by Chris Becker

Following last night’s tepid lead from overnight markets Asian traders are looking at each other and wondering if they should continue on with the bounce from Monday, given the seemingly reduced risk over the Korean peninsula. Stock markets were mixed with only the ASX200 putting on meaningful gains with currencies relatively stable awaiting tonights FOMC minutes.

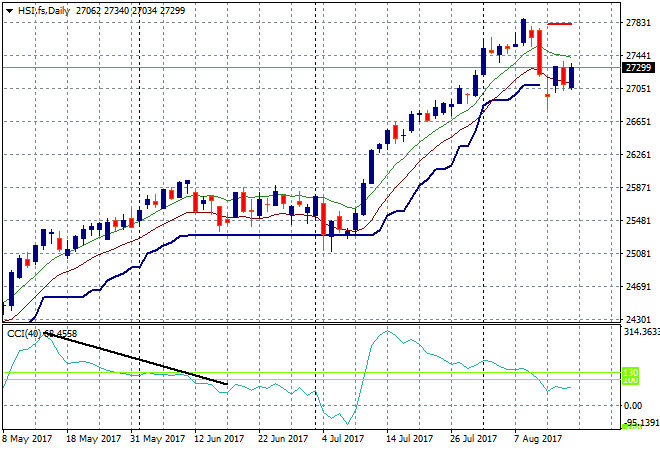

In mainland China the Shanghai Composite has slipped slightly, currently down a few points to 3247, keeping temporary support at bay above the 3200 point level. The Hong Kong based Hang Seng Index is doing much better, up 0.5% to 27362, staying well above daily support at 27000 points. I mentioned yesterday this bounceback has been weak so far and the Hang Seng needs to get above the high moving average band at 27450 or so soon to arrest this dip:

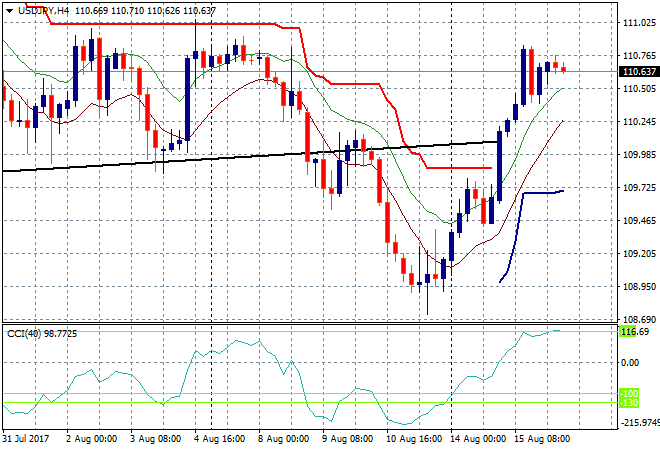

Japanese stocks are very stable, retreating only a few points even as the Yen remains weak against USD. The Nikkei closed about 0.1% lower, remaining at 19729 points, still well below the 20,000 point level. The USDJPY pair is pausing here after its big recent runup, gravitating around a midpoint of control at the 110.60 level.The next resistance level to beat is the 111 handle to make a three week high, but that will all depend on the language of the Fed minutes:

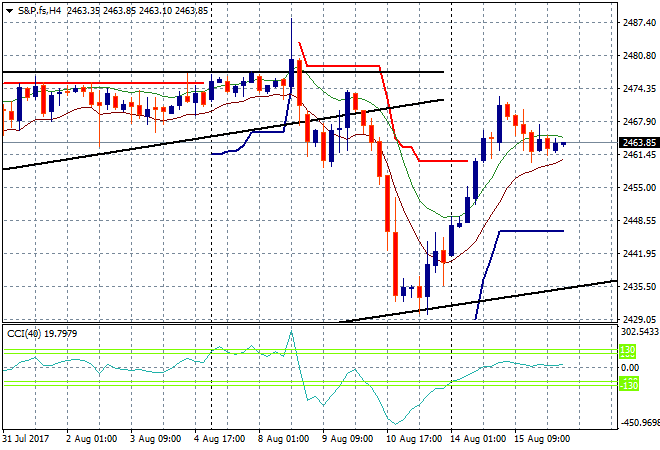

S&P futures are steady here after the minor fall last night:

The ASX200 had a very volatile starting session before finding momentum, shooting up another 0.5% higher, to finish at 5785 points. This was a nice broad rally as CBA went ex-dividend, the rest of the banking sector lifting strongly with Origin up 5.5% even as it announces a mammoth write-off of its LNG export project.

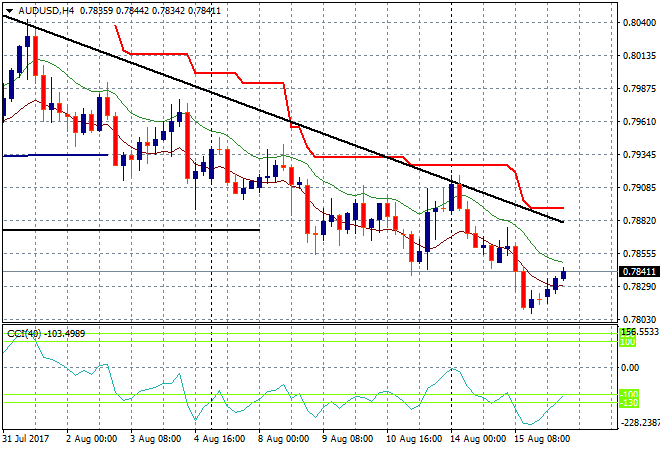

The Aussie dollar has bounced back slightly after its fall yesterday, bouncing off the 78 handle through to the 78.40 level. This looks to be a temporary move up to the high moving average but not to the downtrend daily line, where its likely to come under pressure later tonight:

The data calendar continues tonight with Italian and EZ wide 2Q GDP, but all eyes will be on the FOMC minutes from last meeting.