From Jess Irvine today:

I remember attending an economics conference in Canberra in late 2011 where two esteemed Australian economists, Bob Gregory and Ross Garnaut, both warned Australian households to brace for a decline in living standards at the end of the mining boom.

…In a 2012 paper, Gregory explained: “In peace time, and over such a sustained period, Australia has never experienced such a large increase in income relative to so many other advanced economies. It now appears, following current national accounting practices, that Australian per capita income levels have increased about 25 per cent relative to the United States and now exceed US levels.”

Why? Because the benefits of the mining boom were not quarantined in the Pilbara. Far from it.

A higher Australian dollar – reaching parity and more against the Greenback – helped spread the benefits of the boom through cheaper imports. We stacked our homes with new furniture, gadgets and flat screen TVs, on which we watched each other renovate and extend our homes.

Meanwhile, wages growth soared; not just for those in hard hats and steel-capped boots but also for the army of accountants, lawyers and deal-makers who serviced the mining sector. And the retail staff who sold all the flat screen TVs. And the hospitality staff who sated our Masterchef-inspired taste buds.

And all the while, tax cuts rained down on us from the nation’s capital.

But that mining boom is now well and truly over. Commodity prices peaked in 2011 and while exports are now contributing to growth, much of the benefit of that flows to overseas owners.

The hangover of the mining boom has proven more painful than most economists anticipated.

The much touted “transition” from mining to other sources of demand has disappointed. Record low interest rates were supposed to fire up other parts of the economy. But they haven’t.

Why? Because in response to lower interest rates, Aussie households did what they’ve done every time interest rates have fallen in the past: they borrowed more.

Today, many households find themselves shackled to mortgages they thought they could finance with mining boom-era pay rises, which have failed to materialise.

It could be much worse, however.

Most of the mining booms in our history have ended in periods of rapid inflation and sharply rising unemployment.

We have avoided that fate. Our problem is, in fact, the reverse. Inflation is lower than expected and the jobless rate is falling.

The pain of adjustment is being felt almost entirely in pay packets.

Is that such a bad thing?

It is, in fact, exactly what several decades of economic reform hoped to achieve: a flexible economy, in which prices were liberated to respond to economic shocks so as to cushion their blow.

As one the few economists that did see it coming, I can only say that Jess Irvine is still driving in the rear vision mirror. The post mining boom adjustment is a process of working off the inflationary excesses of the boom to repair competitiveness. Wages weakness is to be expected as a part of that. But the adjustment can be managed to make that worse or better, fairer or less so. You can enact policies that aim to share the adjustment fairly by deflating externally with, let’s face it, very little risk of an inflationary breakout these days. Or, you can enact policies that aim to do it unfairly, by deflating internally, and protecting capital.

Just about every policy choice we’ve made has made it worse for wages and better for capital:

- no fiscal reform to boost productivity;

- no monetary reform to contain credit;

- no attempt to engineer a lower currency;

- sustaining stunning levels of immigration into over-supply.

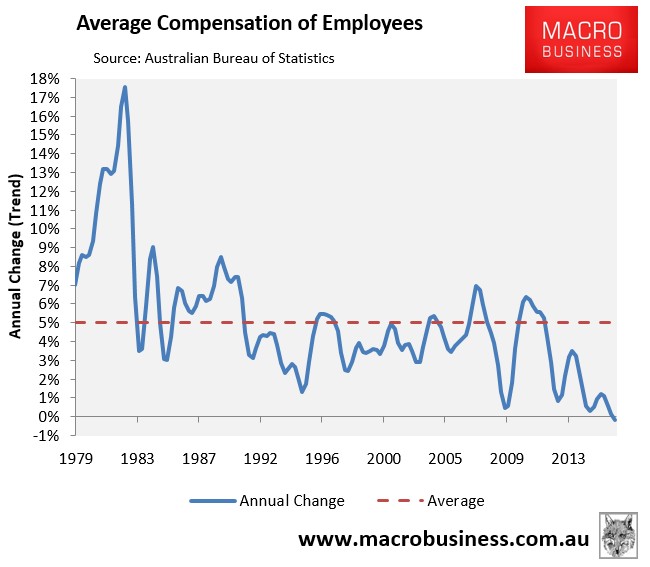

The upshot of this mismanagement is that firms such as Jessica Irvine’s employer, Domainfax, have benefited greatly from policy-support for growing the pie at the aggregate level while average households have had their piece of the pie smashed. Hence today’s wages debacle is the worst in modern history, much longer and deeper than previous post-boom adjustments:

And it is not even half over:

In short, Ms Irvine is selling households a lemon to protect her own job.