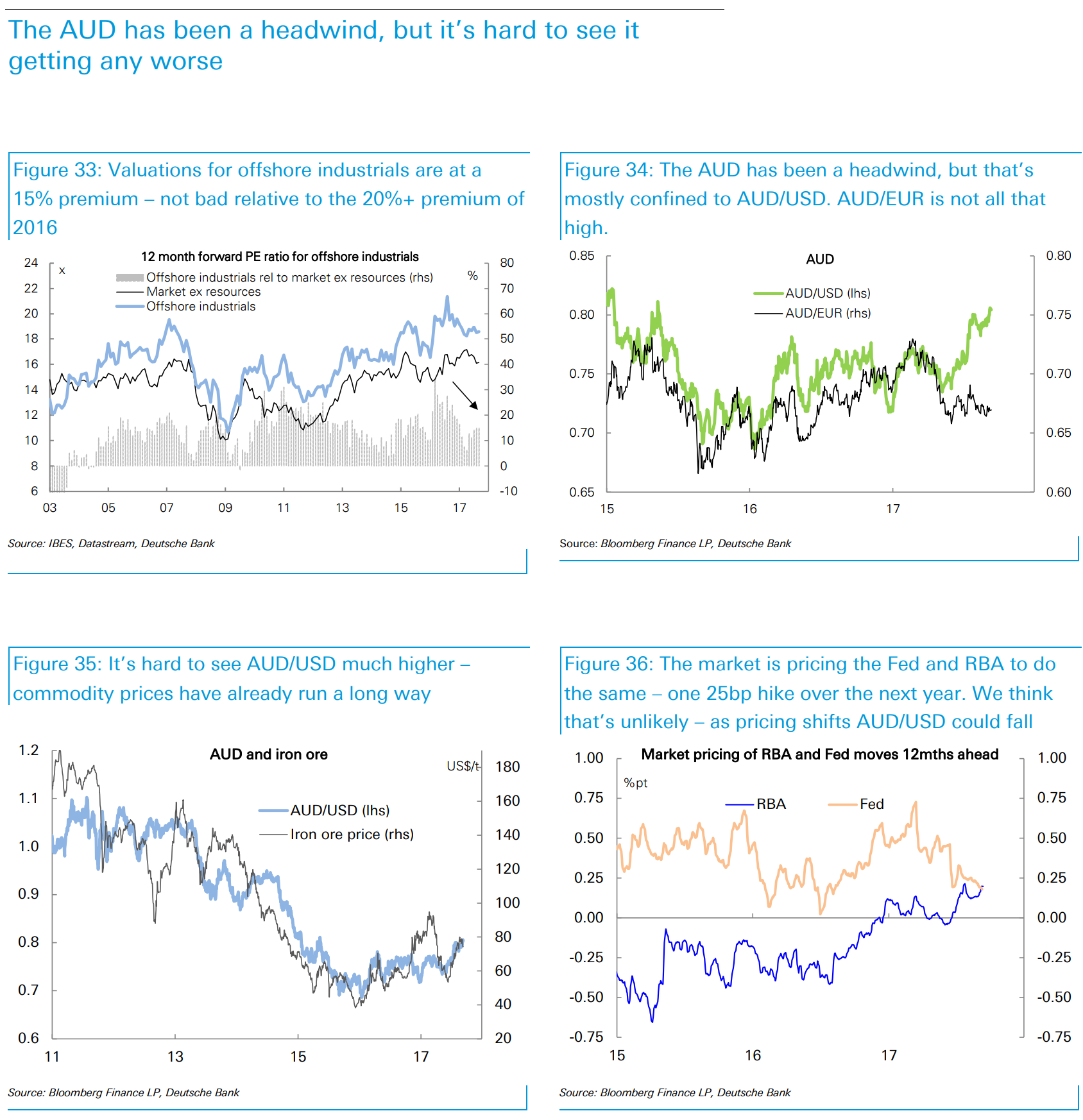

Offshore plays. Superior earnings growth on offer, thanks to solid US & European growth, and valuations look reasonable. The AUD/USD is a headwind, but it shouldn’t get much worse given rate differentials and commodity prices have already moved so much. And AUD/EUR isn’t high – companies with euro exposure are well placed.

Banks. We’re a little overweight, given our lead indicator suggests decent credit growth should continue, and repricing is helping margins. With decent corporate profitability overall, bad debts should stay low. Banks offer a comparable dividend yield to yield stocks without the high valuations, and the vulnerability to rising global bond yields.

Value over growth and underweight yield on extended valuations, and bond yields bottoming. Cyclicals over defensives on neutral valuations but better earnings momentum. Stock correlations are at decade-lows – good for stock-picking. We run a screen for GARP – see page 16.

Model portfolio changes: ADD: Medibank, Worley Parsons, Santos. REMOVE: QBE, ALS, Woodside. Market targets: ASX200 to 5900 by endyear (prev. 6000), 6000 by mid-2018 (unchanged), 6050 by end-2018. This assumes the PE slowly dropping to 15¼x, and earnings growth easing to a mid single-digit pace.

This a good snapshot of the allocations underpinning the MB Fund, though we are underweight Aussie banks because their risk is so awful and miners because we think the cost curve shakeout will resume next year.

Advertisement

David Llewellyn-smith is Chief Strategist at the Macrobusiness Fund and he is definitely talking his book!

David Llewellyn-Smith is Chief Strategist at the MB Fund and MB Super. David is the founding publisher and editor of MacroBusiness and was the founding publisher and global economy editor of The Diplomat, the Asia Pacific’s leading geo-politics and economics portal.

He is also a former gold trader and economic commentator at The Sydney Morning Herald, The Age, the ABC and Business Spectator. He is the co-author of The Great Crash of 2008 with Ross Garnaut and was the editor of the second Garnaut Climate Change Review.