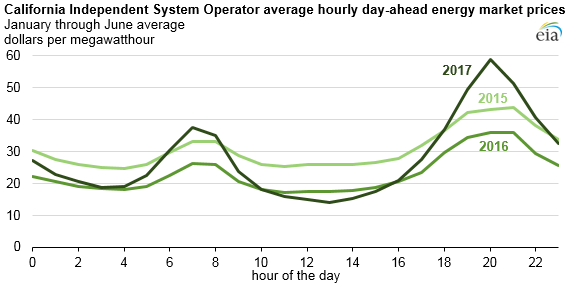

Last week we got an update from the US EIA on the growing differential between electricity prices throughout the day – the spread is now out to $45/mWh between prices at 1pm and prices at 8pm:

Source: EIA

Given this, it is worth a quick update of where prices stand in our journey to energy parity, particularly for batteries.

Keep in mind that the above chart is the “day-ahead” price. The actual energy price range is much larger and does provide much greater arbitrage opportunities for those that can store energy, this is more of an indicator of the on-going arbitrage opportunities.

Earlier this year we had a detailed look at the big picture numbers behind electricity prices and batteries in particular, concluding that (utility scale) batteries to shift the usage from 1pm to 8pm would be around $US220/mWh but that costs were falling at 20% per annum.

Tesla’s recent South Australian battery costs seem to be in that ballpark (I haven’t seen an official figure, maybe readers can point one out?), reports seem to suggest $US200-250.

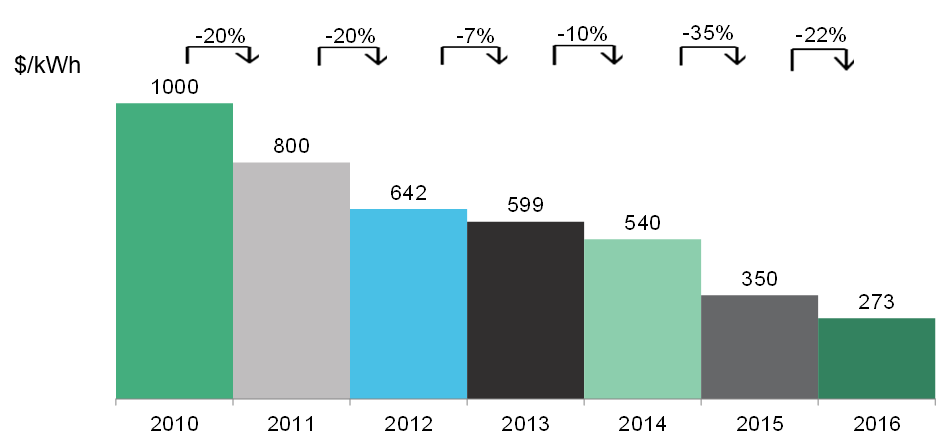

Since then, Bloomberg has updated its battery numbers for 2016, showing that batteries continue to fall at 20% per annum:

Source: Bloomberg New Energy Finance

Net result?

At around $200-250/mWh batteries are a good alternative to peaking plants but they are a long way off influencing the $45/mWh typical spread between electricity prices throughout the day and prices at night.

Updating our investment summary from earlier in the year:

Investment Summary

At the moment, it looks like 7-10 years until we hit “energy parity” (see report from earlier this year for details) between solar+batteries and fossil fuels if current cost reductions are maintained. And don’t sleep on rooftop solar + batteries – they are a lot more expensive than coal, but retail power prices are a lot more expensive than wholesale. There is a decent chance that rooftop solar + battery users going off-grid start a “death spiral” for electricity transmission.

Battery costs are the major determinant at this point – if the rate of improvement slows then it may take 15-20 years. The base case is that battery improvement will be sustained, but it’s far from a given – this is the assumption to watch.

Power prices during the day are going to continue to fall over the next few years as we end up with a surplus of power from renewables. This will actually drive the pick up in batteries – the bigger the difference between the day price and the evening price the bigger the incentive for batteries.

The US is not the market to watch – energy costs are lower there than almost any other developed market. A better indicator of the future will be developments in Europe.

So, how does this affect investments:

- Coal/Gas: Coal and gas will not cease to be used when we hit parity, it is just that the price will be limited to no more than solar+batteries, and that cost will fall year after year. Any investment in these companies should be done with falling commodity price expectations – i.e. value them in run-off. There may be short-term shortages/price spikes, but these are selling opportunities. Increases in electric car penetration may stall the downward trend for a few years.

- Solar companies: Solar manufacturers are difficult – the technology is moving too fast to work out if there will be a “winner takes all”. Service providers to the solar industry are probably a better investment (if you can find one that’s not already very expensive) – we have added one of these recently to the portfolio. We have also been kicking the tyres of some of the semi-conductor stocks that manufacture “commodity-type” parts for solar companies – not a sexy area of the market (and thin margins) but at the right price some of these stocks are interesting.

- Industrials: Companies that have high electricity bills during the daytime (or can shift costs to the daytime) will benefit. There are a number of European materials and refining companies that have struggled to compete with US companies because of the lower-cost US energy.

- Oil: At the margin, less diesel will be used for power generation in remote areas. Expect this to continue. It is not a large part of the oil market, but it will mean oil demand will be weaker than they would have otherwise been.

- Electricity Transmission: Will they get bailed out, will they be allowed to increase prices to offset falling customers, or will they take the pain of the “death spiral”? It is a country by country proposition – lots of risk in this trade.

- Electricity Production: The toughest thing about an investment today for these companies is that your competitor who builds a solar array next year will have lower costs than you who built last year and so your competitor can handle lower electricity prices. Plus the regulatory risks from the “death spiral”. Another risky trade.

None of this relies on increased carbon taxes. But increased carbon taxes will accelerate the trends.

Damien Klassen is Chief Investment Officer at the Macrobusiness Fund, which is powered by Nucleus Wealth.

The information on this blog contains general information and does not take into account your personal objectives, financial situation or needs. Damien Klassen is an authorised representative of Nucleus Wealth Management, a Corporate Authorised Representative of Integrity Private Wealth Pty Ltd, AFSL 436298.