Via the AFR:

It’s almost impossible to find anyone these days who’s not frustrated about the lacklustre efforts of the local sharemarket when compared to Wall Street and how the major S&P ASX 200 index just can’t get much beyond the 5700 level in any meaningful way.

Unfortunately for investors, both trends look set to continue.

Earning and interest rates are always seen as the key drivers of sharemarkets and although it’s early days for this reporting season, it seems investors aren’t impressed with some of the latest results.

As for the topic of interest rates, whenever it does come up the talk is usually about how, eventually, they will have to head higher.

Hmm, well, that’s sure thinly sliced analysis but it is kind of true given the simplicity of the Australian economic model.

The great under-performance versus the S&P500 began in 2011:

That date is not coincidental. 2011 was also the peak for the mining boom and it is the post-boom adjustment that is the real reason for the ASX dawdle.

Economists and strategists rarely consider the structure of the economy. That’s pretty stupid when you consider that it is economic structure that determines longer economic cycles. In Australia’s case, we spent every waking hour after the millennium favouring two sectors above all others in the economy: banking and mining. It worked for a while to boost living standards as we enjoyed enormous income flows from the mining boom, took that easy money and leveraged it in global markets via the banks, then stuck that debt into house prices and consumption.

But after a while we gave ourselves a monstrous case of double Dutch disease as we hollowed everything else out.

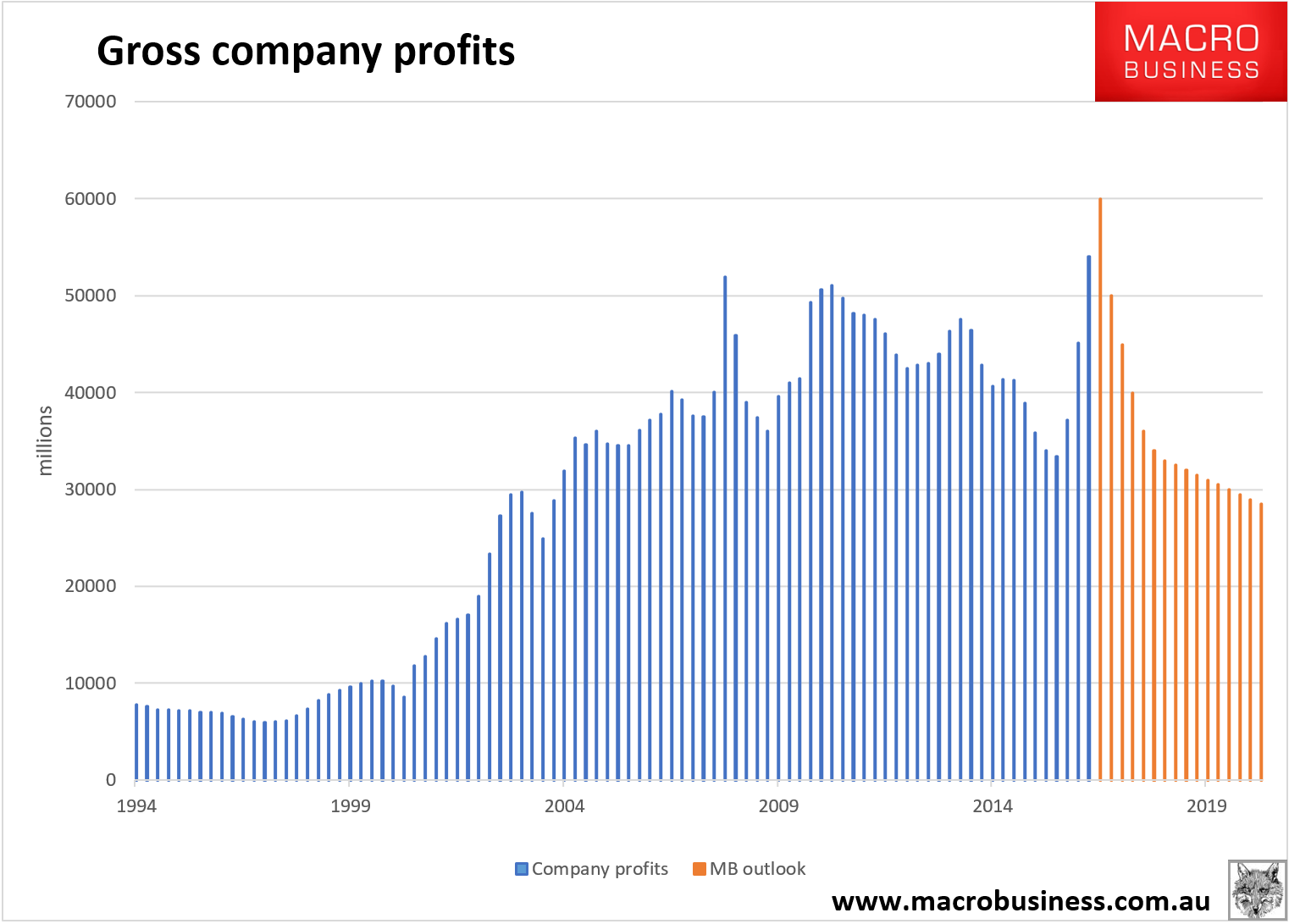

Then, sadly, the income tide from mining started to go out and corporate profits went straight out with it:

We’ve recently seen a big rebound but it’s all in mining and really only in a handful of firms. Moreover, it won’t last as iron ore and coal fall away to new lows ahead as China goes ex-growth. Even with the recent spike profits have barely budged in a decade.

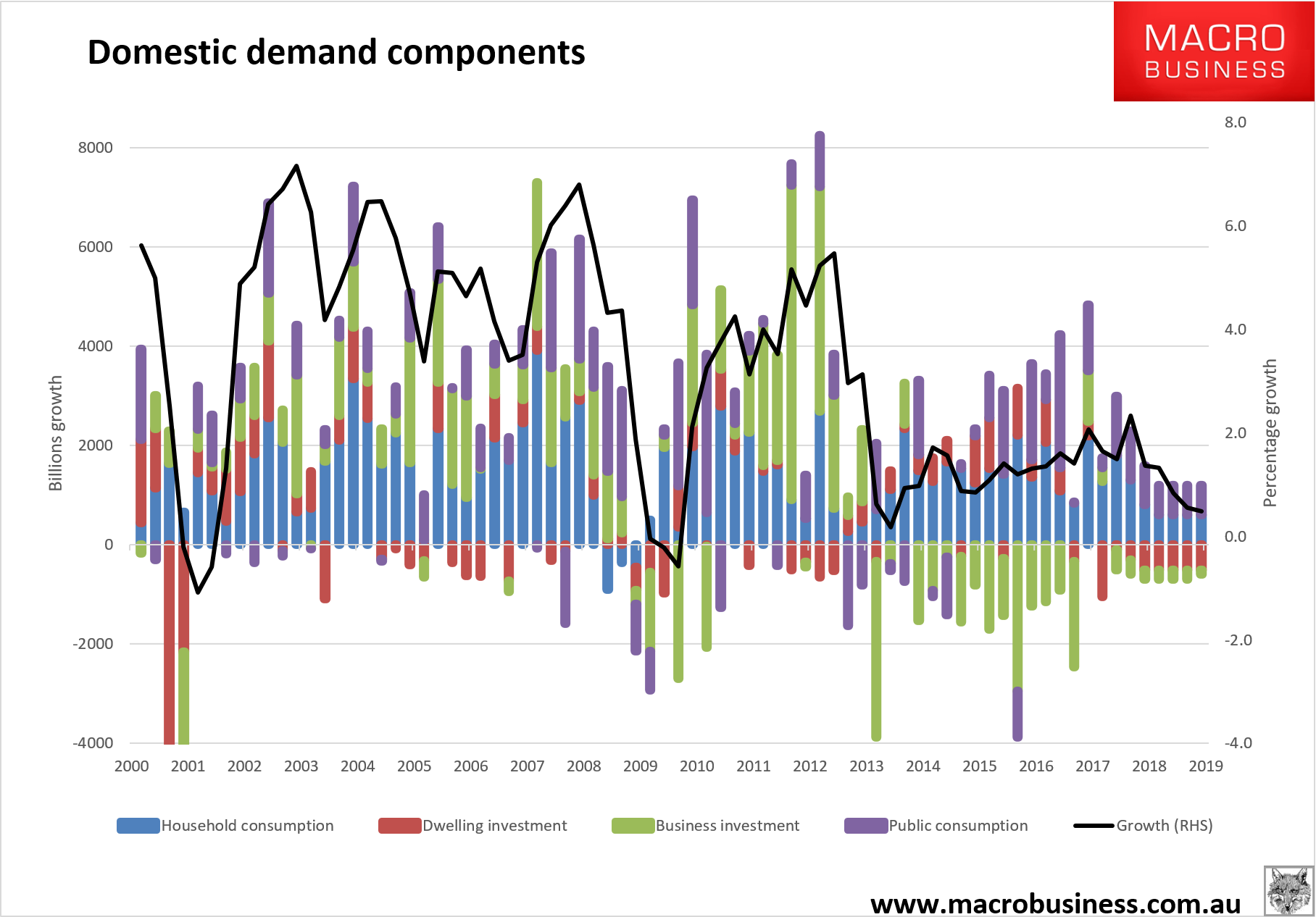

As mining income receded, we relied more on the leveraging. But that, too, had its limits. Households were already massively indebted and without any income growth, mortgages just didn’t appeal like they used to:

And so we filled the demand, income and profits hole with immigration growth. But that just hasn’t cut it given it also smashes wages.

Today we have an economy that barely has a domestic demand pulse, is hooked on public spending, has no investment growth and withering consumption ahead as deleveraging takes a hold with an exhausted housing boom (despite the what the happy idiots at the RBA say):

We’ve few non-mining external sector earners of significance left and domestic demand is shite. I mean, seriously, there is no mystery to ASX under-performance at all and it has years yet to run.

————————————————————————————————

Disclosure: I’m the strategist for the Macrobusiness Fund which is currently overweight international stocks. We also run an international equities fund. Both of these will benefit from a falling Australian dollar so I am definitely talking my own book.

Register your interest in the fund and we’ll be touch.