Judith Sloan has a point today:

The National Electricity Market is on its last legs. What started off as a good idea has descended into a joke, with state governments increasingly going it alone.

…The NEM operates one of the world’s longest interconnected power system. It covers a total distance of about 5000km from Port Douglas in Queensland to Port Lincoln in South Australia, with 40,000km of transmission lines.

But herein lies one of the NEM’s weaknesses: it is a very long, weakly connected system which does not provide the ideal underlying conditions for the efficient and transparent operation of the market for electricity. The penetration of renewables, as well as their preferential access to the NEM, has made this weakness even more apparent. There is no doubt the theory is strong: a national electricity market should provide the basis for the lowest cost of provision of electricity while encouraging optimal investment. That the NEM has failed to do so carries a very heavy economic cost for the nation while imposing a burden on households and businesses.

…So why do I say the NEM is on its last legs? For starters, note that the NEM failure has nothing to do with privatisation. In fact, the NEM operated well after most government-owned electricity assets were sold. And note also that Queensland is experiencing considerable problems with electricity prices yet the assets there are largely still government-owned.

One central failing of the NEM is its inability to achieve one of its core functions: to oversee the reliability and security of the electricity system. The actions of a number of states are also undermining its operation; most particularly, South Australia. It is unsurprising politically that the South Australia government would react to the total power blackout and load-shedding that occurred in that state in the past 12 months. That South Australia now has the highest retail electricity prices in the world is not a badge of honour the Weatherill government happily wears.

…The Queensland government is also attempting to destroy the NEM by instructing one of its generators, but not the other, to bid low at peak times. Mind you, that government has been more than happy to reap the excessive dividends produced by the gaming of the system by these generators.

The NEM is indeed failing. The renewable transformation can be blamed if one discounts the existence of climate change and the need for Australia is contribute to the solution. But if one accepts that very likely truth then the argument collapses. There is nothing technically difficult about high renewables penetration for the NEM. The only question is how policy brings it about.

Australia’s chosen policy path was unremarkable. We elected to rely on abundant gas power generation to substitute for coal as the “transitional fuel” while renewables developed base load capacity in the renewable/battery killer app. By MB numbers that process will be complete in a remarkable five years as even coal becomes uncompetitive against the base load renewables charge.

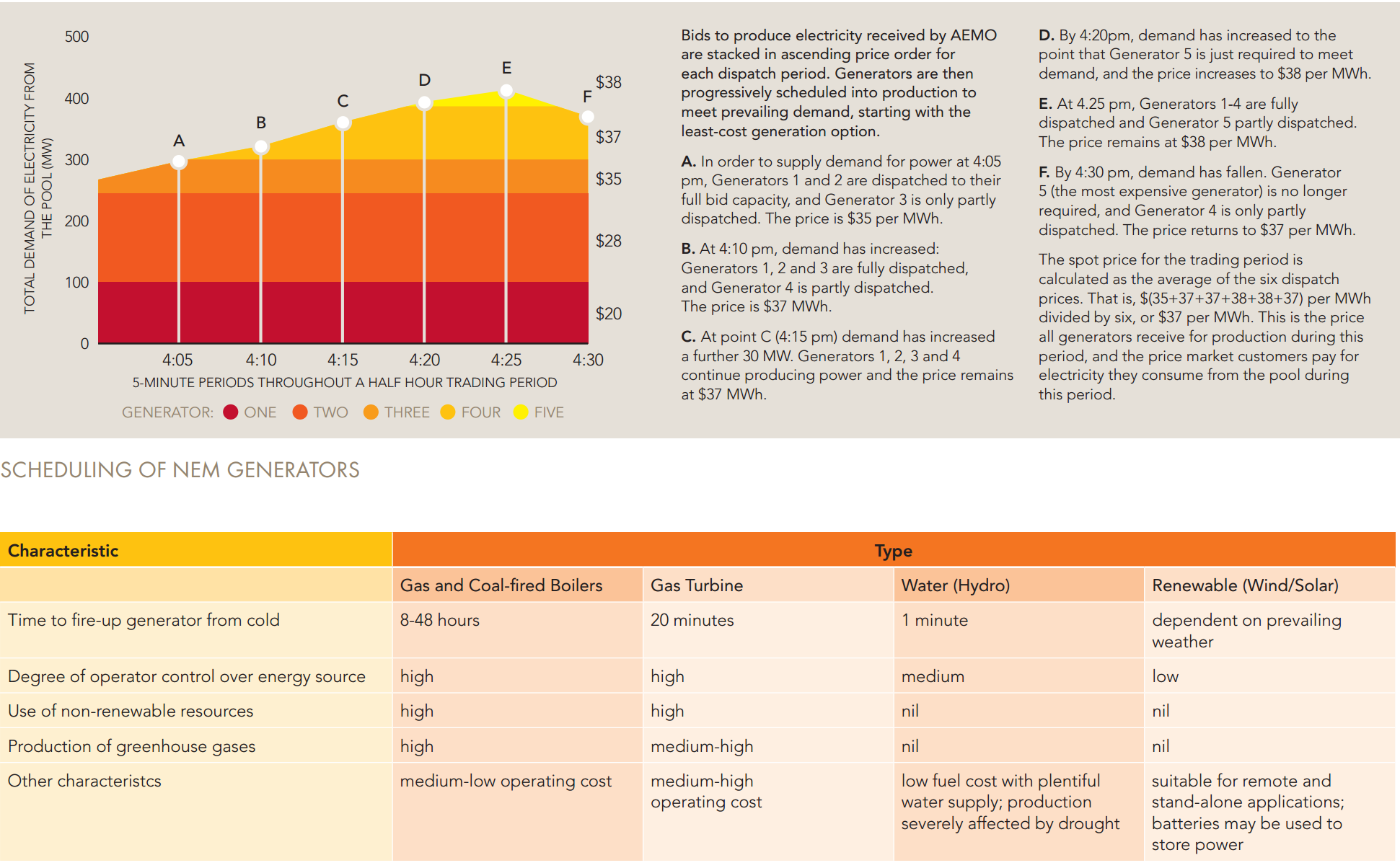

The only thing that went wrong with this path – despite all of the policy balderdash from both sides of parliament – was that Australia simultaneously sold off its gas reserves to others with the same basic idea. That allowed a gas cartel to rise and gouge the entire east coast economy. Given those reserves are all state-owned, if there is a guilty party in the process it is QLD, which has allowed its gas to be dumped on the Asian market at huge losses while charging discriminatory prices at home, skyrocketing power prices and shutting down swathes of Australian gas-fired power. As we know, it is gas that sets the price in the NEM owing to where it sits in the wholesale electricity market bid stack. See Australian Energy Market Operator description below:

Judith Sloan is, of course, a former gas sector executive with east coast cartieler Santos which was the prime mover in the great Aussie gas dumping. It lied about its reserves and has been vacuuming up third party sources ever since, also from The Australian:

As Santos worked toward approving its company-transforming Gladstone LNG project at the start of this decade, managing director David Knox made the sensible statement that he would approve one LNG train, capable of exporting the equivalent of half the east coast’s gas demand, rather than two because the venture did not yet have enough gas for the second.

“You’ve got to be absolutely confident when you sanction trains that you’ve got the full gas supply to meet your contractual obligations that you’ve signed out with the buyers,” Mr Knox told investors in August 2010 when asked why the plan was to sanction just one train first up.

“In order to do it (approve the second train) we need to have absolute confidence ourselves that we’ve got all the molecules in order to fill that second train.”

But in the months ahead, things changed. In January, 2011, the Peter Coates-chaired Santos board approved a $US16 billion plan to go ahead with two LNG trains from the beginning….as a result of the decision and a series of other factors, GLNG last quarter had to buy more than half the gas it exported from other parties.

…In hindsight, assumptions that gave Santos confidence it could find the gas to support two LNG trains, and which were gradually revealed to investors as the project progressed, look more like leaps of faith.

…When GLNG was approved as a two-train project, Mr Knox assuredly answered questions about gas reserves.

“We have plenty of gas,” he told investors. “We have the reserves we require, which is why we’ve not been participating in acquisitions in Queensland of late — we have the reserves, we’re very confident of that.”

But even then, and unbeknown to investors, Santos was planning more domestic gas purchases, from a domestic market where it had wrongly expected prices to stay low. This was revealed in August 2012, after the GLNG budget rose by $US2.5bn to $US18.5bn because, Santos said, of extra drilling and compression requirements.

“At the time of FID (final investment decision), there was a reasonable expectation during the early years that gas would be available in the market at the right price,” Mr Knox said. “However, large volume, long-term east coast gas supply and prices have tightened over the last 18 months, making third-party gas a relatively less attractive gas supply. This is what led to our announcement (that capital spending would increase).” For commercial reasons, Santos had not revealed the volumes of third-party gas needed to feed the second train.

Presentation slides reveal that by then, even with the $US2.5bn of extra spending, third-party purchases had grown from 140 terajoules a day, at FID, to 240 terajoules a day, or 20 per cent of east coast domestic demand.

Santos figured the gas it was taking out of east coast markets would be filled by accelerated production from the Cooper Basin (fuelled by the GLNG supply contract revenue), gas from the Narrabri coal-seam gas project in NSW and helped by the production of shale gas.

Unfortunately, shale drilling did not return hoped-for results, an oil price slump in late 2014 heavily restricted more Cooper Basin drilling and a community backlash, along with regulatory hurdles, stymied Narrabri.

Even before oil prices slumped, Santos revealed its call on domestic gas would be greater than flagged. In a June 2014 presentation slides to an analysts tour of the GLNG facility were told that third party gas would provide between 410 to 570 terajoules of gas per day, or the equivalent of up to half of total east coast domestic demand, even though it was planning to drill 200 to 300 domestic wells a year.

As a result, GLNG, had drilled 769 coal-seam gas wells as of November last year (and presumably connected fewer). This is about a quarter less than the 1000 it had planned to drill by the end of 2015.

If you want to fix the NEM then fix the gas price. STO is still profiteering as of yetserday, via UBS:

STO announces 15 PJ gas sale agreement with Pelican Point Power Station

The agreement will see gas from both GLNG and Santos sold to the 480 MW Pelican Point Power station owned by ENGIE in Adelaide, South Australia. Gas sales will commence in January 2018 and run for a couple of years. Pelican Point output has increased in recent months; at current generation levels it requires 20-24 PJ gas/annum.

Petronas and Kogas may make positive margin from the transaction

STO owns ~66% of gas production from the Cooper Basin, which we estimate will produce ~85PJ (gross) in 2018. With its forecast 56 PJ share of gas supplies, STO has a 50 PJ/annum contract with GLNG, known as the “Horizon” contract. We expect gas for Pelican Point to be derived from a combination of Horizon gas and STO residual equity gas. With oil prices remaining depressed and global LNG market oversupplied, we believe GLNG LNG buyers Petronas and Kogas may take advantage of low spot LNG prices to procure the cargoes they need and sell gas into the domestic market and generate a positive margin. As an example, at US$50/bbl oil price we estimate the LNG price ex-Gladstone to be US$7/mmbtu (equivalent to A$8.30/GJ). If GLNG has sold its gas to Engie at a similar price, there would be no economic impact to GLNG. If Petronas and Kogas then procure alternate LNG volumes for <US$7/mmbtu on the spot mkt (where prices are currently $5-5.50/mmbtu), they could effectively reduce their cost of supply.

Expect more GLNG deals to be done, but ADGSM uncertainty remains

GLNG is the only LNG project affected by the recently announced Australian Domestic Gas Security Mechanism (ADGSM). We expect GLNG to look to enter into more domestic gas sales where appropriate, though contract durations are expected to remain short. Does this remove any requirement for GLNG to supply gas into the domestic market if a shortfall is determined by the Resources Minister under the terms of the ADGSM? No. GLNG will remain a non-net contributor to the domestic market, so it will still have obligations under the terms of the ADGSM in our view. The Government has yet to make a decision on whether there will be a shortfall in 2018.

What is the point of the ADGSM if it doesn’t lower prices to at least export net back? That’s US$6 in SA.

If you don’t fix the gas price then don’t complain as states pull apart the NEM (and they will, price fixing is next). It is really that simple.