Via UBS:

Australia Still Looking Like A Laggard

As we have been discussing for some time, Australian earnings trends are less convincing than those playing out globally. Reporting season has been underwhelming but strength in the resources sector (due to a combination of good results and higher commodity prices) has helped the market.

Earnings-Powered Global Uptrend Should Drag Australia Higher By Year-End

The global equity rally is being supported by a moderate improvement in global economic momentum against a still-benign inflation and interest-rate backdrop. Our main short-term concern is the lack of a meaningful US/global correction over the past 12 months. However, the supportive economic and earnings backdrop alongside plausible valuations in the context of low interest rates suggests to us the medium-term trend is still likely up.

Current Sector Views

We remain overweight resources, moderately overweight banks, overweight selected US$ earners, underweight bond yield sensitives, underweight telcos and underweight insurance.

Stock Additions & Removals

We have made only minor changes this month: we have exited Suncorp Group after a disappointing result. We have also moved from Stockland Group to Westfield Corporation in REITs after further underperformance from Westfield sees it offer a reasonably attractive risk return trade–off in our view.

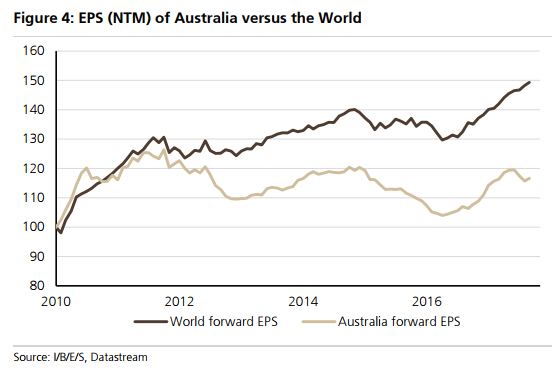

And the tragic charts, EPS lagging:

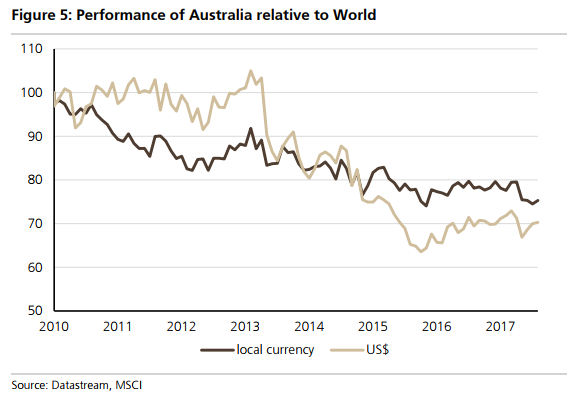

Returns lagging:

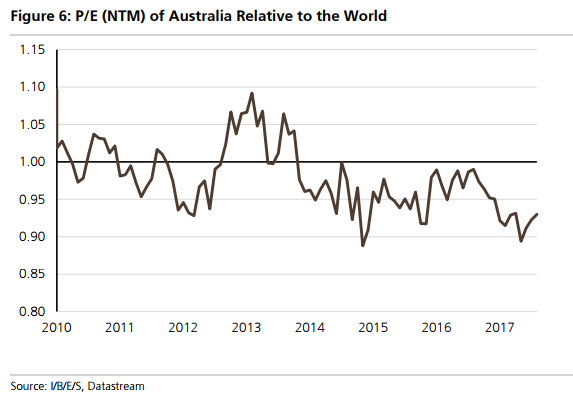

Multiples lagging:

And MB’s favoured allocation since early 2012 absolutely killing it:

Morgan Stanley see no change ahead:

Season Missed Expectations: With 96% of ASX 200 market cap reported, it is clear that the bias has been negative on actual results, with the ratio of misses to beats at ~1.3x, with the average EPS miss being penalized by -3.1% on results day. At the top line, 16% beat on revenue, while 22% missed. More importantly – of the 155 stocks within the ASX 200 universe thathave reported,59% have provided guidance, of which 43% have triggered FY18e EPS downgrades,versus 24% of stocks that received an upgrade. Importantly,growth conviction remains pressured and we expect consensus aggregate FY18e EPSg to fall to circa 5%.

Regional Underperformance Sustained: Putting Australian results in a global context, the ASX weighted miss of -0.7% compares with an 8.3% earning beat for the Topix, 6.3% for MSCI Europe and 5.4% across the US. MSCI EM and APxJ companies in aggregate have beaten consensus net income estimates by 2.6% and 2.4%, respectively (~75% of market cap reported). China and HK companies reported the strongestnet income beat in APxJ/EM, with Taiwan, Singapore and Australia missing. Australia’s lag in earnings strength is a key contributor to its bottom-quartile regional performance this CY (see Asia/GEMs Equity Strategy: EM earnings beat lead by China,25 Aug 2017).

Top-Down and Bottom-Up Signals Align: Weak income and tighter personal credit conditions are making the domestic revenue environment difficult. We expect deceleration from here – the all-important Christmas season looms,and factoring in energy cost increases alone, we see a ~1.4% squeeze on ex-food retail sales,equating to about 8% less ‘Christmas cheer’. This also supports our call for continued growth disappointment at the macro level, where we see annual GDP growth slowing to the low-1s,and confirms our thesis that Australia is out-ofsync with the global recovery (see Australia Macro+: On track for 1.1% GDP growth,28 Aug 2017).