Rod Myer has penned a piece in The New Daily today warning that the Turnbull Government’s First Home Savers scheme will likely lower retirement savings:

Stephen Anthony, chief economist with Industry Super Australia, said the First Home Super Saver Scheme, sold by the government as a housing affordability measure, would offer limited benefits to first home savers and threaten retirement savings.

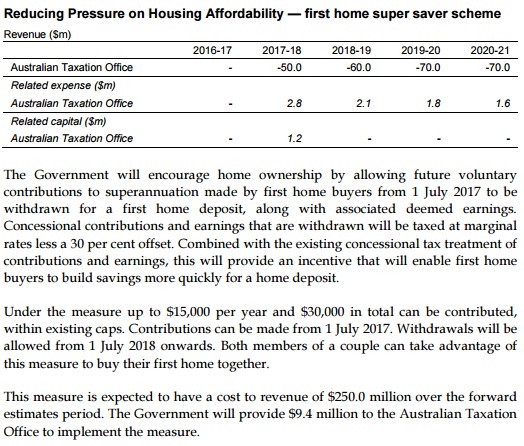

The plan, introduced in the May budget, allows first home buyers to salary sacrifice up to $30,000 into their super account at a maximum rate of $15,000 a year.

The savings are taxed at the super rate of 15 per cent on the way in, which is lower than the 19c bottom tax rate and so gives you a benefit. When funds are withdrawn they are taxed at the marginal rate of the saver less 30 per cent.

This is where the plan strikes trouble. The ATO doesn’t simply tax the money you take out when you buy a home, it will assume you made a return on it that is equivalent to the bank bill rate (what banks pay professional investors) plus three per cent.

That guaranteed return is added to the amount you withdraw, which is fine if your super fund is earning that amount or more. But in years when your super fund makes less than that benchmark, money is effectively being taken out of the rest of your super to make up the figure the taxman wants you to have.

“Super funds will be forced to dip into compulsory savings to cover shortfalls in ‘guaranteed’ returns, leaving people with much less at retirement,” Dr Anthony told The New Daily.

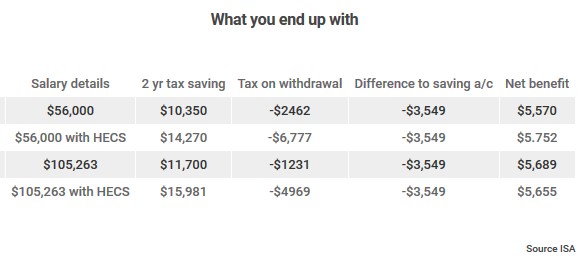

Those transfers from your super to fund your home deposit can be significant. For the year to June 2016, for example, using the ATO’s formula would have seen you transfer an average of 2.3 percentage points of your general super returns into your deposit savings account, ISA research says…

Let’s be honest. This scheme was always going to be a dud that would: 1) reduce retirement balances; and 2) place moderate upward pressure on house prices (making housing affordability worse).

Fortunately, the re-gigged First Home Savers Account is, like its predecessor, is also rather weak. It’s only expected to cost the Budget $250 million over the forward estimates (see below) – probably an overstatement given Labor’s scheme had such a poor take-up rate and just 2% to 3% of young people currently salary sacrifice additional funds into superannuation.

Advertisement

The truth is, MB expected the first home buyer bribe contained in the May Budget to be much worse, and we were actually relieved that it ended up being Mickey Mouse.

Leith van Onselen is Chief Economist at the MB Fund and MB Super. He is also a co-founder of MacroBusiness.

Leith has previously worked at the Australian Treasury, Victorian Treasury and Goldman Sachs.