by Chris Becker

The bounce continues across Asia with green across the board for stock markets as the USD rallies on the back of renewed vigor for interest rate rises. The Korean situation has eased in terms of tension, giving markets respite as they follow the great start to the week from transatlantic markets overnight. Bonds have also seen a mild selloff as risk returns to stock to party!

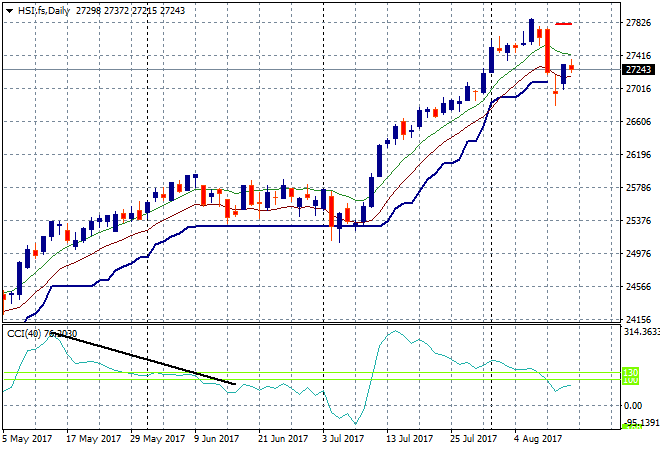

In mainland China the Shanghai Composite has continued its comeback although its slightly deflating going into the close, up 0.2% to 3243 points, keep temporary support at bay at the 3200 point level. The Hong Kong based Hang Seng Index is doing much the same, also up 0.3% and staying above daily support at 27000 points. So far this is a weak move and the bourse needs to get above the high moving average band at 27400 or so to arrest this dip:

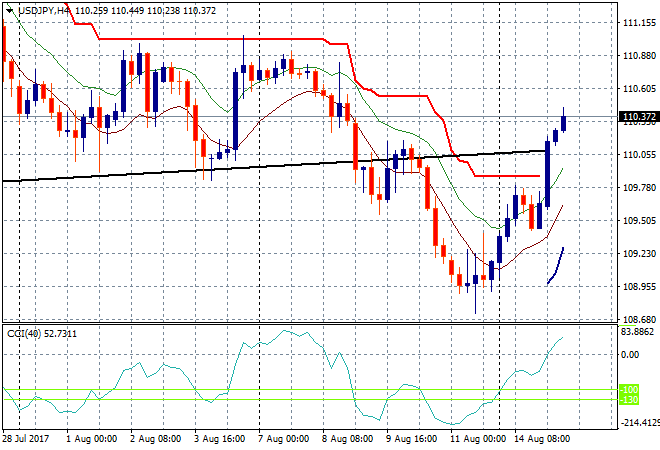

Japanese stocks are the best in the region, catching up to everybody else’s gains as the Yen drops significantly against USD. The Nikkei closed over 1.2% higher, taking back yesterday’s losses but still just below the 20,000 point level. The USDJPY pair is roaring higher on the interest rate comments from the Fed, now powering through the 110 handle and taking out four hourly resistance. The next resistance level to beat is the 111 handle:

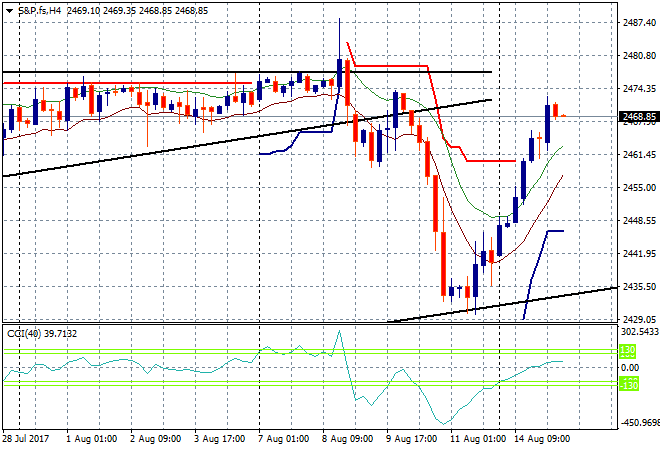

S&P futures are again building as risk returns to the table, almost taking it back to the pre-dip highs:

The ASX200 had another strong start, bid from the open before losing heat in the afternoon to finish up 0.5% higher, to be at 5757 points. The RBA minutes took the wind out of the sails, with CBA still under pressure and iron ore stocks losing ground.

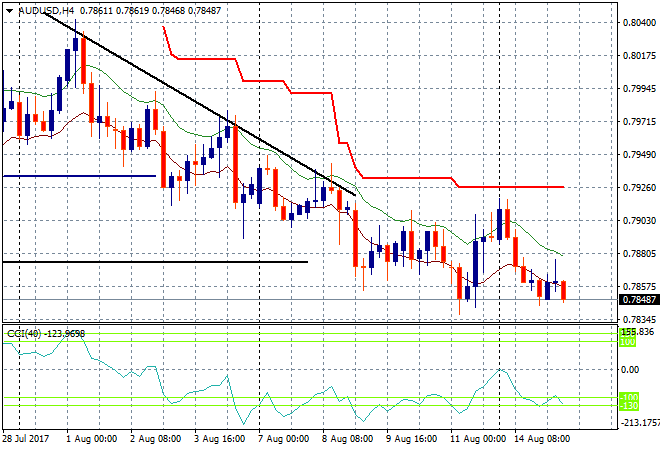

The Aussie dollar reacted meekly to the neutral RBA minutes and has now sold off slightly going into the European sessions. Price is just on the Friday low and looks set to break here below 78.40:

The data calendar continues tonight with German 2Q GDP and UK July CPI prints followed by US advanced retail sales.