by Chris Becker

A mixed day in Asia after the solid response to the US GDP print overnight and the subsequent surge in USD that has seen the Yen selloff and Japanese bourses rise in result. Local releases from Japan, China and Australia added some volatility to currencies but not any game changers.

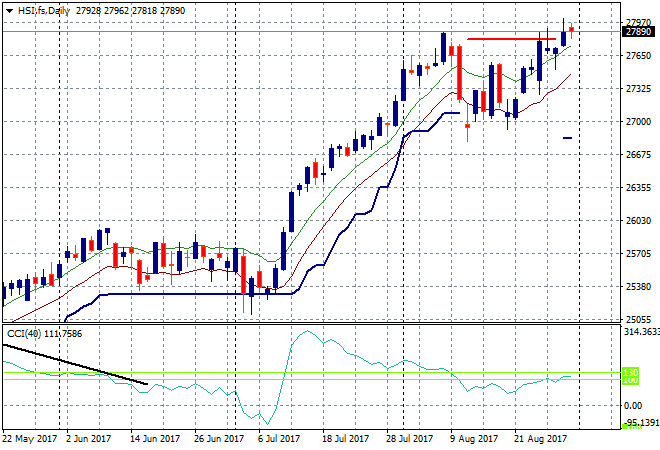

In mainland China the Shanghai Composite closed down only a few points at 3360 extending its pause here after the big breakout recently. The Hong Kong based Hang Seng Index has sold off instead, down 0.6% to be back below 28000 points. This is still above the previous daily high and a welcome entry point for further longs:

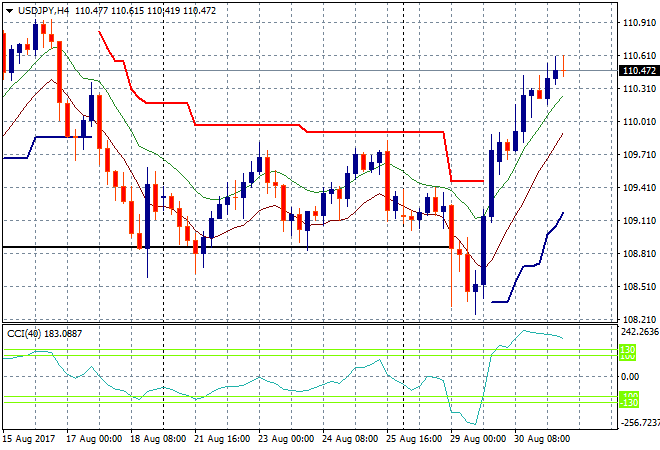

Japanese stocks continued to rally on the weaker Yen. The Nikkei lifted nearly 0.75% again to close at 19646 points, still remaining below the very firm resistance at the 20,000 point level but recovering slowly. The USDJPY pair remains above the 110 handle with the next target at 110.90:

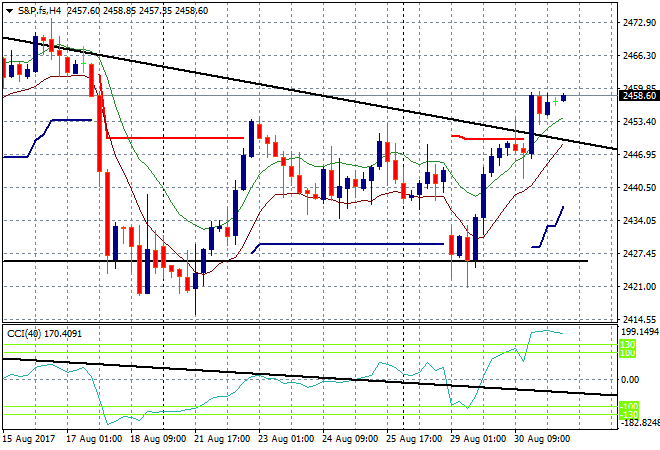

S&P futures are up looking to break above the 2459 point level:

The ASX200 did a lot better today, getting back above the 200 day moving average by lifting 0.7% to 5714 points.Both banks and iron ore stocks lifted in unison here, while Harvey Norman dropped over 7% even after its record result.

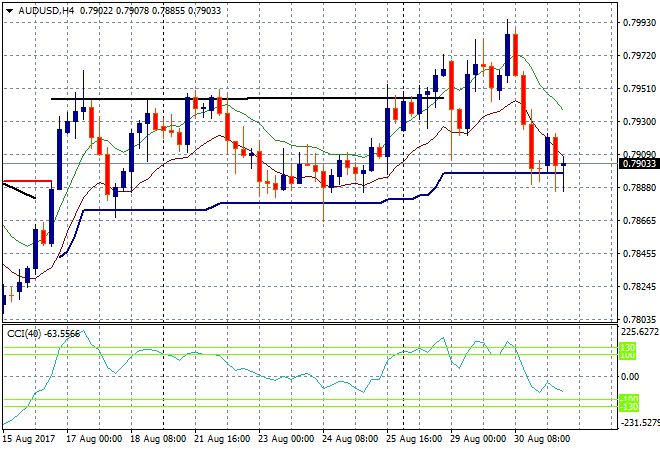

The Aussie dollar was pushed slightly lower on the back of the capex figures and Chinese PMI results, almost reaching the 79 handle. There is still a potential for a fall here below trailing ATR support at the 78.80 level:

The data calendar continues with 3 big releases tonight: German unemployment, European CPI and US Personal Consumption Expenditure.