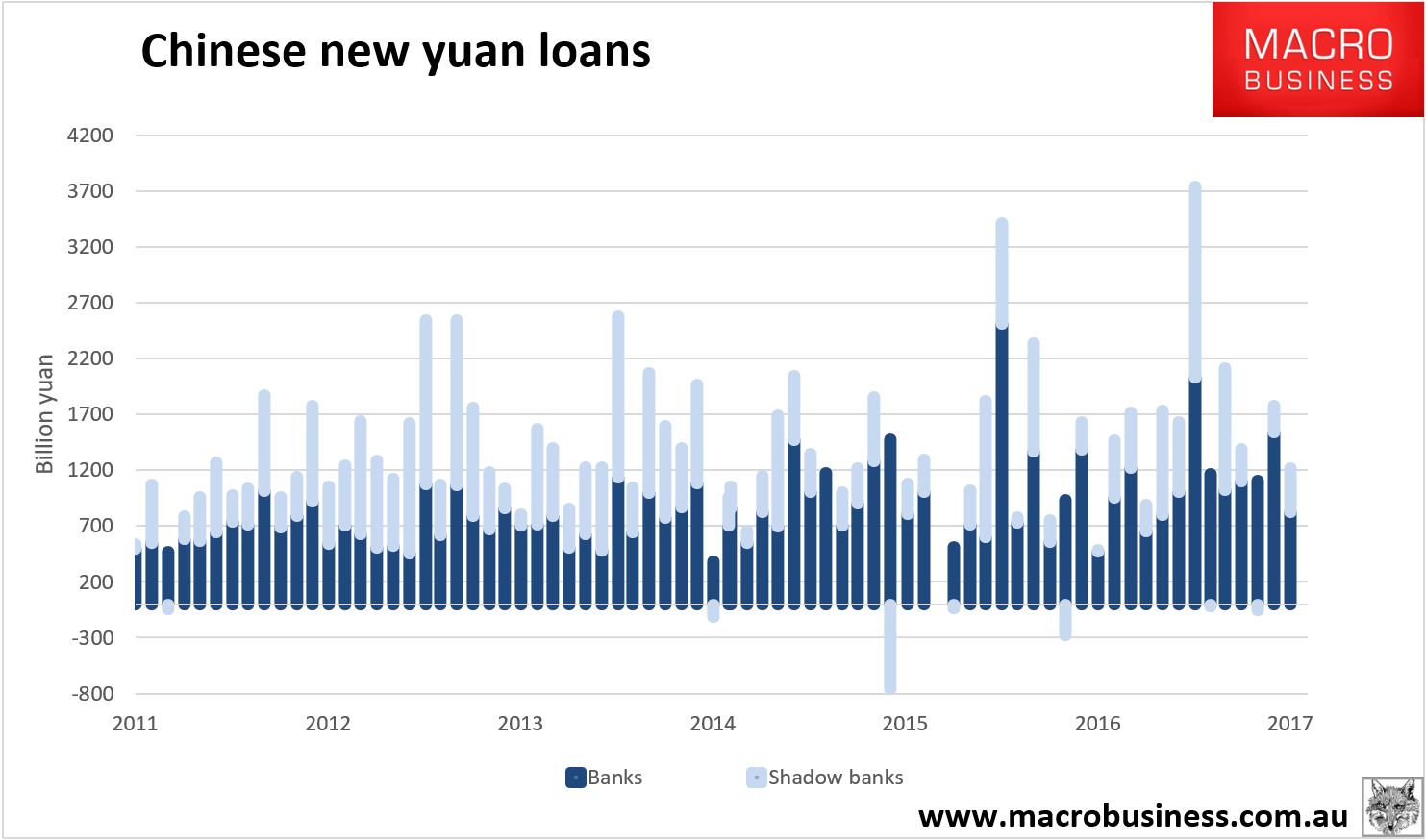

China’s July credit numbers were out and show ongoing strength with Total Social Financing at $1.22tr yuan and bank lending only 826bn of that:

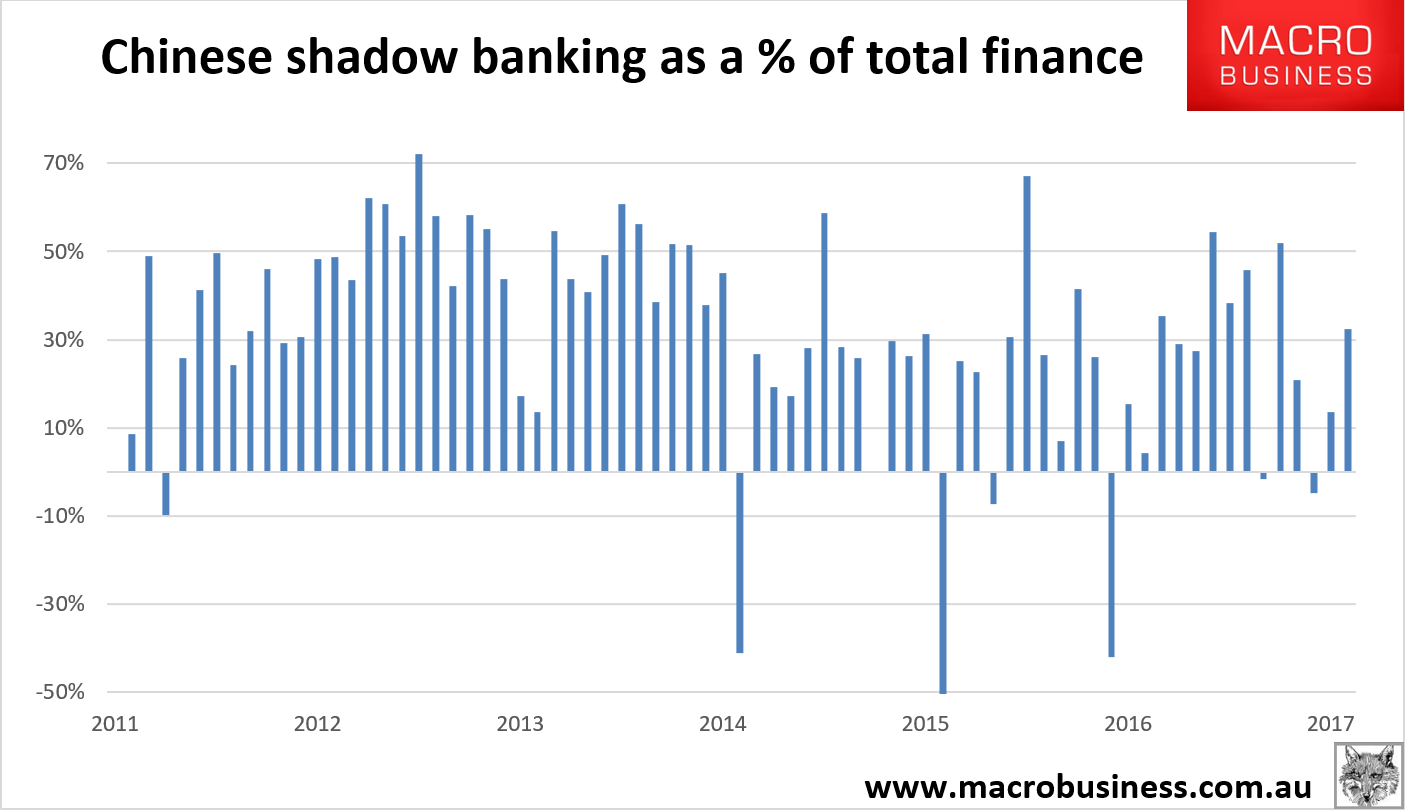

Shadow banking rebounded after a few months of downtrend:

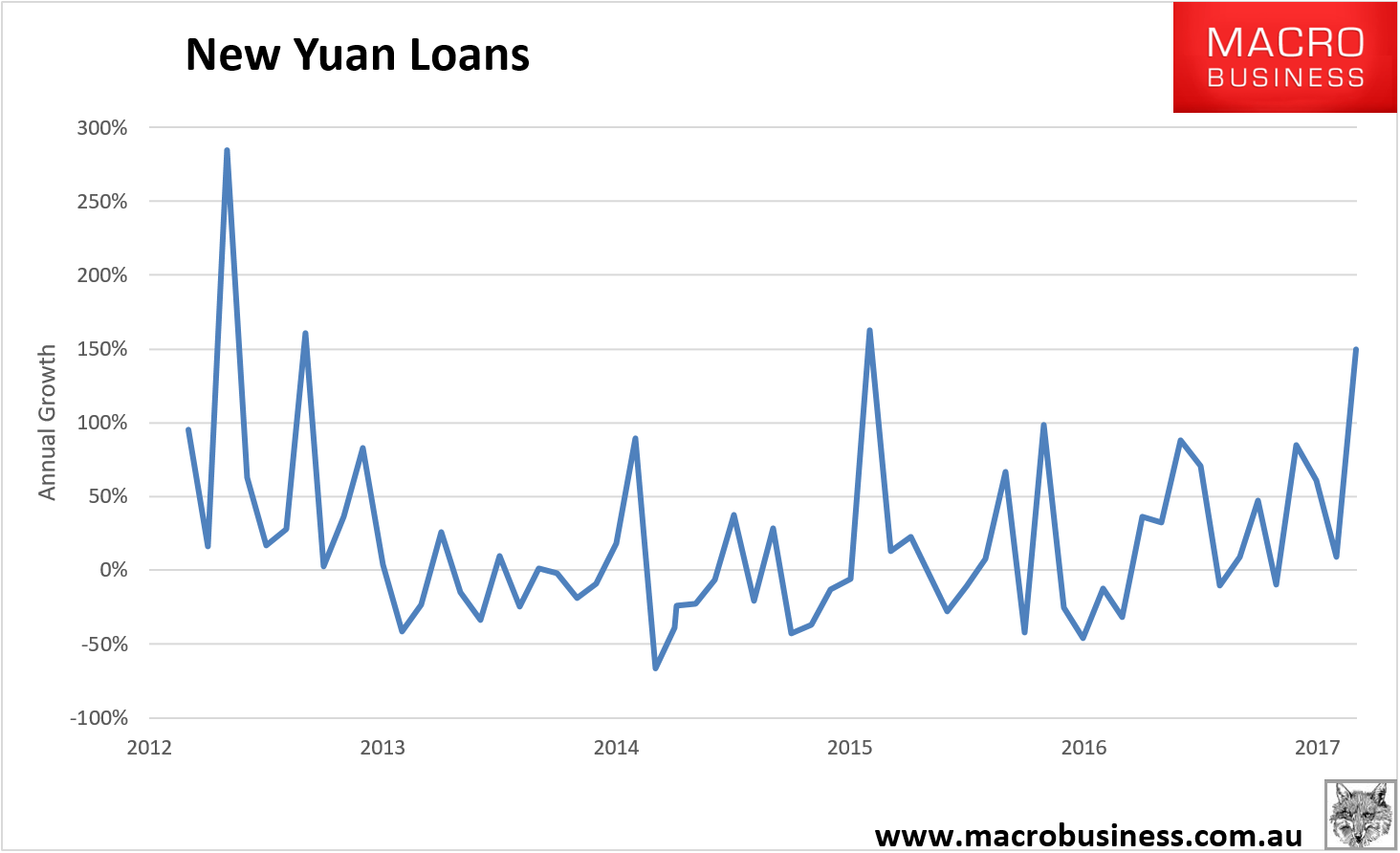

Year on year financing jumped after a weak July 2016:

Advertisement