Quick chart from the Wall Street Journal / BMI overnight asking the question: Are energy stocks undervalued?

The answer is no. No, they aren’t.

And even if oil stocks were undervalued this is precisely the wrong valuation chart to look at.

I’m not saying the Price to Book ratio shown above won’t rise – but there are two ways this can happen:

- The share prices of oil stocks can rise

- The book value of oil stocks can be written down

My bet is that the second will be larger than the first.

Price to book gives you an indication of break-up value – how much value is in the balance sheet.

But resource companies are not like other companies. We are not talking about factories or offices or vehicles where there is an alternate use and the assets can be sold. Assets in the oil and gas sector are largely rigs, pipelines, infrastructure to oil fields etc. They are worth whatever cash they generate and if an oil field isn’t generating cash, the value of pipelines and roads leading to that oil field are going to be close to zero.

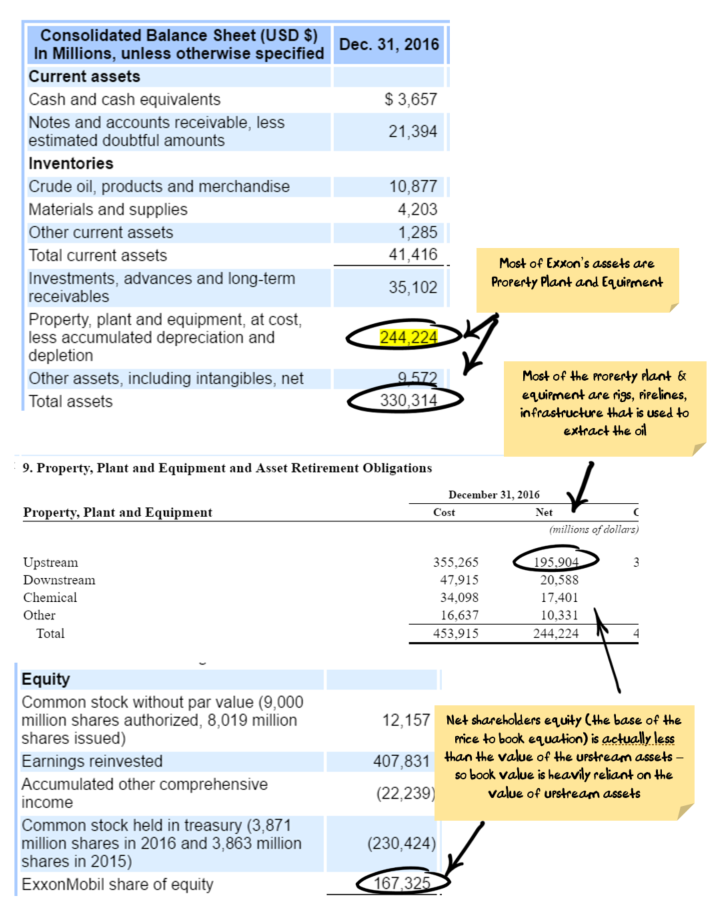

Let’s look at the largest stock, Exxon as an example – keeping in mind that Exxon is an integrated oil company and so actually does have other industrial type assets like refineries and chemical plants which means Exxon “should” be in a better position than the pure play oil companies:

Source: Company, Nucleus Wealth

Given the balance sheet above, key the question is how does Exxon value these upstream assets in its balance sheet? The same way other oil companies do – as a discounted cashflow based on internal oil price assumptions.

You would think that with the oil price falling from $100 to $50 there must have been a lot of writedowns over the last three years.

You would be wrong.

The oil price halved, and Exxon faced lots of pressure to write down its assets. Finally (almost 3 years after the fall) Exxon wrote down its assets by $3.3b – i.e. less than 2%.

Now Exxon is one of the worst, but the others aren’t that much better. And Exxon is by far the largest stock in the index – around 25% of the price to book in the Wall Street Journal chart above is directly related to Exxon.

So, if you want to buy oil stocks because you think the oil price will rise, then I will respectfully disagree but I’ll understand your decision.

If you want to buy oil stocks merely because the price to book value is low then the word “respectfully” no longer applies.

Damien Klassen is Chief Investment Officer at the Macrobusiness Fund, which is powered by Nucleus Wealth.

The information on this blog contains general information and does not take into account your personal objectives, financial situation or needs. Damien Klassen is an authorised representative of Nucleus Wealth Management, a Corporate Authorised Representative of Integrity Private Wealth Pty Ltd, AFSL 436298.