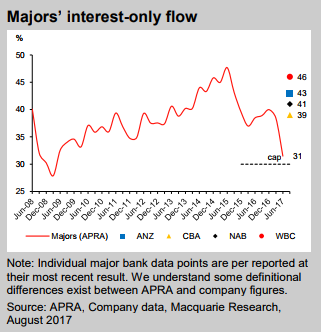

Following the introduction of APRA’s 30% interest-only cap there has been a material reduction in interest-only flow and assuming current trends continue banks will be well below the cap by the required timeframe (Sep-17). This was achieved by a combination of aggressive repricing, tightening of credit standards and some concessions from the regulator. We understand that adhering to the IO cap appears less onerous after the regulator relaxed their treatment of existing loan roll-overs into another interest-only period and lines of credit being excluded from the cap. While in the short term these actions reduce the risk around potential market dislocation, we continue to believe the current economics of IO borrowing is increasingly difficult to justify for customers. We expect more switching and slower growth in IO to result in a headwind to bank margins and medium-term profitability across banks’ mortgage portfolios.

David Llewellyn-Smith is Chief Strategist at the MB Fund and MB Super. David is the founding publisher and editor of MacroBusiness and was the founding publisher and global economy editor of The Diplomat, the Asia Pacific’s leading geo-politics and economics portal.

He is also a former gold trader and economic commentator at The Sydney Morning Herald, The Age, the ABC and Business Spectator. He is the co-author of The Great Crash of 2008 with Ross Garnaut and was the editor of the second Garnaut Climate Change Review.