by Chris Becker

Stocks lifted all across Asia as a wave of risk taking takes hold from bullish economic prints and firm earnings reports. The USD remains under pressure keeping Yen elevated but Japanese stocks rallied nonetheless on solid income reports from its major banks. Commodities are driving this risk rally as well with copper, iron ore and oil all putting in new daily highs.

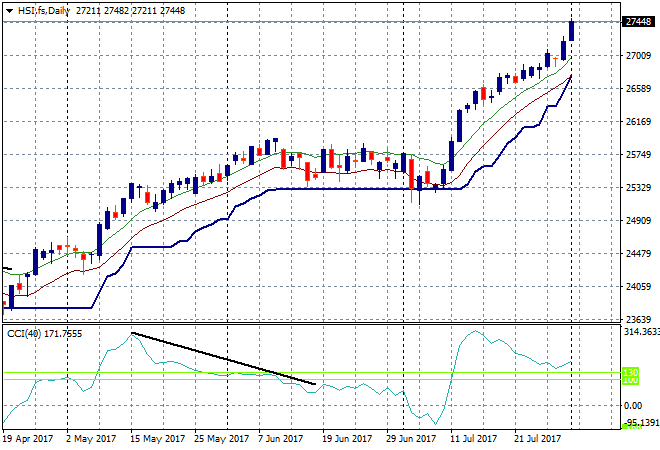

In mainland China the Shanghai Composite is up 0.4% to 3286 points as it reaches for the next obvious resistance at the 3300 point level. The Hong Kong based Hang Seng Index is again doing better, up 0.6% after its recent breakout move above 26,000 points and accelerating away! This is setting up for a lovely retracement, surely?

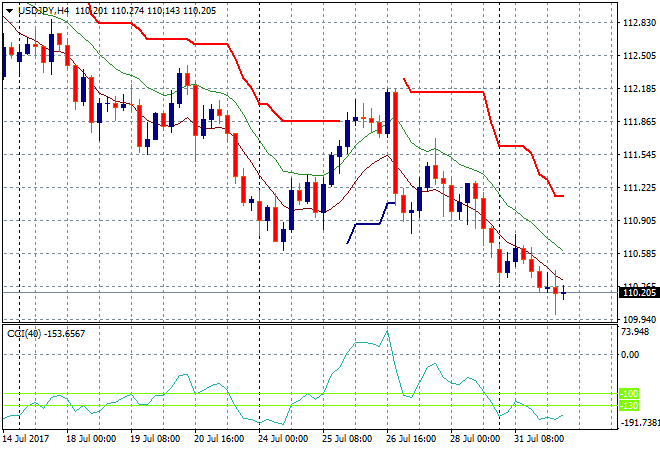

The Nikkei finished 0.3% higher to 19985 points, still below the psychological important 20,000 point level which is firming everyday as significant resistance. The USDJPY pair is slowly melting down after briefly holding here at the 110.50 level. It could make a new low here again tonight on the back of the ISM print, so watch out:

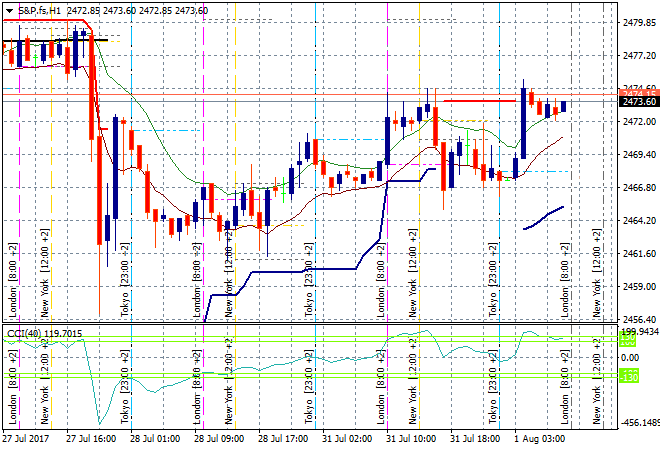

S&P futures are slowly lifting and building returning back to the previous session highs with some very big earnings reports tonight:

The ASX200 had a great session, closing up nearly 1% higher to 5772 points in a broad move across all sectors, seemingly ready to breakout above its recent funk, after respecting the 200 day moving average as support. Commodity players were the biggest movers, again, with BHP up 1.2% and Whitehaven Coal up 7%

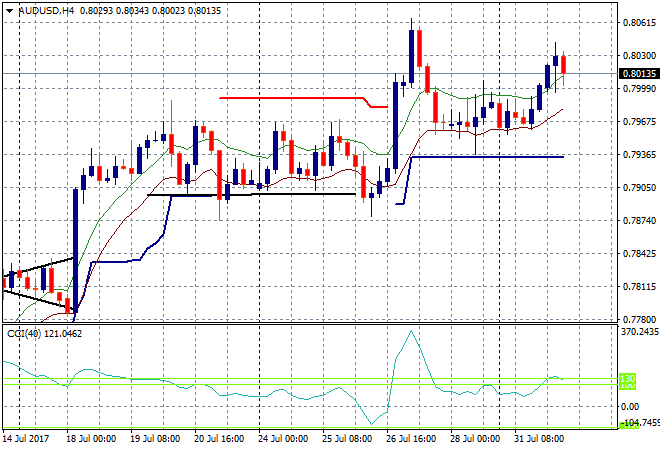

The Aussie dollar was basically unchanged following the RBA meeting where the boffins at Martin Place held fire. Before the release the Pacific Peso lifted up and through 80 cents and retraced only slight thereafter. The very short term target to reach here is last week’s intrasession high at 80.60:

The data calendar continues tonight with some really big hits, starting in Europe with German unemployment and 2Q GDP, while in the States its the personal consumption expenditure (PC) and July ISM prints.