Via Credit Suisse comes confirmation of what we’re seeing RMBS for household credit stress:

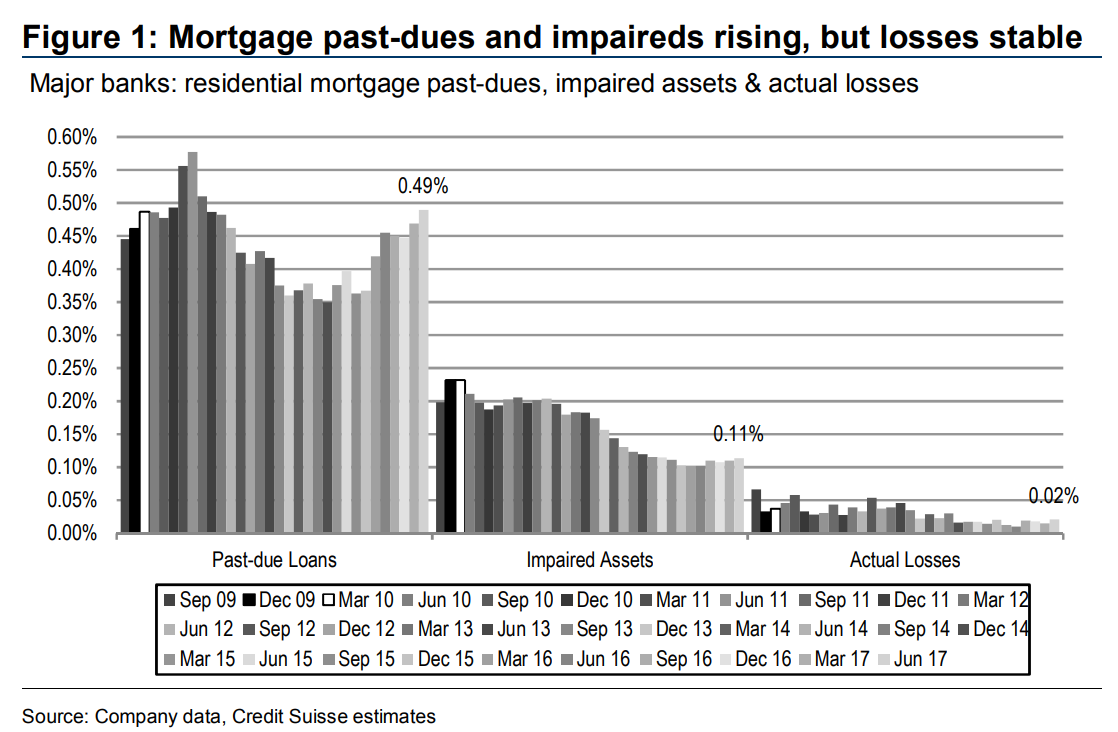

■ Mortgage & card past-due ratios and mortgage impaireds ratios rose in the latest quarter, with loss rates stable in mortgages but rising in cards. Whilst acknowledging seasonality, a slowing Western Australian economy, and residual impacts of Cyclone Debbie, mortgage past-due ratios in particular appear to be structurally rising. More general trends that we saw during the quarter were as follows: Impaireds: The impaireds ratio edged lower again by 1bp (to 0.27%) driven out of business (cards & mortgages impaireds increased); WBC was the lowest amongst the majors at 0.19%. Past-dues: The past-due ratio edged up higher again by 1bp (to 0.29%), driven out of mortgages and cards (business lower); NAB was lowest amongst the majors at 0.14%. Loss rates: Actual losses declined to 0.13% (0.19% sequentially), albeit loss rates in cards has been rising recently. Capital: Major bank equity Tier 1 ratios ranged from 9.70% (NAB) to 10.11% (CBA), with risk weights flat-to-declining (albeit mortgage risk weights were higher again at 25% vs. 24% sequentially: ANZ 26%, CBA 25%, NAB 27%, WBC 24%).

■ Our risk & capital report benchmarks the latest quarter Pillar 3 disclosures for each of the commercial banks (June 2017). For context, our major bank bad debt charge profile is: 0.21% FY16, 0.18% FY17E, 0.21% FY18E, 0.21% FY19E.

The full text of this article is available to MacroBusiness subscribers

David Llewellyn-Smith is Chief Strategist at the MB Fund and MB Super. David is the founding publisher and editor of MacroBusiness and was the founding publisher and global economy editor of The Diplomat, the Asia Pacific’s leading geo-politics and economics portal.

He is also a former gold trader and economic commentator at The Sydney Morning Herald, The Age, the ABC and Business Spectator. He is the co-author of The Great Crash of 2008 with Ross Garnaut and was the editor of the second Garnaut Climate Change Review.