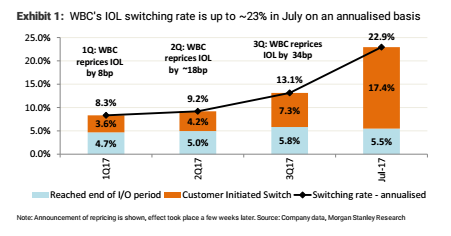

While Australian banks’ margin recovery is in the sweet spot in late 2017, today’s new data from WBC shows IOL switching could be playing out earlier than the market expects. This presents downside risk to margins in 2018.

Interest only switching is rising: WBC has more IOL(~50% of Australian mortgages) than other banks (~40%),and in today’s 3Q17 update it reported that ~A$20bn of IOLhas switched to paying P&I in FY17 to date. The annualised switching rate has risen from ~8 to 9% in 1Q/2Q to ~13% in 3Q17 and then to ~23% in July (first month of 4Q17). The key driver is rising customer initiated switching in response to three successive rounds of IOLrepricing, with the largest repricing of +34bp taking place in June/July.

The full text of this article is available to MacroBusiness subscribers

David Llewellyn-Smith is Chief Strategist at the MB Fund and MB Super. David is the founding publisher and editor of MacroBusiness and was the founding publisher and global economy editor of The Diplomat, the Asia Pacific's leading geo-politics and economics portal.

He is also a former gold trader and economic commentator at The Sydney Morning Herald, The Age, the ABC and Business Spectator. He is the co-author of The Great Crash of 2008 with Ross Garnaut and was the editor of the second Garnaut Climate Change Review.