Output growth in Australia has been soft over the past year. The latest national accounts put real GDP growth at just 1.7% over the year to QI 2017. But over that same period, total income growth has been incredibly strong. Nominal GDP, the broadest measure of national income, lifted sharply over the past year after an extended period of weakness (chart 1). For most households, however, it doesn’t feel like national income growth has been strong. Wages growth remains soft and household disposable income per capita has fallen through the year (see here). It’s quite an unusual situation for nominal GDP growth to have been so robust at the same time as wages growth remaining dormant.

In this note we take an in-depth look at nominal GDP. We begin with a discussion on the importance of nominal GDP and why growth has been so strong over the past year. We then look at why the lift in national income hasn’t flowed through to the household sector and we outline the reasons why nominal GDP growth is set to ease from here. Finally, we discuss the rationale for our monetary policy call in the context of nominal GDP.

Why nominal GDP matters

Most commentary around GDP focuses on real GDP – the change in the total quantity of output in the economy. This makes sense because it paints the actual picture of economic growth.

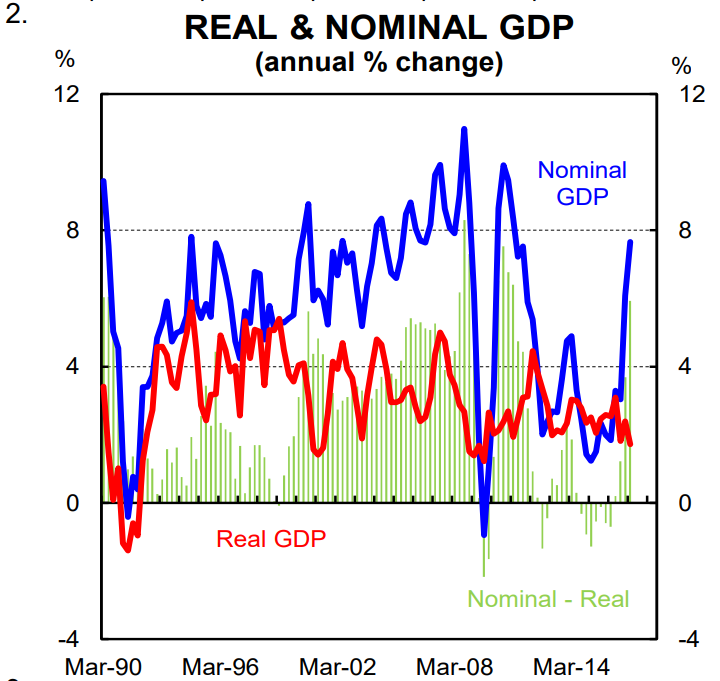

But nominal GDP is also very important. As distinct from real GDP, nominal GDP is the monetary value of the goods and services produced in a specific time period. In other words, it takes account of the price changes of the goods and services produced as well as the quantity. In Australia, commodity prices play a big role in nominal GDP moves. As a result, nominal GDP growth is more volatile than real GDP (chart 2).

Nominal GDP is important for earnings and revenue. Wages, profits and taxes are all measured in nominal terms. And importantly, debt is denominated in nominal dollars. As a result, nominal income growth is necessary to reduce the debt burden faced by households, businesses and government.

Having weak nominal GDP growth can have bad consequences for an economy. Wages, for example, are sticky downwards with a zero lower bound (workers are generally not asked to take pay cuts). As a result, if nominal GDP growth is persistently weak firms may seek to cut costs through a reduction in headcount or hours worked. Weak nominal GDP growth also discourages investment because it makes it harder for firms to repay debt. In that context, softness in nominal GDP growth dampens animal spirits – something the RBA has lamented and one reason given for the weakness in non-mining investment.

For the Government, nominal GDP is effectively the tax base. Tax revenues are strongly correlated with nominal GDP growth (chart 3). And the national debt burden is often expressed as a ratio to nominal GDP because it reflects the capacity of the Government to meet its debt obligation.

The recent story

Nominal GDP growth in Australia is heavily influenced by commodity prices and therefore the terms-of-trade (chart 4). Commodities make up around 65% of Australia’s exports with bulk commodities worth around 50%. The prices of commodities can be highly volatile. As a result, Australia can experience big swings in the spread between real and nominal GDP when there are sizeable movements in commodity prices, particularly the prices of iron ore and coal.

In the first phase on the mining boom, the commodity price boom, nominal GDP growth was particularly strong. But between early 2012 and late 2015, nominal GDP growth eased because falling bulk commodity prices dragged Australia’s terms-of-trade lower. In the year to QI 2017, however, a big lift in iron ore and coal prices pushed up national income significantly. The latest national accounts put nominal GDP growth at a strong 7.7%pa in QI 2017. This is the highest rate of growth in national income since the GFC. It’s also faster than total private sector credit growth which means that total private sector debt has fallen as a share of GDP over the past year, including household debt to GDP.

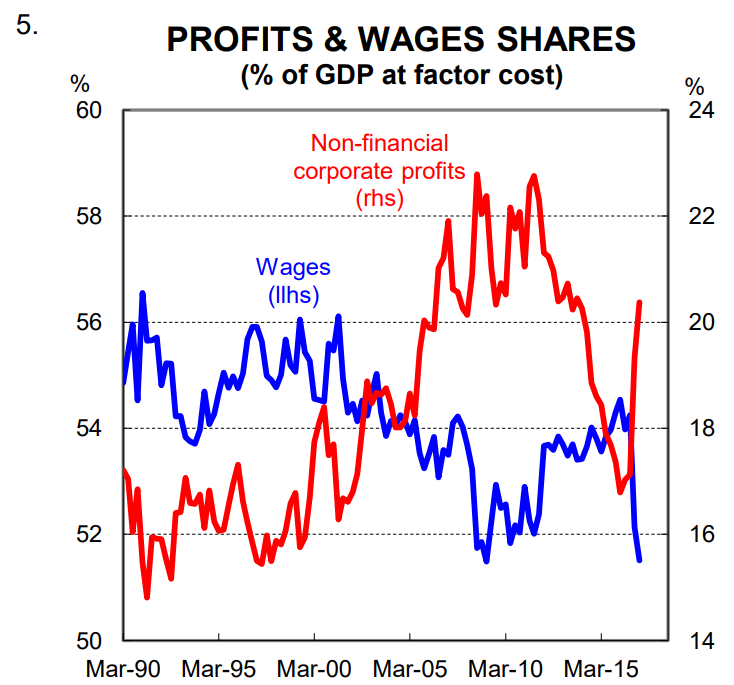

However, the lift in nominal GDP has not been distributed evenly between the household and corporate sectors of the economy (chart 5). Over the past year, employee salaries and wages growth has been incredibly weak. In contrast, the big rise in national income has been captured through a lift in company profits and taxes. As a result, while household debt to GDP has fallen, household debt to household disposable income has continued to rise (chart 6). So there is both a numerator and denominator effect at work. This is the key concern to the RBA and regulators. Weak employee salaries and wages growth is why the economy hasn’t “felt” like nominal GDP growth has been so strong.

While the household sector hasn’t done too well over the past year, the Government’s fiscal position has benefited as a result of the strong growth in nominal GDP. The latest Australian Government monthly financial statements puts 2016/17 revenue $6.3bn ahead of the Revised Budget profile. Some of this can be attributed to firmer commodity prices which have boosted corporate tax receipts and royalties. But in our view, this windfall won’t last because we see commodity prices trending lower over the next few years. On that note, we have been surprised by the recent strength in commodity prices. Chinese stimulus has been stronger than expected and the improvement more generally in the global economy has supported commodity prices. However, we still believe that bulk commodity prices will ultimately move lower as the Chinese economy rebalances away from investment to consumption led growth.

Why didn’t the lift flow through to the household sector

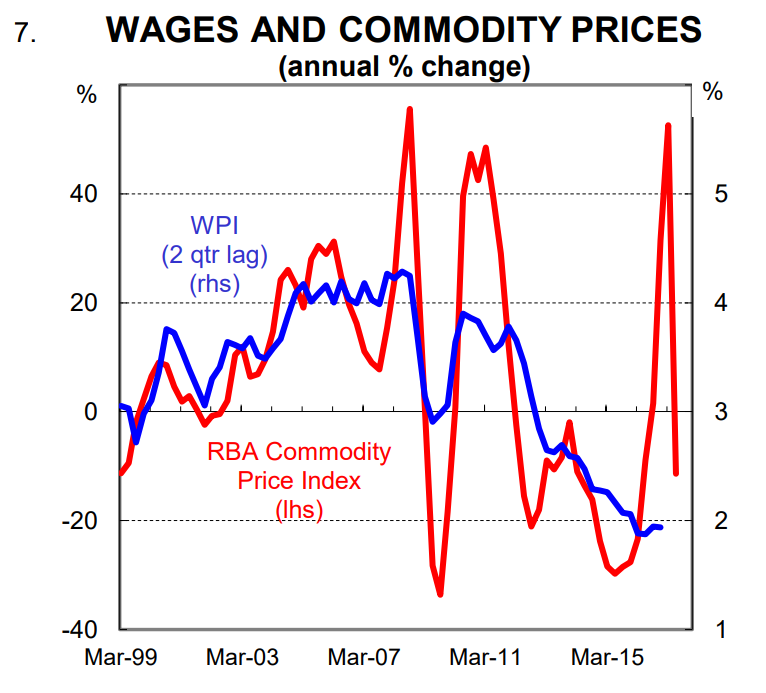

The primary and most direct mechanism for higher national income growth to flow through to the household sector is via wages growth. Historically, changes in commodity prices (i.e. the terms-of-trade) have been positively correlated with wages growth in Australia (chart 7). But there has been no lift in wages growth despite the lift in nominal GDP growth. There are a few reasons for this, but in our view the single biggest factor that has pushed down on wages growth is elevated labour market slack. There is very little incentive for firms to pay higher wages when labour market supply exceeds demand. In addition, the recent increase in commodity prices has not and will not generate a lift in investment like in previous cycles. Therefore it won’t materially contribute to labour market tightening like the prior commodity price booms. That said, mining vacancies have recently picked up so there will be a small direct positive impact on the labour market.

Of course some of the increase in nominal GDP growth from higher commodity prices has flowed through to the household sector via the share market. In particular, households that own shares in resources companies (including via superannuation) have benefited. Notwithstanding, household income growth, which includes dividend payments, has been weak. This disparity between corporate and household income growth is one of the reasons why a solid gap has opened up between business and consumer sentiment.

We should add that there is also another mechanism for a lift in nominal GDP to flow through to households and that is via a cut to personal income taxes or transfers. But at this stage, that looks unlikely. Indeed, the 2017/18 Budget assumes no change in income tax rates over the forward estimates period which means the average rate of income tax per worker will lift due to bracket creep.

The outlook

Commodity prices and therefore the terms-of-trade fell over Q2 2017. Our model puts the terms of down by 4.5% over the June quarter. This will weigh on nominal income growth and the impact will be evident when the national accounts print on 6 September. On our forecasts, nominal GDP will fall by 0.6% in Q2 which will see annual growth step down to 5.5%. At this stage, our “terms-of-trade tracker” is pointing to a rise of 5.0% in Q3.

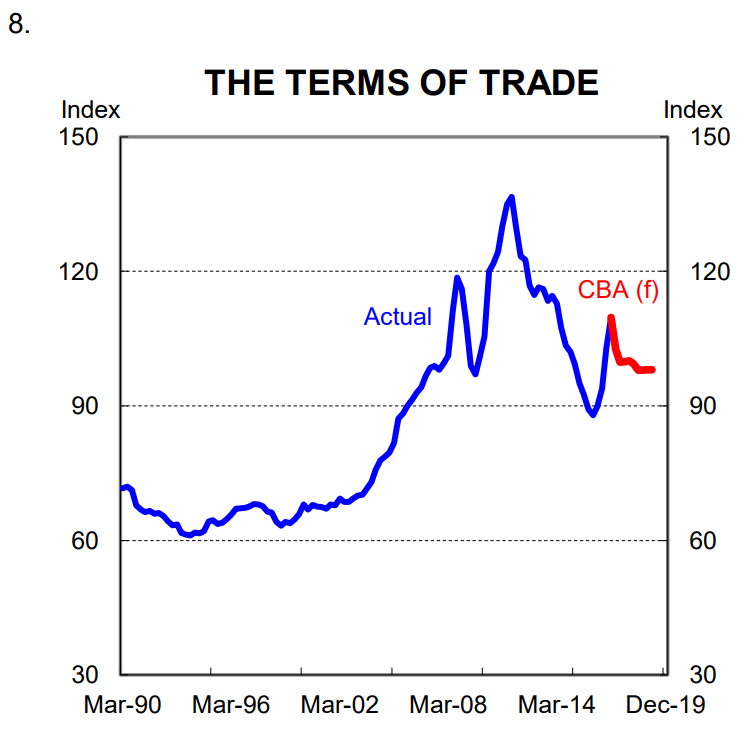

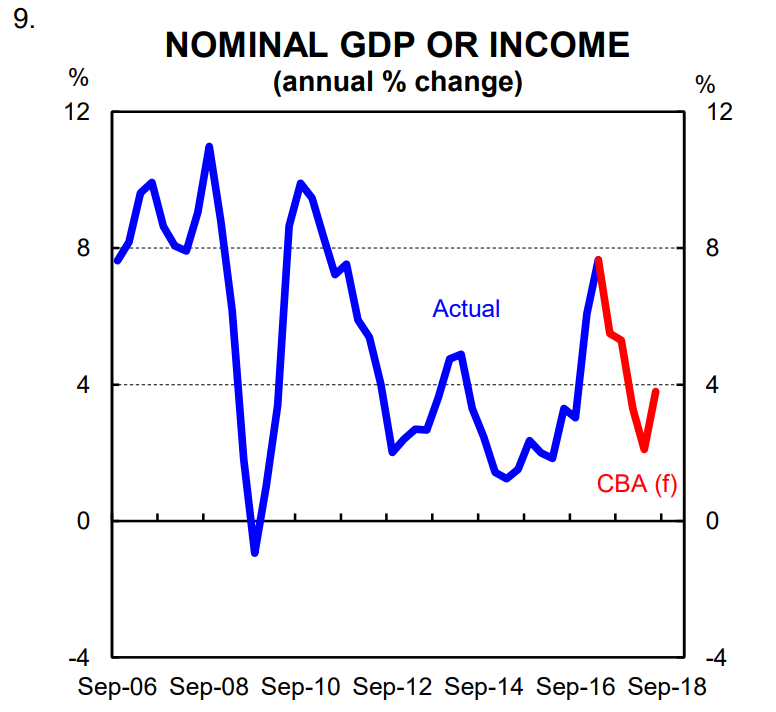

Looking further ahead, our views on real GDP, inflation within the broader economy, the terms-of-trade and the exchange rate influence our nominal GDP forecast. We expect the terms-of-trade to trend lower over the next few years, but to remain above its trough in early 2016 (chart 8). As a result, our forecast profile has annual nominal GDP growth easing to a low of 2.1% in QI 2018 despite a lift in real GDP growth (chart 9). This means that the Federal Budget will remain under pressure because growth in tax receipts will slow. Beyond that, we have nominal GDP growth lifting and stabilising at around 4½%.

What does it mean for monetary policy

From a monetary policy perspective, a softening in nominal GDP growth fits in with our view that the cash rate will remain on hold until deep into 2018. The RBA obviously has an inflation target. But there is a strong correlation between the cash rate and nominal GDP growth (chart 10). This makes sense because nominal GDP is picking up both changes in output as well as changes in prices (i.e. inflation). As chart 10 highlights, the recent lift in nominal GDP has not been accompanied with policy tightening. This is because: (i) there has been no spillover to wages growth and core inflation; and (ii) it is assumed to be a temporary lift.

Despite a solid lift in national income over the past year there is still plenty of spare capacity in the economy which will continue to weigh on wages growth and core inflation. The labour market is tightening, but from our vantage point underlying wages growth (i.e. excluding the impact of the Fair Work Commission on the minimum wage) will remain soft for some time. In addition, the higher AUD is acting as a disinflationary force and will weigh on nominal GDP growth over the period ahead. As such, we think that policy is on hold until core inflation is on a sustained uptrend which we suspect won’t be until late 2018. By then, we anticipate that nominal GDP growth will have stabilised at around 4½%pa.

Completely agree. I just don’t see the terms of trade continuing along that stable path so nominal growth won’t rebound…

David Llewellyn-Smith is Chief Strategist at the MB Fund and MB Super. David is the founding publisher and editor of MacroBusiness and was the founding publisher and global economy editor of The Diplomat, the Asia Pacific’s leading geo-politics and economics portal.

He is also a former gold trader and economic commentator at The Sydney Morning Herald, The Age, the ABC and Business Spectator. He is the co-author of The Great Crash of 2008 with Ross Garnaut and was the editor of the second Garnaut Climate Change Review.