By Gareth Aird, Senior Economist at CBA:

Key Points:

- The RBA has shaved a little from their near-term growth forecasts while medium-term projections are broadly unchanged.

- Headline inflation forecasts have been nudged up while core inflation forecasts have been left unchanged.

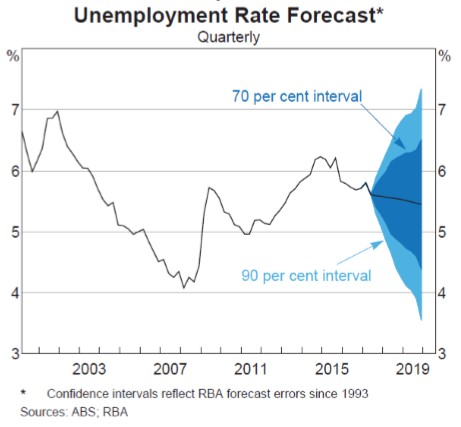

- The RBA have a shallow downward trajectory for the unemployment rate that glides to 5½% by mid-2019.

- We have the RBA cash rate on hold at 1.5% throughout 2017 and well into 2018.

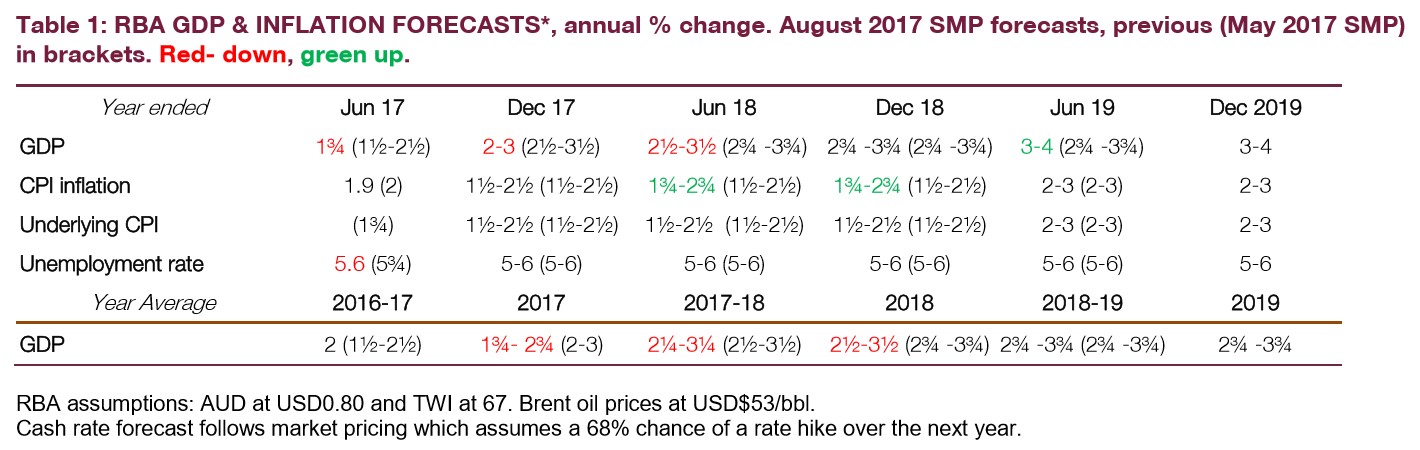

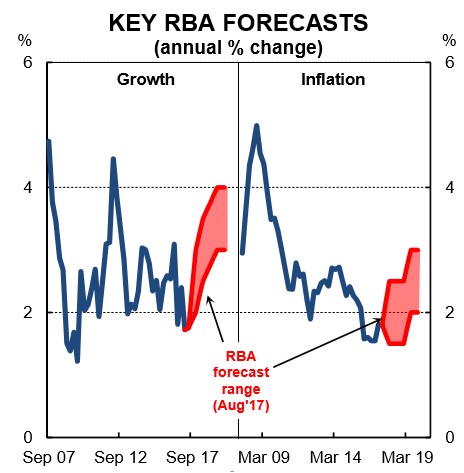

The RBA’s updated forecasts are consistent with policy on hold over the rest of 2017. The Bank expects growth to lift over the next few years to an above-trend pace. And while core inflation is forecast to be close to 2% in H2 2017 (a touch under on the Bank’s chart), the RBA sees headline inflation tracking in their 2-3% target band. Optimism around the recent strength in employment growth is tempered by a “subdued” outlook for wages growth. As such, we think that the Bank retains a neutral bias in today’s Statement on Monetary Policy (SMP).

The Bank has downwardly revised their near term GDP forecasts due to the softer than expected QI which was negatively impacted by weather. Looking at the Bank’s through the year forecasts implies that the pace of growth picks up to 2% by year end and 2¾% by Q2 2018. Positive contributions to come from LNG production, consumption, infrastructure spend and a lift in non-mining investment. The RBA notes that the stronger AUD has had a “modest dampening” effect on the growth forecasts. In summary, the Australian economy would be deemed to be in good shape if the RBA’s growth outcomes can be achieved. The forecasts look reasonable to us but the risks are to the downside.

Core inflation forecasts haven’t budged, but the expected trajectory for headline inflation has inched higher due to the lift in utilities prices. There is nothing in the inflation forecasts to suggest that policy will be tightened over the next year. We think that at the very least the RBA would need to upgrade its core inflation forecast to even entertain the idea of a rate rise.

We note the change in language from the RBA on the labour market that signals the Bank is clearly happy with developments. The RBA states that leading indicators of the labour market point to, “solid employment growth” over H2 2017. Here the emphasis is on solid and suggests that the RBA considers the recent strength in the labour market as genuine and that it will continue over the year. As a result, some mild downward pressure is expected to be applied to the unemployment rate.

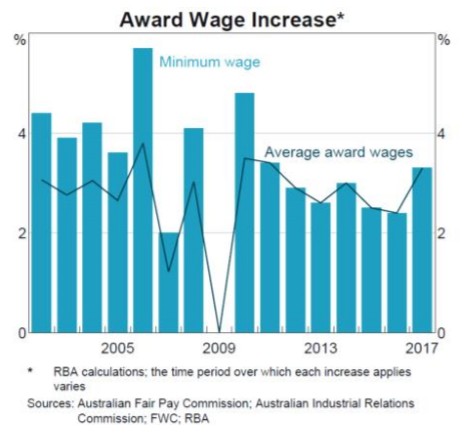

On wages, the RBA devoted “Box C” to a discussion on the 2017/18 minimum wage decision. The upshot is that it should contribute 0.2ppts to growth relative to its contribution in 2016/17. We have a similar view to the RBA on the outlook for wages growth. Namely that it has reached a bottom and should pick up gradually from here. That said, the process will be slow because there is still plenty of slack in the labour market. As a result, we think that the RBA’s outlook for wages growth is more plausible than the optimistic wages forecasts underpinning the 2017/18 Federal Budget.

In summary, it looks like more of the same from a monetary policy perspective over 2017. Rates will stay on hold until wages growth and core inflation are on a sustained upward trend. That is some way off and in our view that means that policy is likely to be on hold until late 2018.