■ From market darling to chump change: Precedents of banks experiencing governance crises suggest that a peer group NTA multiple de-rating of 10- 20% is plausible (implying a CBA share price of A$74–$81), and that the issue can manifest itself in the share price for an extended period (two years for NAB); CBA’s peer group NTA multiple de-rating to date has been 8%. We reduce our CBA price target from A$89 to $80 with an unchanged NEUTRAL rating on the stock to reflect this de-rating risk.

■ We have examined precedents of governance crises within banks (National Australia Bank, Wells Fargo), for insights as to the possible implications for share rating and subsequent remediation actions taken.

■ Next news: 1) 3Q16 trading update 8 November; 2) AGM 16 November; 3) New CEO appointment (by the end of FY18E). The CBA AGM could be a key catalyst inasmuch as, following CBA’s first strike on its remuneration report in 2016, a possible second strike in 2017 (i.e. a “no” vote of 25% or more on the remuneration report) would prima facie see shareholders vote at the same AGM to determine whether all directors need to stand for reelection (if this “spill” resolution passes with 50% or more of eligible votes cast, then a “spill” meeting takes place within 90 days). We see the CEO appointment as critical to any 12-month view on the stock (timeframe for announcement, credibility of the appointment).

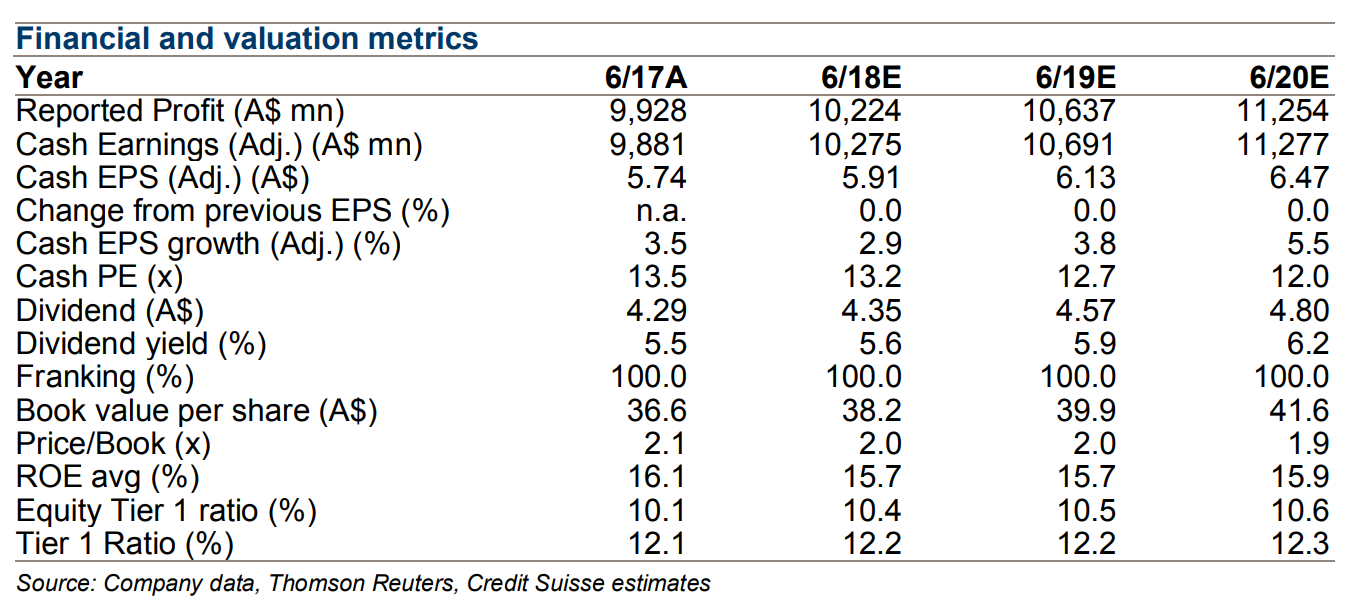

■ Valuation: CBA currently trades on 13.1x 12-month prospective earnings (3% premium to the major banks vs. a 13% four-year average premium) and a corresponding book multiple of 2.2x. CBA is our least preferred major bank exposure, and our NEUTRAL rating reflects our view that the stock’s multiple remains constrained by governance and control issues, which will take some time to resolve. Key downside risks include adverse turning of the credit cycle and adverse changes to regulation.

An ex-growth utility with a high payout ration exposed to an asset bubble and skyrocketing regulatory risk.

David Llewellyn-Smith is Chief Strategist at the MB Fund and MB Super. David is the founding publisher and editor of MacroBusiness and was the founding publisher and global economy editor of The Diplomat, the Asia Pacific’s leading geo-politics and economics portal.

He is also a former gold trader and economic commentator at The Sydney Morning Herald, The Age, the ABC and Business Spectator. He is the co-author of The Great Crash of 2008 with Ross Garnaut and was the editor of the second Garnaut Climate Change Review.