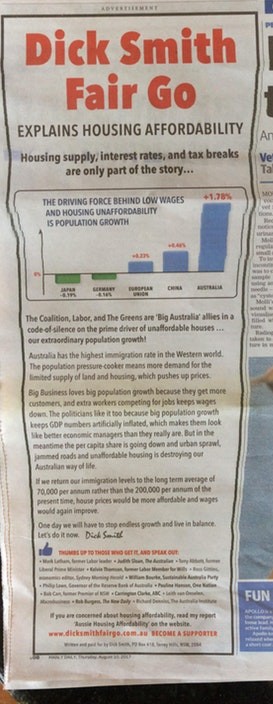

Aussie entrepreneur and icon, Dick Smith, yesterday launched his new website, Dick Smith Fair Go, with a series of advertisements in Australia’s major newspapers (example below):

Below are a few key extracts summarising the key causes of Australia’s housing crisis:

Advertisement

Supply and demand:

The government, the banks, and many economists peddle the disingenuous misdirection that it’s just a lack of supply that’s to blame. It usually sounds something like this:

“Overwhelmingly, the single greatest contributor to the housing affordability issue is land supply, is a lack of land in the right places, is zoning restrictions that make it difficult to develop, is red tape that makes it difficult for housing estates. And also, importantly, having infrastructure, like transport, in the right places. … Those things together probably make the greatest contribution.” Mitch Fifield – Q&A

When the role of demand does occasionally get an airing, like the time I stirred the pot by pointing out that Pauline Hanson’s One Nation was the only political party to have a policy on Australia’s population growth, many of the Twitterati breathlessly babble that “Immigrants can’t all be on welfare and competing with Australian first-home buyers at the same time!”.

It’s true that immigrants are often unfairly scapegoated for many of society’s problems, and that should always be called out for what it is…

Just like anything else, land and house prices depend on both supply and demand – and Australia’s housing supply clearly has difficulty keeping up with our break-neck population growth.

This is not surprising considering housing supply adjusts slowly to increased demand (with the many steps and constraints involved in building new housing stock) while we have the equivalent of five wide-bodied jet-loads of immigrants coming in every week.

But many economists, and politicians like Mitch Fifield, talk as if the ‘supply’ of land for housing was the only thing that we could change, whereas the demand caused by immigration-fuelled rapid population growth was beyond our control.

If anything, the reverse is closer to the truth. After all, in suburbs close to jobs and opportunities, the availability of land in which to build new stock is very limited. Increased demand from more and more people trapped inside a limited ring of desirable inner suburbs sends prices sky high…

There are those who look at our vast land area and imagine it could be filled with people. But Australia’s geography should be seen in terms of a thin coastal strip, that requires careful management and planning, bordering a vast arid interior of salty, sandy soils – a relatively low carrying capacity.

So if we want to avoid that future, and generations of battery-kids, then we need to look at our immigration-fuelled population explosion…

Capital gains tax and negative gearing

After population growth, the next big driver of unaffordable housing comes from the workings of the capital gains tax (CGT) combined with negative gearing…

The way that the CGT 50% discount and negative gearing interact causes the most problems for housing affordability…

Turbo-charged bank lending:

After the stock market collapse in 1987, when business took a hit and slowed down, Australian banks shifted their focus to lending for property investments.

This was turbo-charged after the Global Financial Crisis of 2007–2008 when interest rates were driven to historic lows in an attempt to spur ‘economic growth’ by making it very cheap for people to borrow money for investment.

The more money the banks pumped in, the higher real estate prices rose to meet the increased spending power of buyers. The higher the prices, the higher the loans. This is a business model that some would call a ‘Ponzi scheme’ – which are illegal in Australia. Aided and abetted by negative gearing and the 50% discount on the capital gains tax, it was very profitable for everyone who could get in on the action…

Overseas investment and speculation:

Another factor that is having a major effect on the price of housing is the influx of capital from overseas investors…

Government has passed token legislation in an attempt to restrain its effect, but there are always ways of circumnavigating these laws… survey data consistently shows that foreign buyers account for a significant share of established home sales…

It is also possible that many of the purchases are funded by ‘black money’; that is, corrupt money from countries whose governments are attempting to crack down on corruption.

Indeed, the global anti-money laundering regulator (the Paris-based Financial Action Taskforce) found that Australian homes are a haven for laundered funds, particularly from China.

It’s almost as if Australia would prefer to cooperate as a launderer of corruption than deal with the negative effects on young first-home buyers.

And below are some of the policy solutions offered in the report:

Stabilise the Population:

One way to make a big difference to the housing affordability crisis is to admit that both supply and demand factors are at play.

With more than half of Australia’s break-neck population growth coming from immigration, our government needs to look at what it can do about overheated demand.

The prudent path forward is to plan for the population to peak and stabilise at the highest level that our continent can sustain at the standard of living that we’ve achieved in Australia today.

How do we do this?

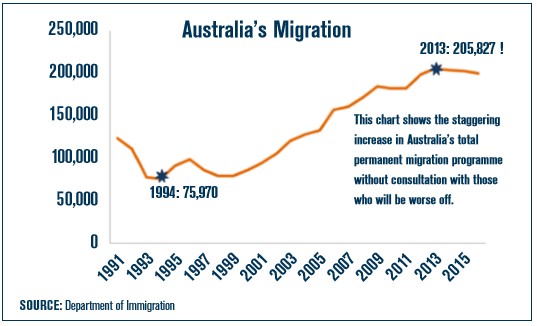

With our current net immigration numbers (arrivals minus departures) of around 200,000 each year, the Productivity Commission estimates that Australia’s population will increase from around 24.5 million currently to around 40 million by 2060.

By comparison, under zero net immigration (where we admit the same number of immigrants into Australia as we have people leaving the country) of about 70,000 new immigrants each year, Australia’s population would peak at 27 million by 2060.

So our current 200,000 net immigration intake would add some 13 million people over these years, while our natural increase would add just 2.5 million.

A lower population growth rate and a stabilised population under zero net overseas migration would reduce the demand for housing and give supply a chance to catch up.

It would also reduce the pressure on our national infrastructure and help Australia’s economy stay within the ecological limits to growth on the arid continent we call home.

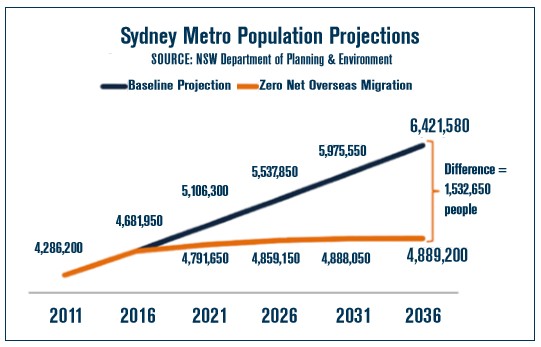

To illustrate, consider Sydney in the chart below, where State Government projections have the city’s population growing by 1.53 million fewer people over the next 20 years with zero net overseas migration.

That’s the equivalent of nearly four Canberras that would not need to be built across Sydney, along with all the extra people competing for housing and choking-up Sydney’s roads and public transport.

Capital Gains Tax:

First, removing or reducing the 50% discount on capital gains made from investing in housing would help to reduce the incentive for investors to pile money into property and encourage them to channel their money into more productive, job-creating ventures.

If we bring housing prices down by reducing immigration and increasing supply, investors wouldn’t be seeing much in the way of capital gains anyway, which will also reduce their incentive to invest in housing.

Negative Gearing:

Second, negative gearing rules should be reformed so that investment interest expenses on property can only be deducted against taxable income from other investments earned in that year.24 This reform would reduce house prices by making residential property less attractive to the investors, and further encourage them to channel their money into other, more productive assets, like job-creating businesses.

A Broad-based Land Tax:

It would also make sense to apply a broad-based land tax (preferably in place of stamp duties) in Australia.

Such a reform would encourage a more efficient use of the housing stock and improve labour mobility, penalise land banking and vagrancy (increasing effective land supply in the process), and help to make infrastructure investments self-funding for governments, since any land value uplift brought about through increased infrastructure investment would be partly captured by the government via increased land tax receipts…

Increased taxation on overseas investors:

Let’s increase the tax on foreigners who want to buy Australian property.

In Victoria, the foreign tax is currently 7% of the value of the purchase. In New South Wales it’s 4%, and in Queensland its 3%. The remaining states and territories currently have no foreign tax at all.

The last thing that we want is more young Australians being outbid at auctions for inner-city apartments by overseas investors looking for somewhere safe to park their wealth away from their own government – especially if they’re going to leave them empty.

Using a tax to hit the profitability of foreigners investing in the Australian property market would make some of them look elsewhere and give Australians looking to buy their first home a chance to take their place.

Implement anti money laundering rules on residential property

In 2008, the Australian Government was supposed to implement anti-money laundering (AML) rules for real estate gatekeepers, such as real estate agents, accountants and lawyers. This legislation has been sitting in limbo for nearly a decade, despite explicit warnings from the global AML regulator (the Parisbased Financial Action Taskforce), AUSTRAC, and Transparency International that Australian property is a potential haven for laundered funds.

Bringing Australia’s real estate gatekeepers into the AML net would meet Australia’s global commitments as well as dampen foreign demand for Australian property.

Leith van Onselen is Chief Economist at the MB Fund and MB Super. He is also a co-founder of MacroBusiness.

Leith has previously worked at the Australian Treasury, Victorian Treasury and Goldman Sachs.