As expected, the Turnbull Government and the Business Council of Australia (BCA) have used the Trump Administration’s pledge to cut the corporate tax rate from 35% to 20% to redouble their lobbying efforts to cut Australia’s corporate tax rate.

Here’s Treasurer Scott Morrison:

Mr Morrison said the Labor Party would leave Australian businesses “stranded on a tax island” and uncompetitive with the US, the UK, Singapore and other countries around the world if it did not allow the Turnbull government to proceed with plans to lower Australia’s rate to 25 per cent.

“Having a lower tax environment for business to invest is good for jobs, it’s good for investment, and the Labor Party through their politics of envy frankly just don’t get it, and they are putting a very heavy tax on jobs by not supporting us to have a more competitive tax environment,” Mr Morrison said.

And here’s BCA chief executive, Jennifer Westacott:

“Every company tax reduction overseas is a de facto tax increase in Australia and a disincentive for investors,” BCA chief executive Jennifer Westacott said…

“Make no mistake, we are in the midst of a global fight to attract investment dollars and Australia is lagging badly”…

The BCA calls Australia’s tax competitiveness “woeful” and its broader competitiveness ranking “mediocre at best”…

Ms Westacott said only company tax reductions would get wages growing again and called on the Senate to pass the enterprise tax plan, which she said would go some of the way to restoring Australia’s competitiveness and boosting the economy.

“Doing nothing is no longer an option.”

Thankfully, Labor shadow treasurer, Chris Bowen, is holding firm against further corporate tax cuts:

“Malcolm Turnbull and Scott Morrison have a plan for a big business tax cut worth $65 billion paid for by higher taxes for middle income Australians,” Mr Bowen said.

“With a Budget still in deficit and gross debt over half a trillion dollars and projected to reach $750bn without peaking, a $65 billion big business tax cut cannot be justified.”

Sadly for Scott Morrison and the BCA, the Treasury’s own modelling on the company tax cut package showed minimal benefits for either jobs or growth. As explained by The Australia Institute’s Richard Denniss:

According to Treasury’s in-house modelling, and the modelling it commissioned from Chris Murphy, if the company tax rate is lowered from 30 per cent to 25 per cent then gross domestic product will double by September 2038, while without the tax cut it won’t double until December 2038. Wow, a whole three months earlier. Both modelling exercises conclude that in 20 years’ time the unemployment rate will be 5 per cent regardless of whether we spend $50 billion on company tax cuts or not…

The “benefits” are more accurately described as rounding error than significant reform.

The Grattan Institute has also pointed out that if companies pay less tax then some could reinvest some of what they save. But in practice, most profits are paid out to shareholders. So the tax cut won’t have much of an impact on domestic investment or jobs.

And yet despite these minuscule benefits to jobs or growth, the full company tax cut package would cost the federal budget a small fortune in lost revenue.

Again, the modelling of the company tax cut package conducted by Independent Ec0nomics on behalf of the Australian Treasury estimated that the full company tax cut package would cost $11.3 billion per year. However, this would be reduced to $8.2 billion due to “a gain in personal income tax and superannuation income tax of $3.1 billion as the cut in company tax automatically reduces the value of franking credits”.

Obviously, the loss of revenue from company tax cuts would need to be made up somewhere, such as by raising personal income taxes, cutting government investment in infrastructure, or slashing welfare expenditure. Such cuts would necessarily reduce jobs and growth.

The fact of the matter is that Australia’s unique dividend imputation system strongly undermines the case for company tax cuts, since the lion’s share of the benefits from cutting company taxes would flow to foreign owners/shareholders, thus representing a direct fiscal transfer from Australian taxpayers to foreigners, and lowering national income in the process.

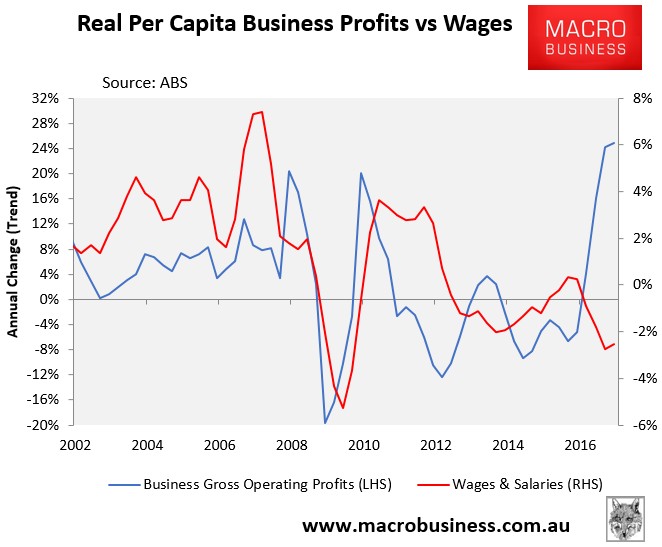

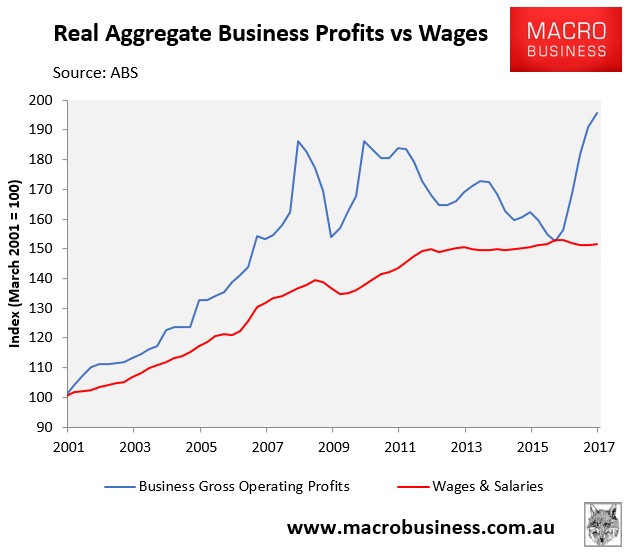

Ms Westacott’s claim that “only company tax reductions would get wages growing again” is also ridiculous. Real per capita business profits have lifted 25% over the past year at the same time as real wages have fallen:

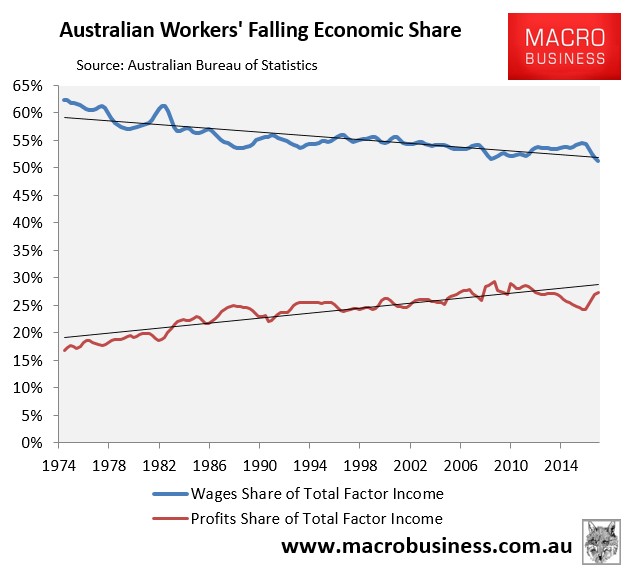

Moreover, workers’ share of total factor income has hit the lowest level since June 1964:

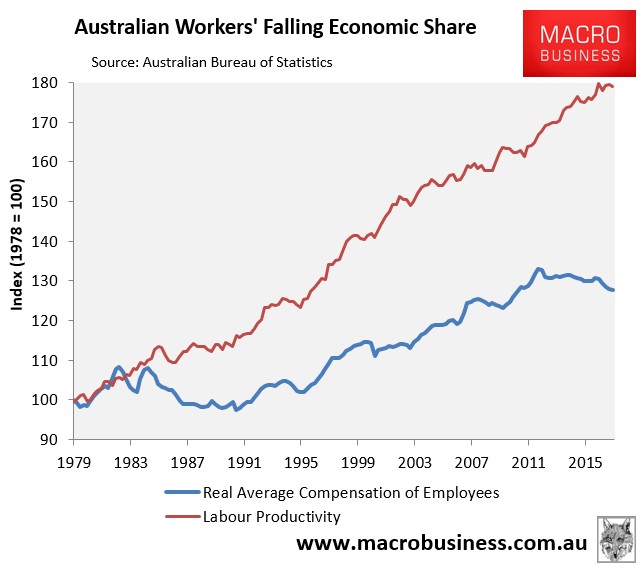

And this has occurred in the face of strong labour productivity growth:

Why should anyone trust the BCA’s claim that cutting company taxes would magically lift wages when surging company profits have not done the trick?

While labour has been doing a great job, as evident by its strong productivity performance, its efforts are getting killed by dismal capital productivity as savings are massively mis-allocated into profitless houses, profitless energy and a profitless government that wouldn’t know a reform policy if it ran over it in a bus.

The last thing that Australia should do is lower the company tax rate, which would unambiguously benefit the wealthy and worsen inequality.

Rather than this blind faith in flawed ‘trickle-down’ economics, Australia needs tax reforms that encourage capital to be once again deployed into productive investments.

Alternatively, the federal government could use the tens-of-billions of dollars that would be spent on cutting company taxes to undertake critical infrastructure investment and restore Australia’s dilapidated infrastructure stock, which is under siege from its own mass immigration agenda.

unconventionaleconomist@hotmail.com