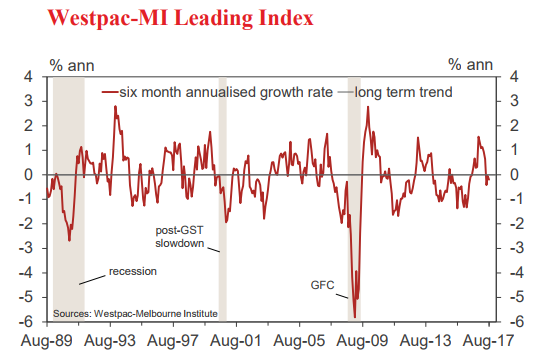

• The six month annualised growth rate in the WestpacMelbourne Institute Leading Index, which indicates the likely pace of economic activity relative to trend three to nine months into the future, slipped from –0.04% in July to –0.19% in August.

The six month annualised growth rate in the WestpacMelbourne Institute Leading Index, which indicates the likely pace of economic activity relative to trend three to nine months into the future, slipped from –0.04% in July to –0.19% in August.

Westpac’s Chief Economist, Bill Evans, commented, “The growth rate remains negative for a third consecutive month pointing to below trend momentum and a sharp turnaround from strong positive, above trend reads at the start of the year.”

While the Index only gives us a glimpse of the likely momentum in the first few months of 2018 it currently seems to be more consistent with our view of the likely growth environment next year than the Reserve Bank’s forecast for growth comfortably above trend.

Westpac is currently forecasting growth of 2.5% in 2018 compared to the RBA’s 3.25%. Trend growth is generally assessed as 2.75%.

The Leading Index growth rate has slowed from 1.13% above trend in March to 0.19% below trend in August, a deterioration of 1.32ppts. Two components account for almost all of the reversal: commodity prices (–1.31ppts) and the yield spread (–0.43ppts).

After surging nearly 40% over the second half of 2016, the RBA’s AUD commodity price index has retraced nearly 12% in 2017 to date.

Similarly, after widening by over 100bps in 2016, the yield gap – the difference between the 90day bill rate and the 10yr bond rate – has narrowed by about 12bps, pointing to more subdued market outlook for economic conditions.

The contribution from other index components has been more mixed. On the positive side, the index growth rate has been boosted by: dwelling approvals (+0.27ppts); aggregate monthly hours worked (+0.26ppts); and the Westpac-MI Unemployment Expectations index (+0.09ppts). However, these improvements have been partially offset by a bigger drag from the S&P/ASX 200 (–0.22ppts) while other components have been largely unchanged.

The Reserve Bank Board next meets on October 3. There is no doubt that the Board will continue to leave the cash rate on hold. Of more interest is the medium term outlook for interest rates. The dominant dynamic that is likely to keep rates on hold will be ongoing weakness in income growth (reflecting weak wages growth and slowing employment) constraining consumers’ capacity to lift spending. High household debt levels and ongoing risk aversion will discourage households from further substantial cuts to their savings rates.

While overall business conditions are currently strong that is not widespread across all industries with manufacturing and construction dominating. Signs of a slowing in residential construction are also pointing to an easing in confidence in the construction sector and investment and employment intentions may ease.

With macro-prudential policies slowing housing markets, the need to raise interest rates in 2018 seems unnecessary. Westpac continues to expect rates will remain on hold in 2018.

David Llewellyn-Smith is Chief Strategist at the MB Fund and MB Super. David is the founding publisher and editor of MacroBusiness and was the founding publisher and global economy editor of The Diplomat, the Asia Pacific’s leading geo-politics and economics portal.

He is also a former gold trader and economic commentator at The Sydney Morning Herald, The Age, the ABC and Business Spectator. He is the co-author of The Great Crash of 2008 with Ross Garnaut and was the editor of the second Garnaut Climate Change Review.