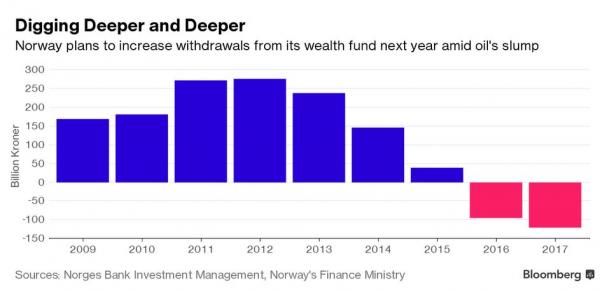

First world problems in a nutshell. You have to drawdown some of your savings for the very first time – a meager $11USD billion or so from your near $1 trillion sovereign wealth fund (SWF) – because lower commodity prices are taking big slugs out of your budget.

And then, and then – because you were soundly forecasting a 2.1% annual rate of return (ROR) for the next ten years on that fund, but realise that the low oil prices might be a secular shift, you consider shifting the ROR up to 2.5% by buying some more stocks…

Silly Norwegians, don’t they know thats obscenely risky? Why not do it the old fashioned way and let the household sector borrow to the moon, have your central bank go on a QE bond-buying spree and tighten that fiscal budget by not spending on infrastructure or providing incentives to shift to a carbon neutral economy?

Advertisement

By the way, here’s what happens when you convert your vast, but eventually non-renewable mineral wealth into savings instead of the ‘Strayan method of pissing it up against a wall, via Bloomberg:

“Norway’s $970 billion wealth fund has been ordered to raise its stock holdings to 70 percent from 60 percent in an effort to boost returns and safeguard the country’s oil riches for future generations. Any short-term view on growing risks will play little part, according to Trond Grande, the fund’s deputy chief executive.

‘We don’t have any views on whether the market is priced high or low, whether bonds and stocks are expensive or cheap,’ he said in an interview after presenting second-quarter returns in Oslo on Tuesday. The decision to add stocks ‘was made at a strategic level, on a long-term expected excess return that we’re willing to take risk to achieve. And parliament has said that they wish to spend some time to phase in that increase.’”

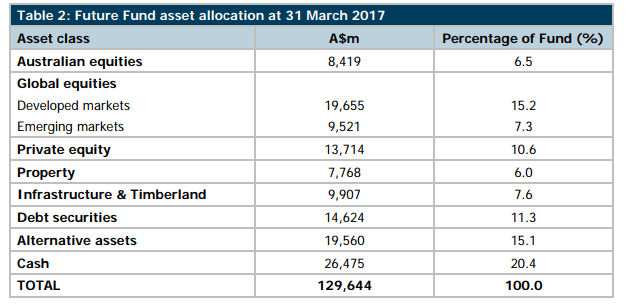

The composition of the Norwegian SWF fund is approximately 65% stocks, 32% bonds and 2.5% in property. Australia’s own SWF, the Future Fund (which is for funding public service pensions) has approx. $130 billion spread across the following allocation:

Advertisement

Quite a different composition at about 55% stocks/alternatives, and quite a lot of cash. And the Future Fund is doing a lot better in terms of nominal performance, returning 7.7% per annum since inception.

Imagine the returns if it had proceeds from the “once in a century” mining boom instead of the losing sale of Telstra?