The run-up to 0.8000 looks stretched. Continued uncertainty about the USD may hold the AUD up, however

We see rates on hold at 1.5%. Recent data suggests the risks to the upside are rising.

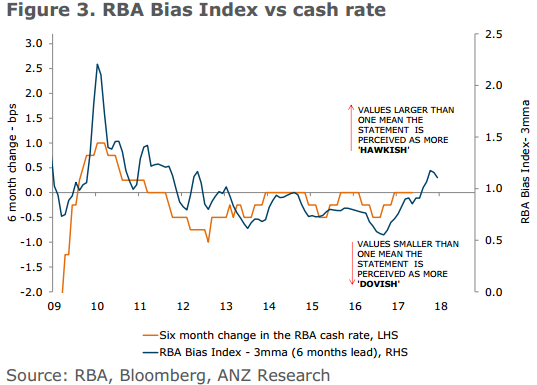

We have used statistical techniques to analyse the language in the RBA’s post-board meeting statements. From this we have constructed a measure of the RBA’s bias – our RBA Bias Index. This index provides a clear signal about the likely change in the cash rate over the coming 6-12 months (Figure 3). It also leads changes in market pricing of the RBA cash rate. The most recent post-meeting statements have taken the RBA Bias Index a little above one. This indicates the RBA’s policy bias is starting to lean in a slightly hawkish direction. We don’t think the signal is yet strong enough to shift our view from ‘on hold’, but the evolution of the RBA’s language clearly bears watching.

Meh. The RBA’s dwelling construction and business investment outlook is way too strong. If it hikes it’ll be a policy error. Still quite unlikely.

Also, Morgan Stanley:

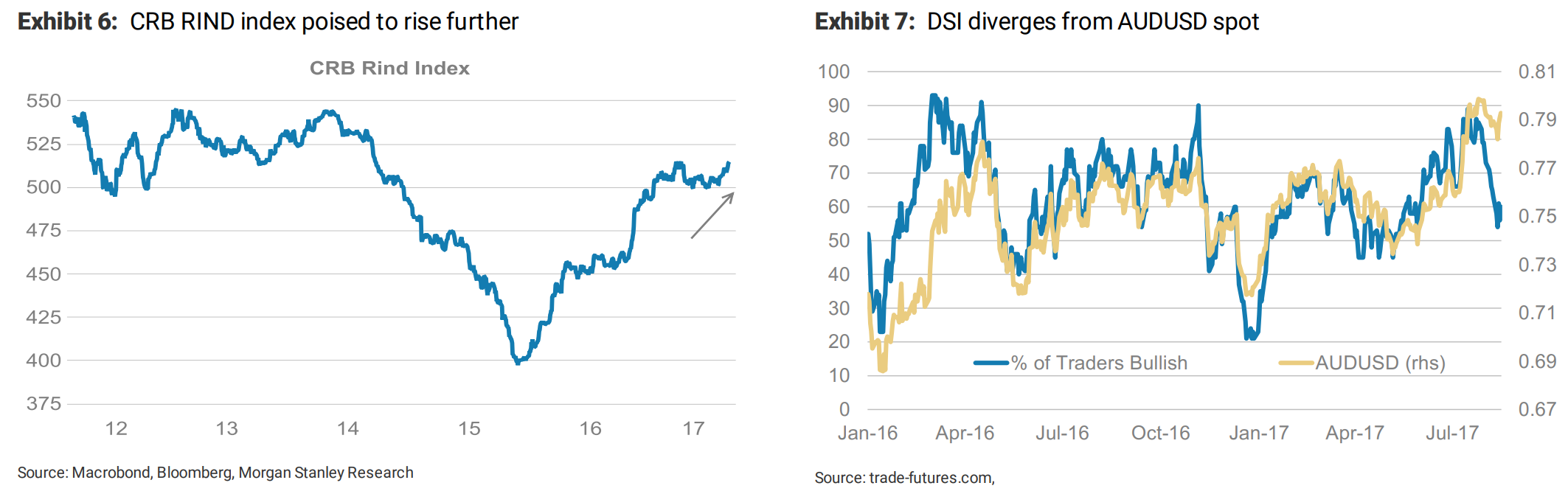

Commodity price strength has come on the back of better global demand and China reducing excess capacity. We have often cited the CRB RIND index which has been increasing again as of late (Exhibit 6). We prefer the RIND as it excludes speculative forces and marks the underlying trend. Commodity reflation supports commodity producers via the terms of trade channel. We view this as a likely explanation as to why AUD has been supported despite declining speculative sentiment (Exhibit 7).

I’d like to know what the DSI measures. Terrific correlation there. It’s not forex traders, which are long AUD on COMEX.

Advertisement

In short, commodity prices are keeping the currency range high at the moment while US political risk is pushing it around day-to-day via the USD. The RBA is still on sidelines.

My view remains that there is good risk of one more spike higher as the Fed under-delivers on tightening expectations.

But still substantially lower next year as China slows.

Advertisement

David Llewellyn-smith is Chief Strategist at the Macrobusiness Fund, which is currently substantially allocated into international assets. If you want to get your money offshore to catch any downdraft in the Australian dollar then fill in your details below and we’ll be in touch.

The information on this blog contains general information and does not take into account your personal objectives, financial situation or needs.

David Llewellyn-Smith is Chief Strategist at the MB Fund and MB Super. David is the founding publisher and editor of MacroBusiness and was the founding publisher and global economy editor of The Diplomat, the Asia Pacific’s leading geo-politics and economics portal.

He is also a former gold trader and economic commentator at The Sydney Morning Herald, The Age, the ABC and Business Spectator. He is the co-author of The Great Crash of 2008 with Ross Garnaut and was the editor of the second Garnaut Climate Change Review.