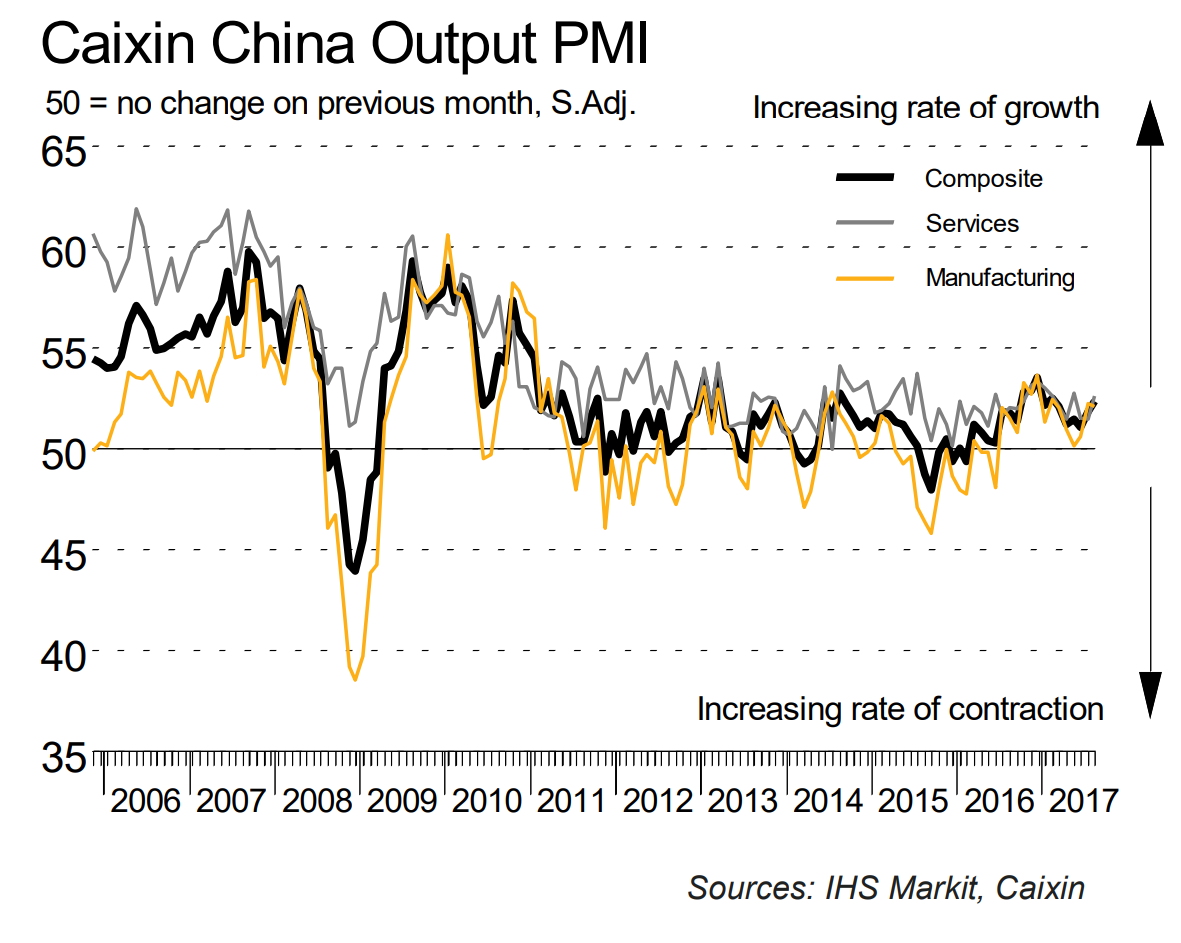

The Caixin China Composite PMI™ data (which covers both manufacturing and services) indicated that Chinese business activity growth picked up for the second month in a row during August. Furthermore, the latest expansion of activity was the strongest seen for six months, as shown by the Composite Output Index posting 52.4, up from 51.9 in July.

August data revealed that the latest expansion of overall business activity was underpinned by increased activity at both manufacturers and services providers. Notably, services companies registered the quickest upturn in business activity for three months. This was highlighted by the seasonally adjusted Caixin China General Services Business Activity Index rising from 51.5 in July to 52.7. At the same time, goods producers noted a further modest increase in output that was little-changed from that seen in the previous month.

In line with the trend for activity, growth in new business accelerated in the service sector midway through the third quarter. The latest increase in new work was the fastest seen in three months and solid overall, with a number of companies linking growth to improving market conditions and new marketing strategies. At the same time, new order intakes at manufacturers rose to the greatest extent in over three years. As a result, composite new business increased at the joint-quickest pace in 2017 to date.

Stronger growth of activity and new orders led service providers to expand their payrolls again in August. Notably, the rate of job creation was the fastest seen for four months. Meanwhile, manufacturers reported a further reduction in headcounts in the latest survey period, though the rate of job shedding moderated since July. At the composite level, employment stabilised in August, thereby ending a four-month sequence of decline.

Manufacturers and services companies in China both reported higher amounts of outstanding work during August that was in turn linked to greater new order intakes. That said, service providers saw only a marginal rate of backlog accumulation that was the weakest in four months. The level of work-in-hand (but not yet completed) at manufacturing firms increased at a pace that, though modest, was the quickest seen in the year to date. Consequently, unfinished workloads continued to rise modestly at the composite level.

Cost burdens continued to rise at a sharper pace at manufacturers than service providers in August. Notably, the rate of input price inflation at goods producers accelerated to five-month high, with a number of panellists commenting on higher raw material costs. In contrast, average input prices rose at a marginal pace at services firms that was one of the slowest seen over the past eight years. Subdued cost pressures at services companies did not offset the steeper increase in input costs at manufacturers, however, as shown by composite input costs rising to the greatest extent since March.

Prices charged by Chinese services firms declined during August amid reports of greater market competition. Though only marginal, it was the first time that prices had fallen for nearly a year-and-a-half. Manufacturers meanwhile increased their factory gate charges and at a solid rate. According to panellists, companies raised their selling prices due to greater cost burdens. At the composite level, prices charged increased at the steepest rate for five months. After dipping in July, overall business confidence in China picked up slightly in August. The improvement was driven by stronger optimism across both the manufacturing and service sectors, with the latter expressing the most marked degree of positive sentiment.

David Llewellyn-Smith is Chief Strategist at the MB Fund and MB Super. David is the founding publisher and editor of MacroBusiness and was the founding publisher and global economy editor of The Diplomat, the Asia Pacific’s leading geo-politics and economics portal.

He is also a former gold trader and economic commentator at The Sydney Morning Herald, The Age, the ABC and Business Spectator. He is the co-author of The Great Crash of 2008 with Ross Garnaut and was the editor of the second Garnaut Climate Change Review.