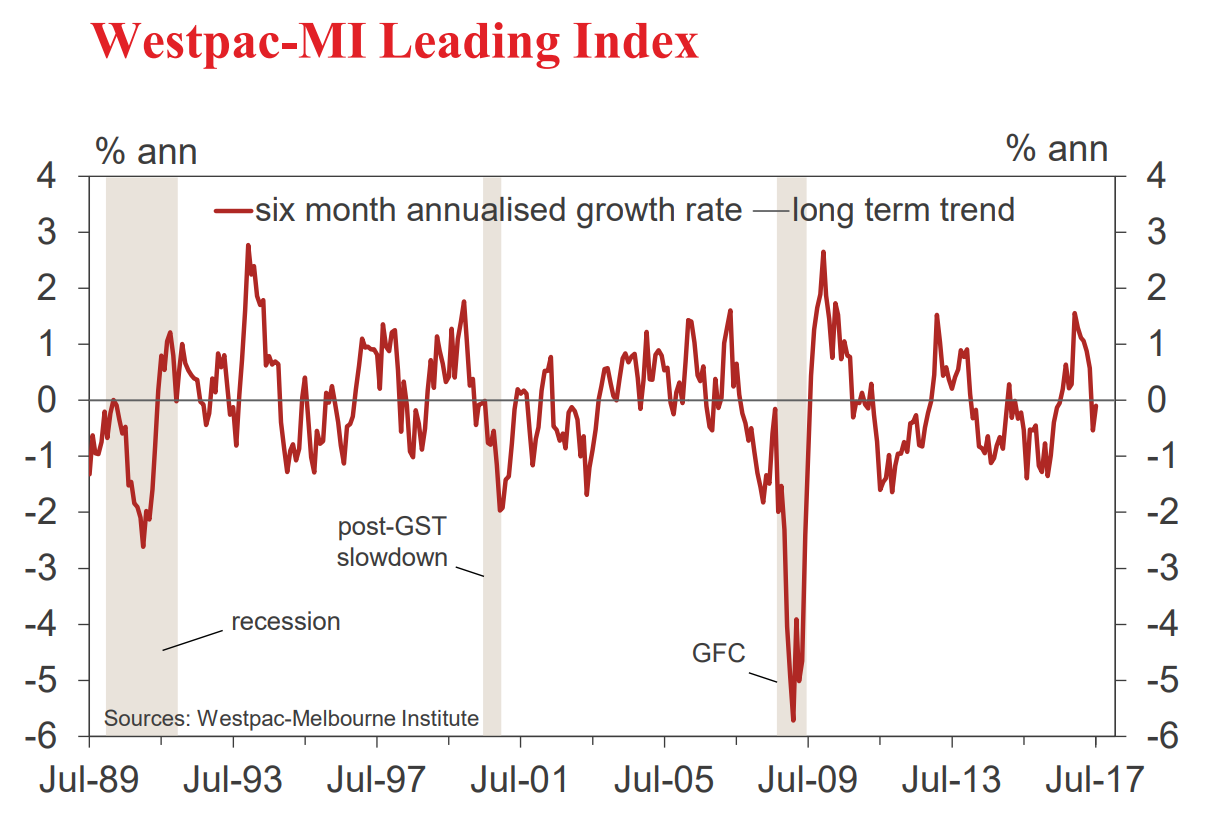

• The six month annualised growth rate in the WestpacMelbourne Institute Leading Index, which indicates the likely pace of economic activity relative to trend three to nine months into the future, rose from –0.54% in June to –0.10% in July.

Despite the improvement in the growth rate it remains negative for a second consecutive month pointing to below trend growth momentum and a sharp turnaround from strong positive, above trend reads at the start of the year.

While the Index only gives us a glimpse of the likely momentum in the first few months of 2018 it currently seems to be more consistent with our own view of the likely growth environment in 2018 than the forecast recently released by the Reserve Bank which is pointing to above trend growth in 2018 at 3.25%. Westpac is currently forecasting growth of 2.5% in 2018. Trend growth is generally assessed as 2.75%.

The Leading Index growth rate has slowed from 1.11% above trend in February to 0.10% below trend in July, a deterioration of 1.21ppts. Two components account for almost all of the reversal: commodity prices (–1.63ppts) and yield spread (–0.43ppts). After surging 42% over the second half of 2016, Australia’s commodity prices (Reserve Bank Commodity Price Index) have fallen 16% in the first seven months of 2017 (in AUD terms).

Over the same period, the yield spread (10 year bond rate minus 90 day bank bill rate) has moved through a sharp widening (100 basis points over the second half of 2016) to a modest narrowing (7 basis points). The spread captures financial markets’ assessments of the economic outlook both locally and abroad.

The contribution from other index components has been more mixed.

On the positive side, the index growth rate has been boosted by: dwelling approvals (+0.39ppts); aggregate monthly hours worked (+0.27ppts); US industrial production (+0.25ppts); and Westpac-MI UE index (+0.14ppts). These improvements have been partially offset by bigger drags from the Westpac-MI CSI expectations index (–0.11ppts) and the S&P/ASX 200 (–0.1ppts).

The net impact of international components (commodity prices; yield spread; US industrial production) has swung from a peak of adding 1.5 percentage points (the peak) to the Index’s growth in December 2016 rate to subtracting 0.5 percentage points in July 2017.

On the other hand the domestic components (the remaining five components) have moved from flat in December 2016 to now adding 0.37 percentage points to the growth rate.

The Reserve Bank Board next meets on September 5. There is no doubt that the Board will continue to leave the cash rate on hold. The more interesting question is whether, as expected by markets and signalled by consumers’ responses in the Westpac-Melbourne Institute Consumer Sentiment survey, the RBA will raise rates next year. High business confidence and improving employment conditions along with the Bank’s own upbeat growth forecasts support the case for higher rates. On the other hand we continue to see evidence of a downbeat consumer and signs that the housing markets are set to slow under the weight of stretched affordability.

It is interesting that in the Bank’s Board minutes which were released on August 15 it sounded less confident about achieving its inflation target. We concur and, consistent with below trend growth, expect that rates will remain on hold through 2018.

David Llewellyn-Smith is Chief Strategist at the MB Fund and MB Super. David is the founding publisher and editor of MacroBusiness and was the founding publisher and global economy editor of The Diplomat, the Asia Pacific’s leading geo-politics and economics portal.

He is also a former gold trader and economic commentator at The Sydney Morning Herald, The Age, the ABC and Business Spectator. He is the co-author of The Great Crash of 2008 with Ross Garnaut and was the editor of the second Garnaut Climate Change Review.