by Chris Becker

Asian markets are in a flux as traders wait for more staid and stable speeches from Jackson Hole later in the week. The Aussie dollar put in a new weekly low as a result of the risk off mood while the local bond market rallied in response to the Treasury rally overnight. Its looking like another week to write off for local stocks too, with a failure to gain traction once more.

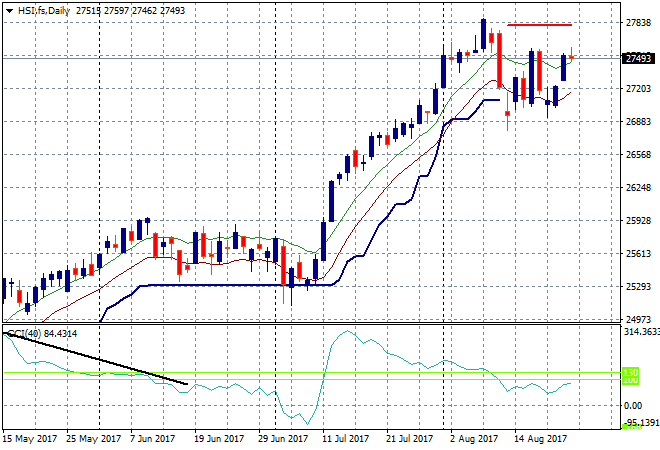

In mainland China the Shanghai Composite was steady going into the lunch break but has sold off this afternoon, down 0.5% to 3271 points as it continues to reject key resistance at 3300.. The Hong Kong based Hang Seng Index reopened after yesterday’s typhoon and was the only bright spot in Asia, lifting approx. 0.4% to 27518 points. This doesn’t quite match the previous high in the bounce back, but the market remains positive on all momentum readings:

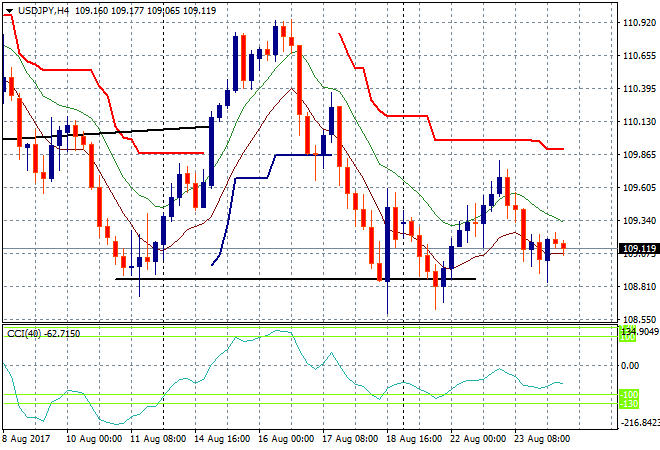

Japanese stocks took the brunt of the poor mood, with volumes very thin. The Nikkei closed 0.4% lower taking back all of yesterday’s gains and then some to finish at 19353 points, still confirming the very firm resistance at the 20,000 point level. The USDJPY pair is holding around the 109 handle after its slump overnight on the weaker USD, providing the headwind to local stocks. The next level here is obvious weekly support at the 108.80 level:

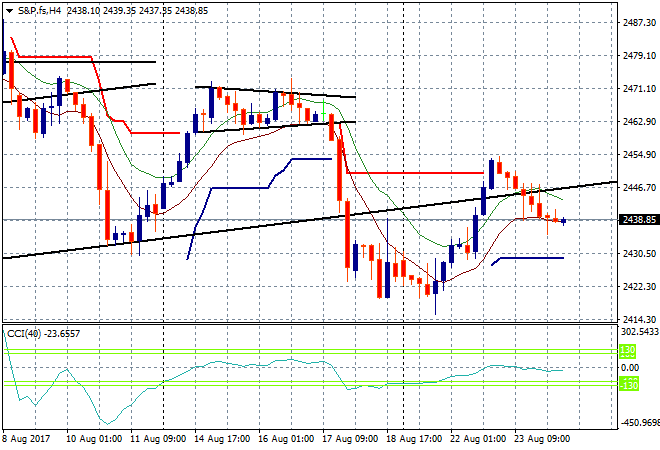

S&P futures are off slightly, as are Eurostoxx, both down around 0.3% or so as we head into another crucial session – will the buy the dip crowd help here?

The ASX200 actually finished in the green, but only just, up 0.15% to 5745 points after gapping down significantly at the open. Again, we see a close just above the 200 day moving average, but no significant breakouts including in any of the main sectors. And again we see iron ore and other commodity stocks rally while financials dragged the rest of the bourse back.

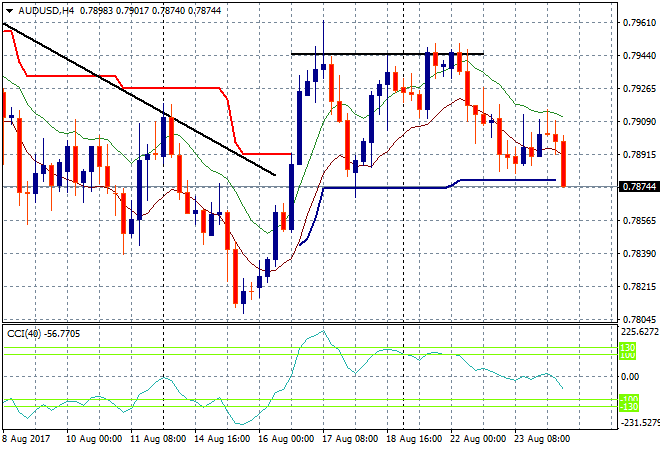

The Aussie dollar has fallen to a new low for the week and pushed through four hourly support at the 78.70 level in a risk off breakdown. If The City confirms this move later tonight, then its off down to the 78 handle:

The data calendar tonight includes two important releases to watch out for, first UK 2Q GDP print and then weekly initial jobless claims in the US.