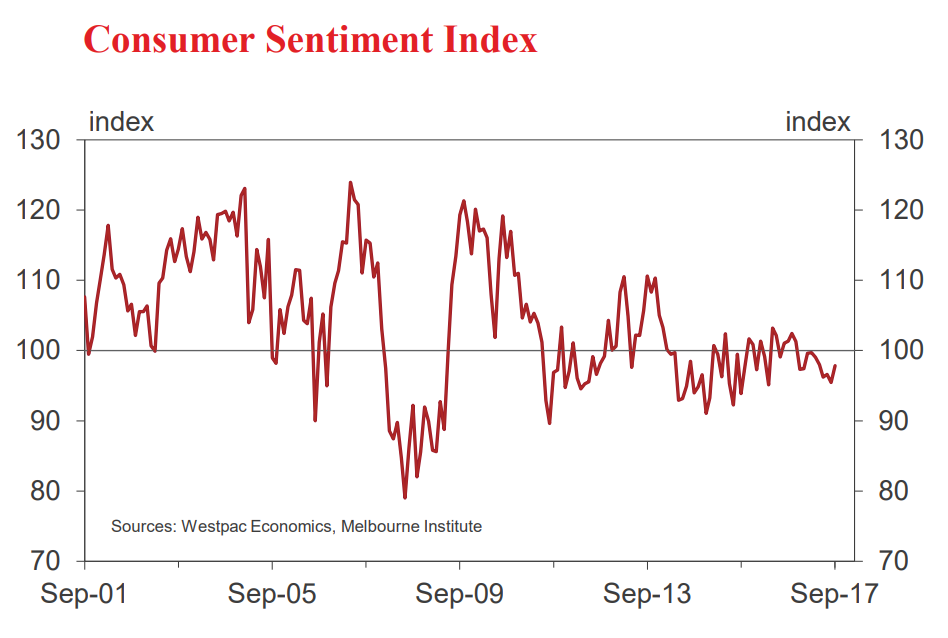

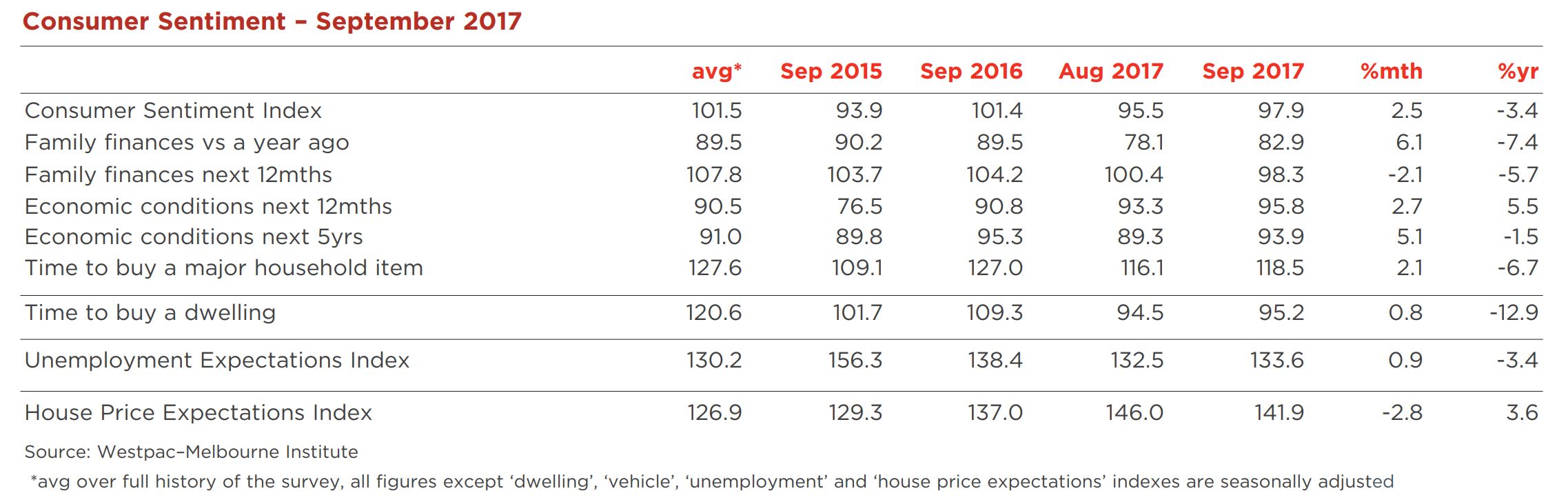

• The Westpac Melbourne Institute Index of Consumer Sentiment rose 2.5% to 97.9 in September from 95.5 in August.

The consumer mood remains downbeat with September marking the tenth consecutive month that pessimists have outnumbered optimists. Pressures on family finances, concerns around interest rates, deteriorating housing affordability and rising energy prices have all weighed on confidence in 2017. These factors are more than offsetting the boost from an improved outlook for jobs particularly when a stronger labour market has not been associated with increased wages growth.

The survey detail shows family finances remain a key area of concern. The ‘finances vs a year ago’ sub-index rose 6.1% but was coming from a very weak read in August (a three year low). Meanwhile the sub-index tracking expectations for ‘finances over the next 12 months’ fell 2.1%, reversing all of last month’s gain.

Consumer expectations for the economy showed more consistent gains. The ‘economic conditions, next 12 months’ sub-index rose 2.7% and the ‘economic conditions, next 5 years’ sub-index posted a robust 5.1% gain. While both are still in pessimistic territory below 100 they are now marginally above long run average levels. The improved but still ‘lukewarm’ sentiment towards the economy likely reflects the somewhat mixed picture from recent data including the June quarter national accounts which showed a reasonably solid 0.8% gain in GDP but subdued annual growth and notable areas of weakness around household incomes and consumer spending.

Consumers were slightly more positive towards major purchases, the ‘time to buy major a household item’ sub-index rising 2.1% in September. However again the rise was small and, coming off a weak August read, the sub-index remains well below its long run average.

The September survey included additional questions on news recall that provide further insight into the factors shaping sentiment. Interestingly, recall levels have fallen significantly over the last three years suggesting consumers may be getting less exposure to news in general. In September the topic areas with the highest recall were ‘economic conditions’ (21%); ‘budget and taxation’ (17%); interest rates (16%); inflation (16%); jobs (15%); and international conditions (12%). While news on all fronts was viewed as unfavourable, consumers rated news on inflation and international conditions as much more negative than three months ago – likely reflecting sharp increases in energy costs and developments around North Korea. The only material improvement was around jobs where news was viewed much less negatively than in June.

The improved labour market situation was also broadly apparent in the Westpac Melbourne Institute Unemployment Expectations Index. Although the index edged up 0.9% in the month, at 133.6 it is still down 4.8% from its June level and the second lowest reading since 2011 (recall that lower reads mean more consumers expect unemployment to fall in the year ahead).

Consumer views around housing were mixed in September. The ‘time to buy a dwelling’ index rose 0.8% but at 95.2 remains at very low levels by historical standards. State indexes continue to vary widely, ranging from a very weak read in NSW (81.3) to a strongly positive result in WA (130.4). Consistent falls in prices in WA over recent years may be finally restoring affordability to attractive levels.

The Westpac Melbourne Institute Index of House Price Expectations dipped 2.8% but at 141.5 remains high overall. Of those consumers with a view, 57% expect prices to rise in the year ahead, 31% expect no change and 12% expect prices to decline.

Responses to additional questions on the ‘wisest place for savings’ continued to indicate risk aversion. Nearly two thirds of consumers still favour safe options – deposits, superannuation or paying down debt – with only 10.5% nominating real estate, a new 40 year low, and 9% nominating shares. More consumers favour ‘pay down debt’ (23.5%) than real estate and shares combined. The Reserve Bank Board next meets on October 3. There is no doubt that the Board will continue to leave the cash rate on hold.

Of more interest is the medium term outlook for interest rates. While those commentators favouring rate hikes next year point to record business conditions we are starting to see a considerable gap open up between business conditions and business confidence. Persistent weak consumer sentiment, consistent with weak consumer demand, may be worrying businesses around the sustainability of current strong conditions.

From our perspective prospects for consumer spending and residential construction appear soft. We do not expect that economic conditions in Australia in 2018 will be consistent with the need for the Bank to raise rates.

David Llewellyn-Smith is Chief Strategist at the MB Fund and MB Super. David is the founding publisher and editor of MacroBusiness and was the founding publisher and global economy editor of The Diplomat, the Asia Pacific’s leading geo-politics and economics portal.

He is also a former gold trader and economic commentator at The Sydney Morning Herald, The Age, the ABC and Business Spectator. He is the co-author of The Great Crash of 2008 with Ross Garnaut and was the editor of the second Garnaut Climate Change Review.