Thanks to McGrathmaggeddon we know exactly what to look for in over-inflated and poorly timed exit strategy IPO. Fairfax today announced something a little similar.

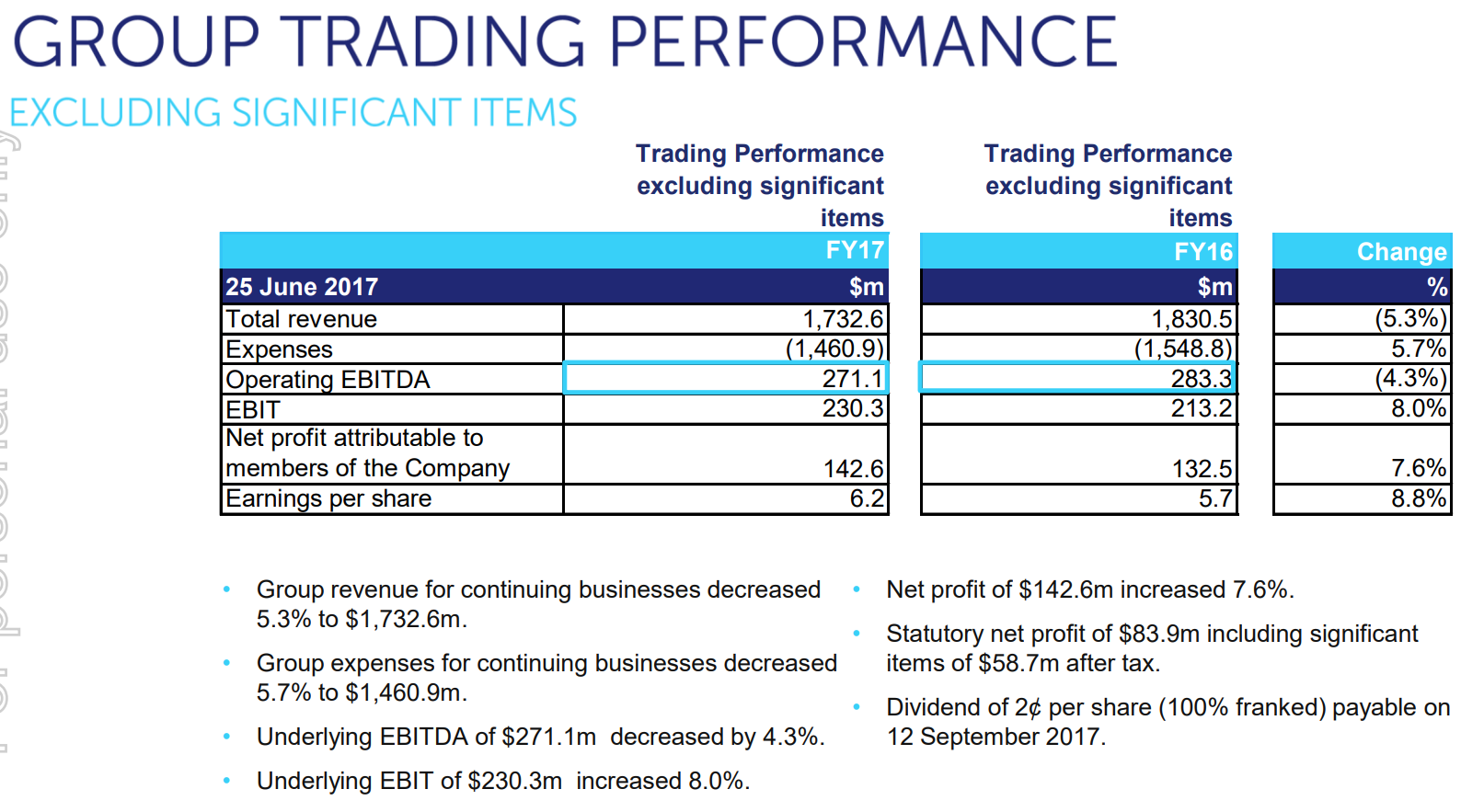

It’s full year result was ordinary with falling revenue but costs falling even faster to deliver a rebounding net profit after big losses last year:

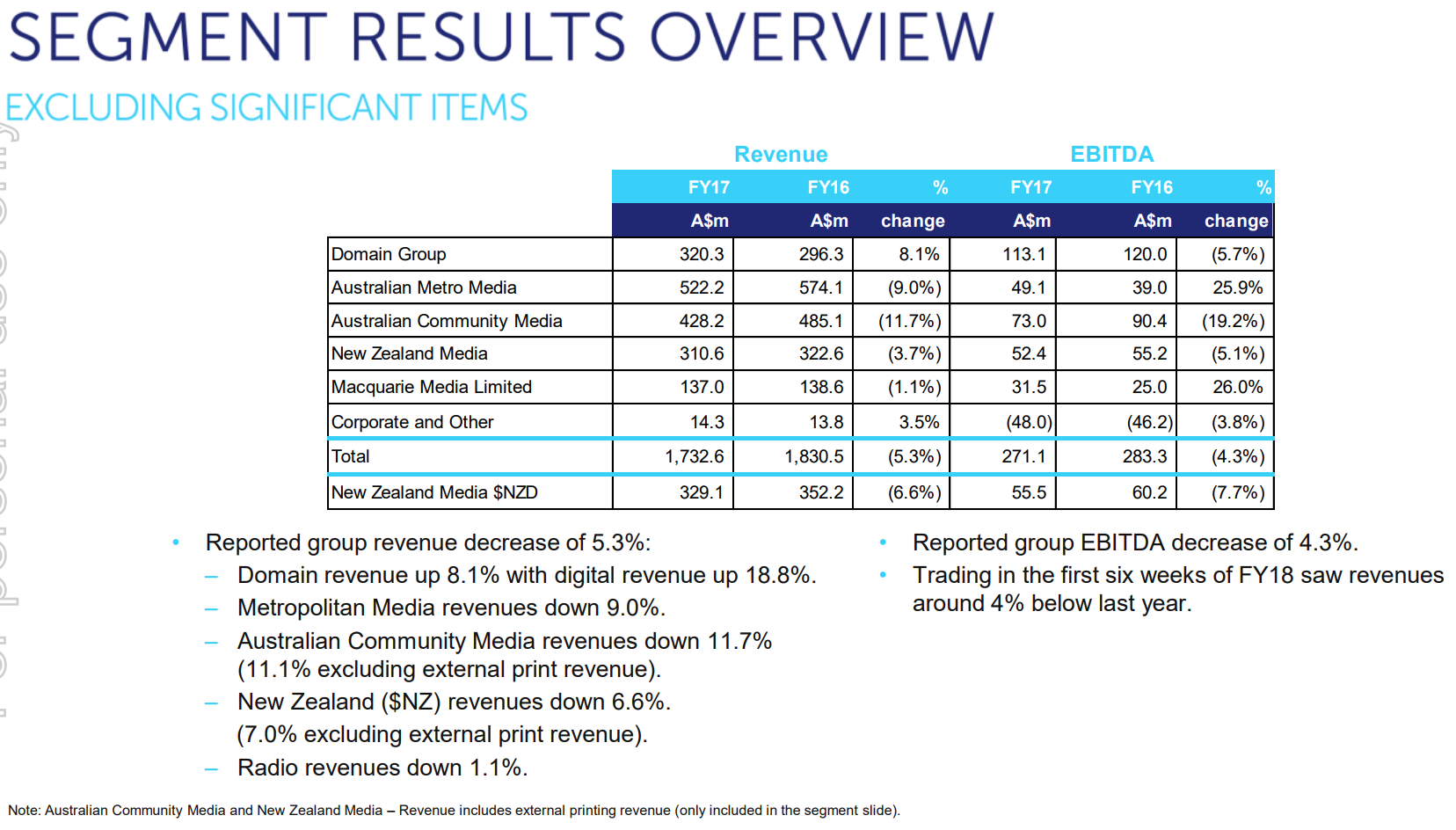

Needless to say, shrinking to greatness is hardly the stuff of a powerhouse business model but it gets worse when we delve into the business lines:

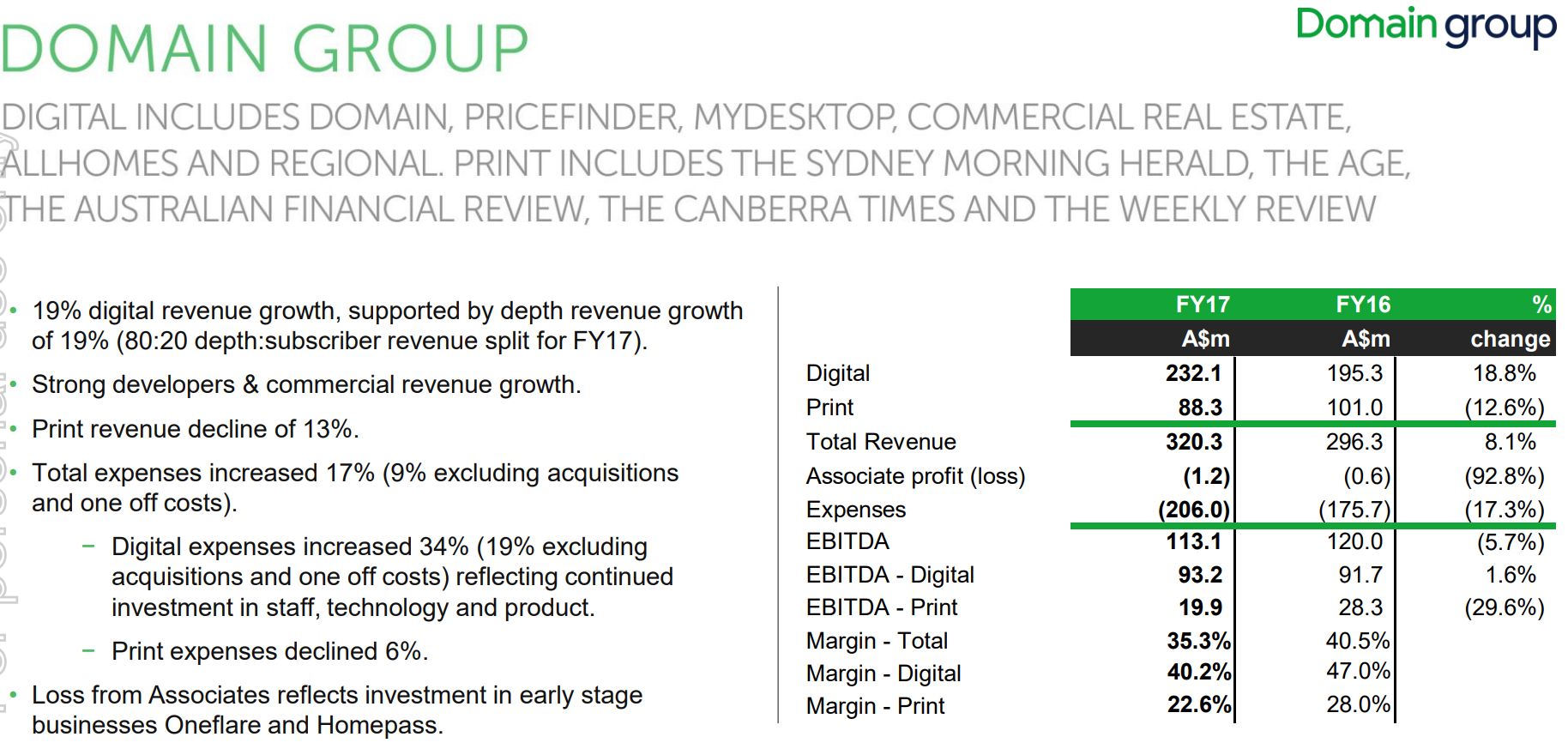

Everywhere you look, electronic delivery is cannibalising print revenues, even in Domain Group:

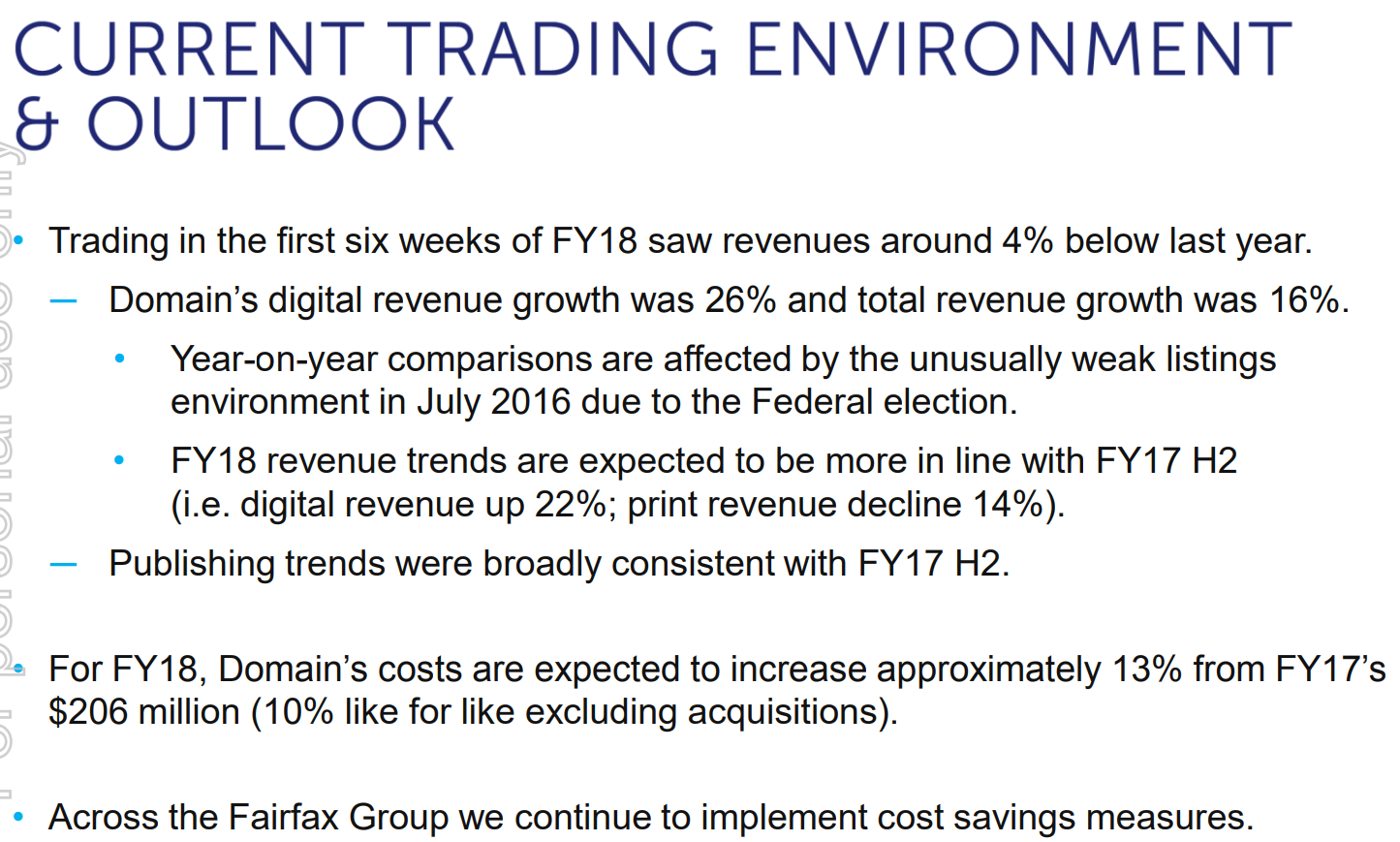

And there is no end in sight:

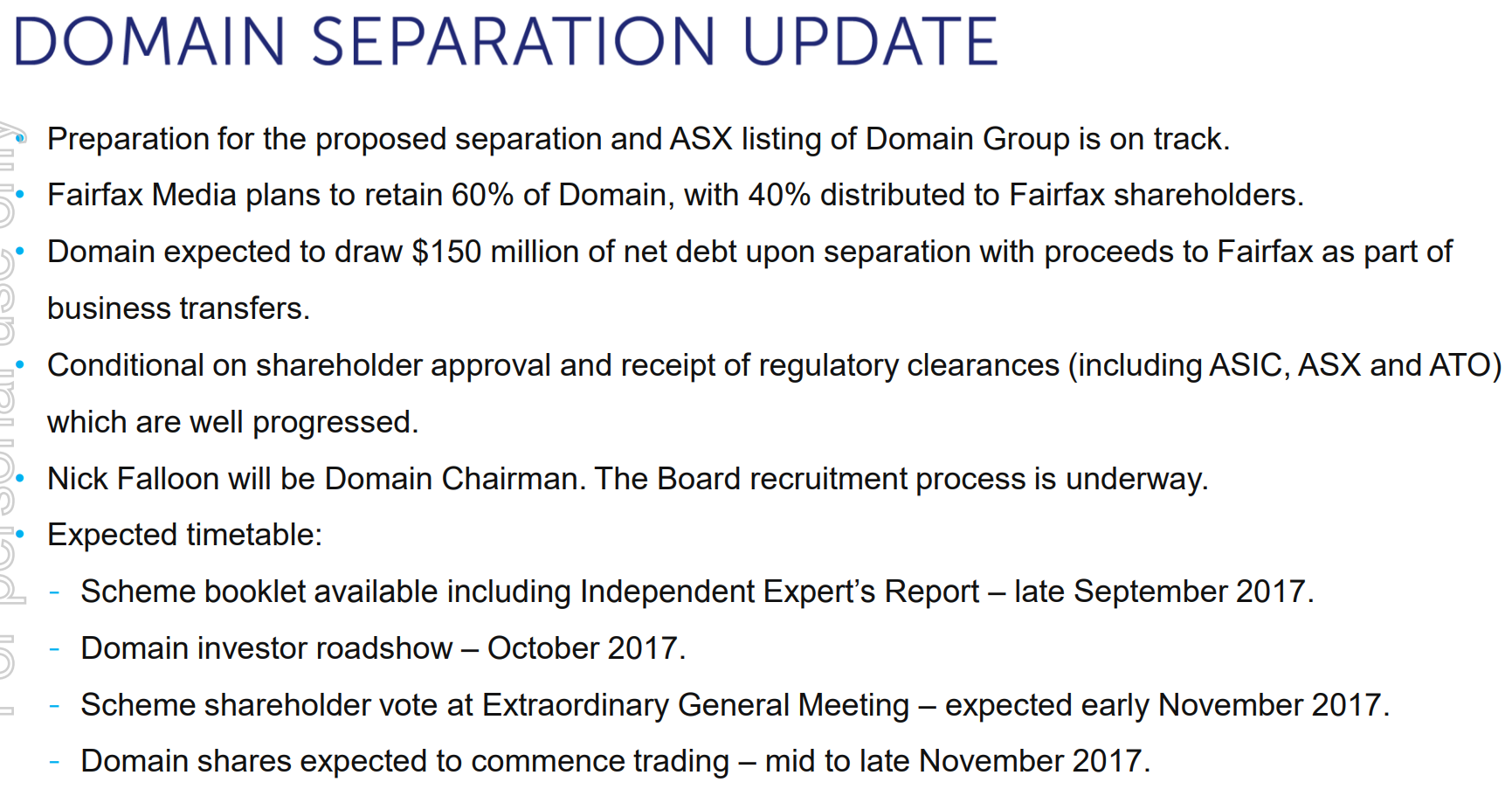

Which brings us to the Hail Mary move, Domainmaggeddon:

It makes sense for Domainfax to partially free the Domain balance sheet to fund growth. But is it worth investing in?

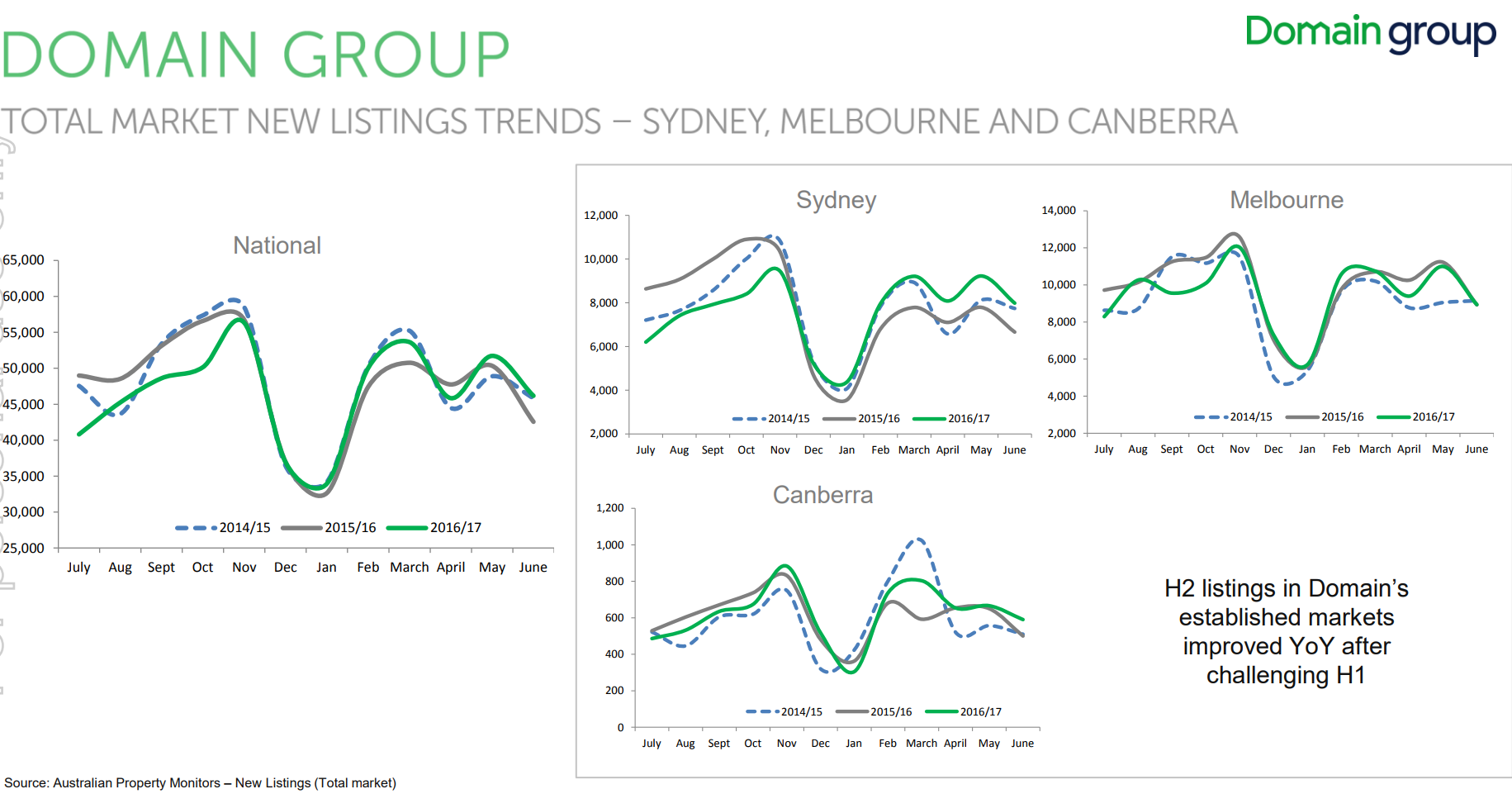

The business has some strengths, most obviously in its duopolistic position in the market providing pricing power. As the smaller member it may still have some market share growth in it as well. To that extent it is a better option than McGrathmaggeddon which exists in a highly fragmented sector. But like the ill-fated realty group, it is a listings-dependent business at the end of a very obviously mature boom cycle so one has to seriously question the timing. Listings have recently rebounded from 2016’s extraordinary “shrinkflation” episode but traditionally listings businesses do not do terribly well when real estate prices fall and that is precisely the developing environment for 2018:

Monetary regulators have made it abundantly clear that they are determined to cap household debt, which equates almost exclusively to mortgages, so the timing could not be less auspicious.

There is also some disruption risk, via Morgan Stanley:

2) Why we believe there is some risk for REA. We estimate Purplebricks et al currently only have <1% share of listings in Australia … so it’s not a big deal. But we note their peer group in the UK have ~6% and aspirations to reach 30%. To date there’s been no impact on REA earnings at all, because Purplebricks still advertises every listing ithas on REA (and Domain). But, the key point is, it’s always a basic listing. Premium is an option, but rarely taken. Thus the higher the penetration Purplebricks achieves overtime … the larger the potential disruption on REA’s propensity to: i)grow subscribing agents; ii) push annual price increases; and iii) sell more premium ads – the key driver of recent earnings growth.

I expect that as the long and drawn out reckoning of the Australian economic model transpires, Domain pricing power is also likely to come under pressure as its realty clients fail.

It may not be as bad as the McGrathmaggeddon IPO before it but it’s a matter of degree not kind.