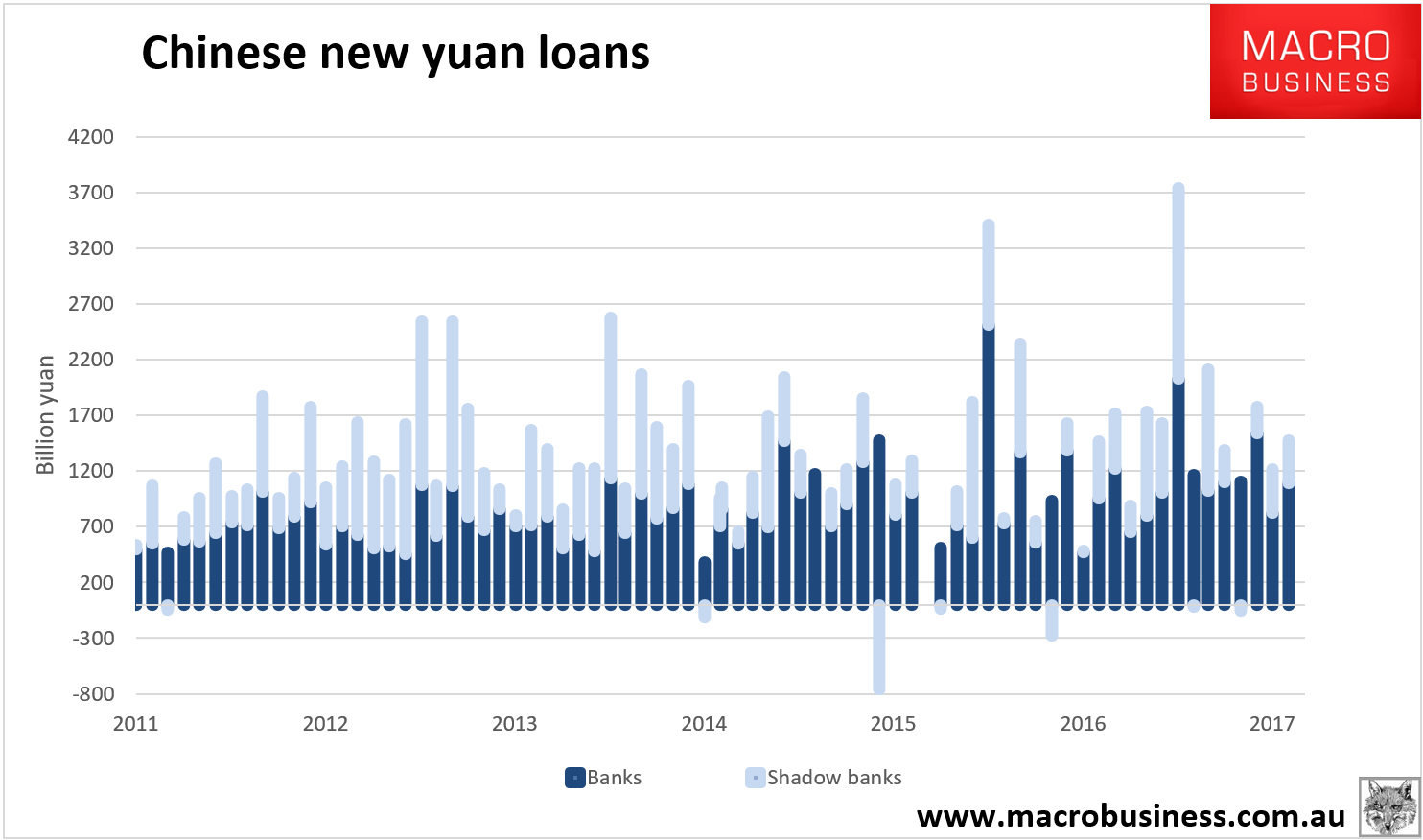

August new yuan loans were out Friday night and for the uninitiated appeared strong with 1.48tr yuan in total social financing:

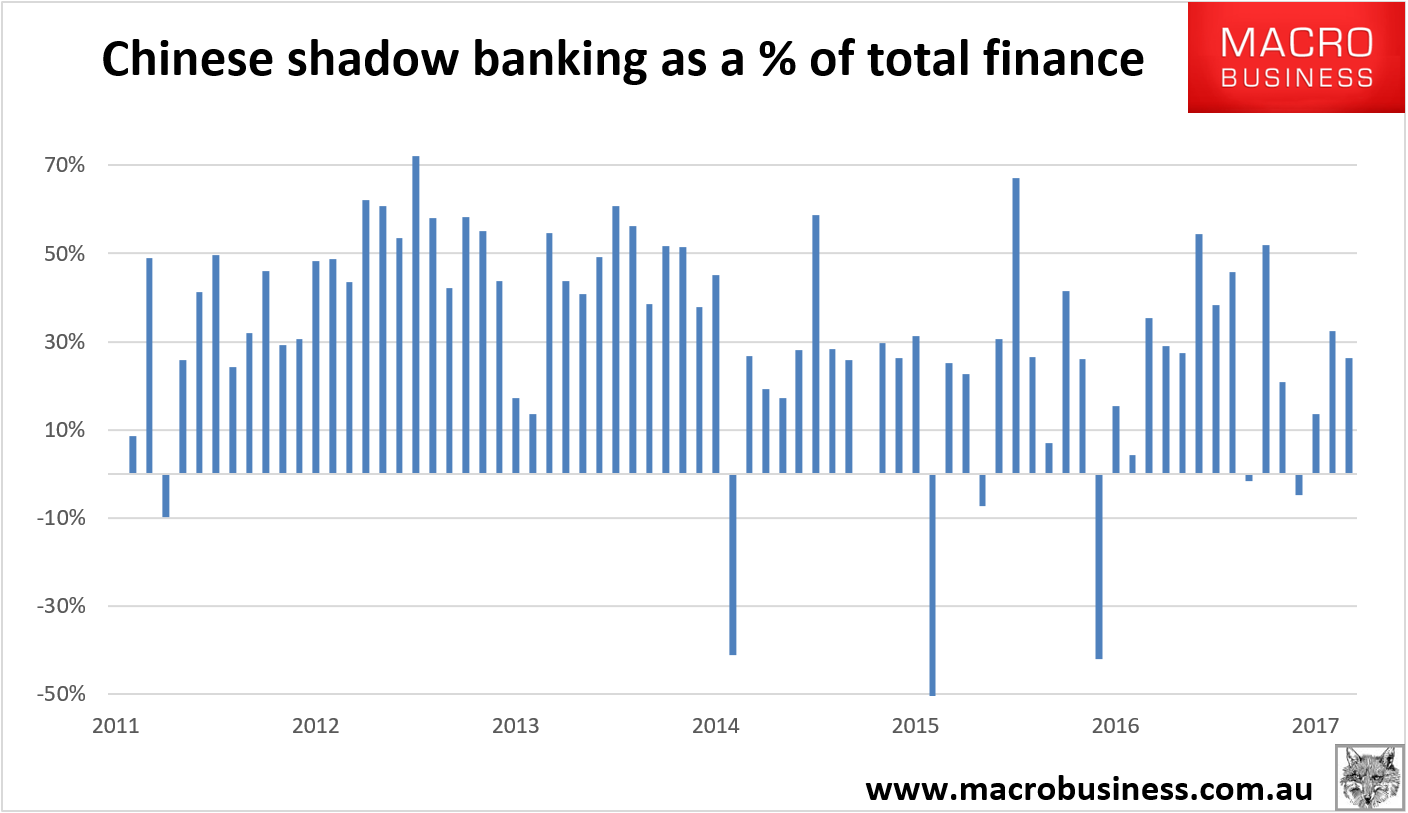

Shadow banks made up one quarter of that:

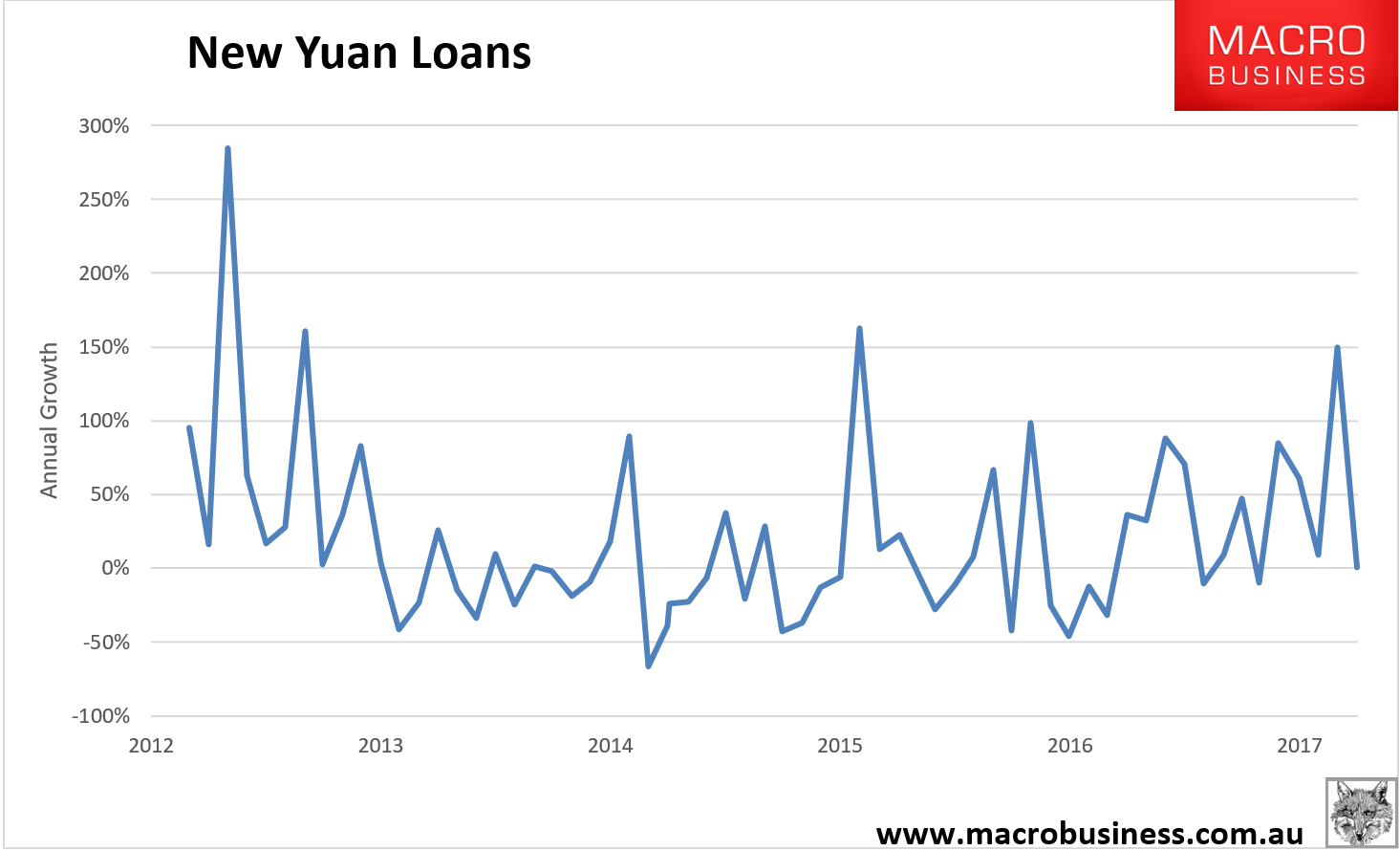

Year on year growth sank to zero:

Advertisement

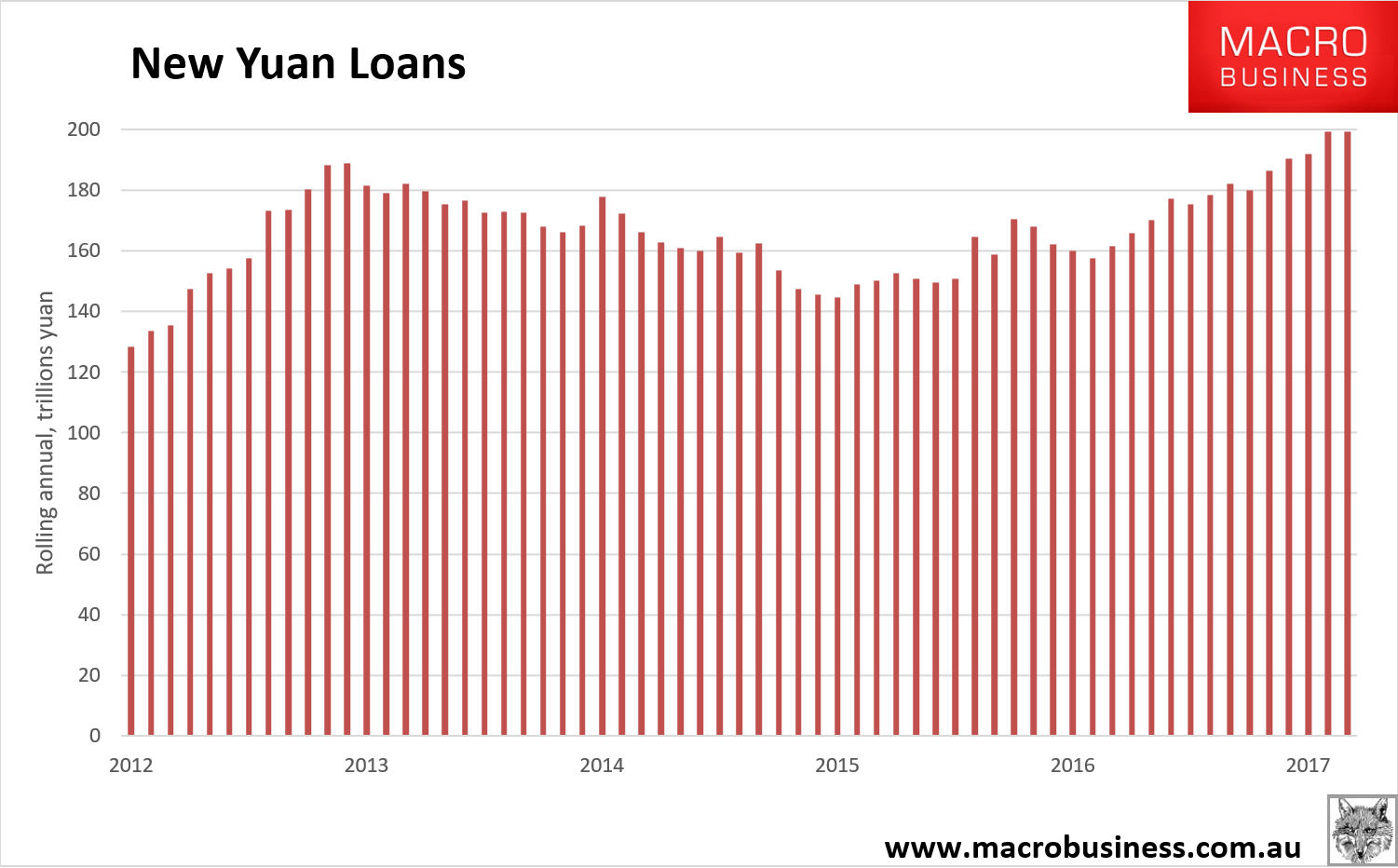

The rolling annual topped out:

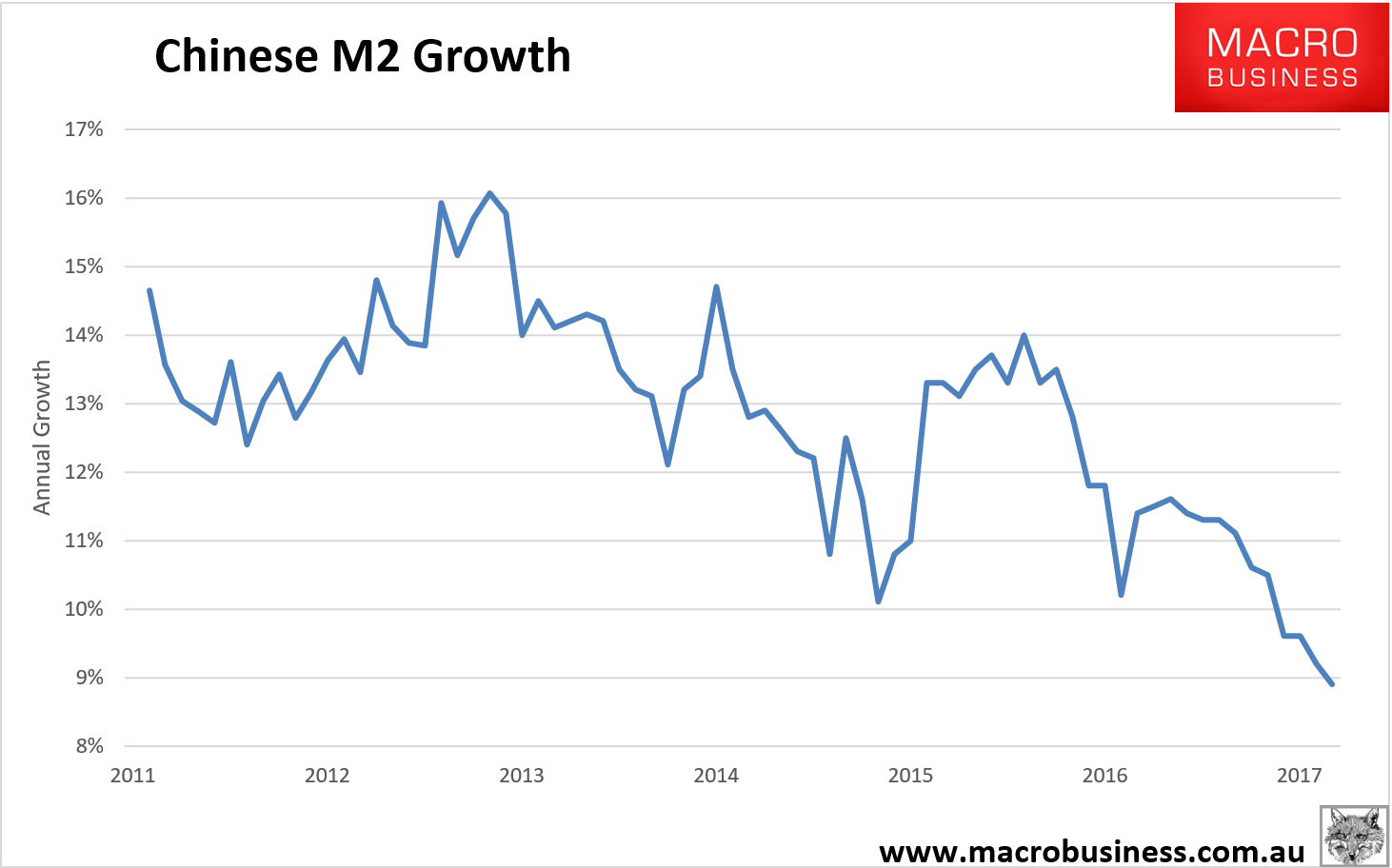

And M2 sank to a new all-time low at 8.6%, almost developed market-like:

Advertisement

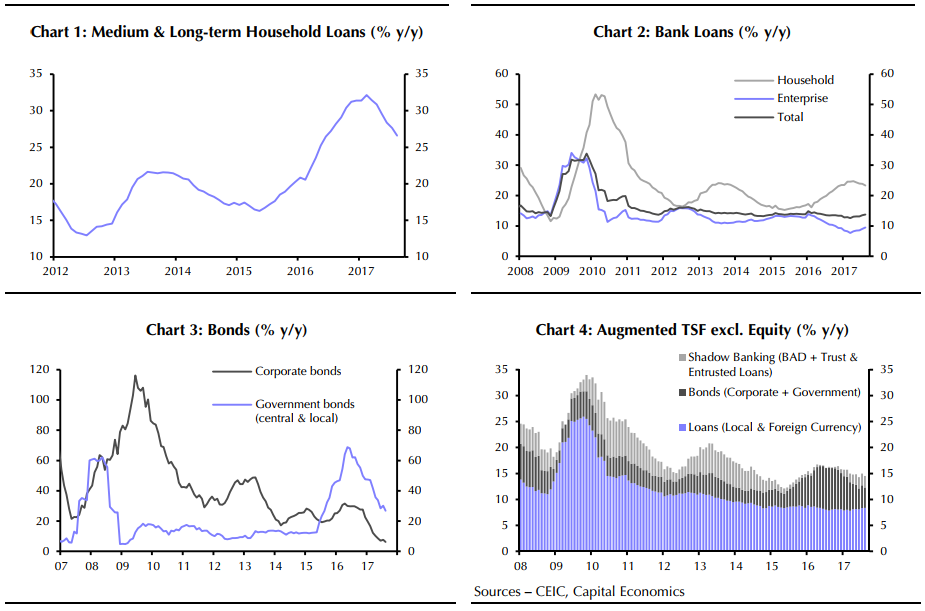

The detail was even more revealing of ongoing softening as long term household loans, mostly mortgages, rose to 663.5 billion yuan in August from 561.6 billion yuan in July but are decelerating consistently year on year. Capital Economics has more:

New lending rose in August, but this masks a decline in underlying credit growth, which has trended down during the past year. A further slowdown appears likely given the government’s current campaign against financial risks.

Medium and long-term bank lending to households, a proxy for mortgages, continued to slow – a sign that property demand is cooling. (See Chart 1.) This was offset by more rapid bank lending to firms. (See Chart 2.) That said, we think it would be wrong to conclude that credit demand among firms is strengthening. Instead, it appears that firms are responding to higher yields by substituting bank loans for bond issuance.

Indeed, after a short-lived reversal in July, the slowdown in corporate bond issuance resumed last month. Issuance of government bonds – which are not included in the TSF figures – also cooled in August. (See Chart 3.) After adding in government bonds, broad credit growth declined from 15.0% y/y to 14.6%, reversing most of the pick-up in July. (See Chart 4.)

Today’s data are consistent with our view that broad credit growth remains on a downward trajectory. It is likely to cool further in coming quarters as monetary conditions remain relatively tight. While we don’t expect the People’s Bank to push up rates any further, a decisive shift toward monetary policy easing seems unlikely at this stage given the rhetoric over controlling financial risks.

David Llewellyn-Smith is Chief Strategist at the MB Fund and MB Super. David is the founding publisher and editor of MacroBusiness and was the founding publisher and global economy editor of The Diplomat, the Asia Pacific’s leading geo-politics and economics portal.

He is also a former gold trader and economic commentator at The Sydney Morning Herald, The Age, the ABC and Business Spectator. He is the co-author of The Great Crash of 2008 with Ross Garnaut and was the editor of the second Garnaut Climate Change Review.