The first column after the city name is its tier, then rental yield and payback in years. Xiamen tops out at a 1 percent yield, or 100 year return of capital. You might think that’s overstating things a bit, but it’s also a gross yield and doesn’t include maintenance, taxes and other costs. Most of the yields are also far below mortgage interest rates, as much as 50 percent below. Unless investors are paying cash, many properties won’t have a positive cash flow (ignoring inflation and price rises) for far longer than forecast.

The table highlights how Chinese home valuations are based almost purely on expected price appreciation. If forced to hold and rent, if the market tops out like Japan or the United States and enters a multi-year or multi-decade decline, returns will fall through the floor. For comparison, here’s a 2016 list of Top 20 Cities In U.S. For Investing In Real Estate Rentalsfrom Forbes. Most of the cities have yields around 5 percent, including Austin, TX. It is not a list of the cheapest bargains, rather its cities with good yields and good fundamentals such as population growth and job growth.

This table compares foreign and Chinese city rental yields. On the left is the city’s international grade. NY and London are A, Toronto and LA A, Orlando is C-, New Castle and New Orleans at the bottom. Comparable Chinese cities are on the right.

Some of those yields look good versus China’s most southern capitals:

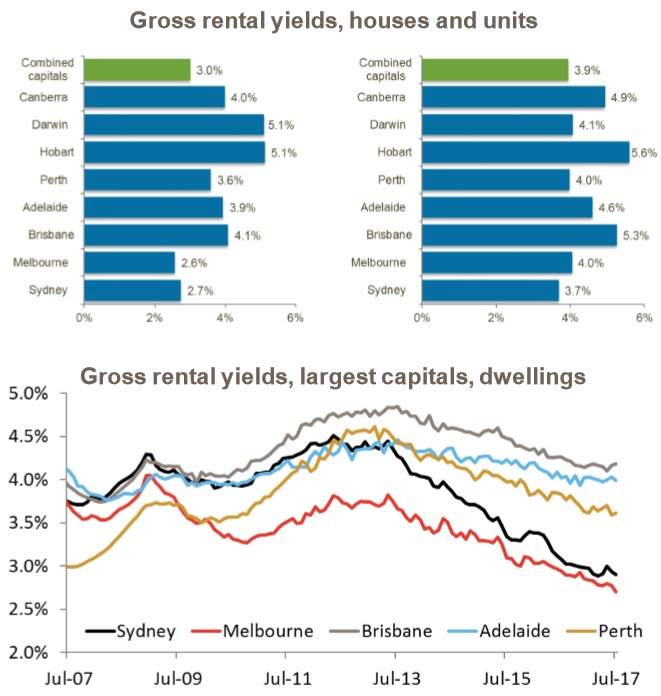

The rise in dwelling values across the combined capitals over the month has not been matched by a rise in weekly rental rates, which means gross rental yields have slipped lower over the month. Gross yields are once again at new record lows across the combined capital cities, driven by further falls in yields across both Melbourne and Sydney…

Over the past five years, gross rental yields have compressed across every capital city apart from Hobart where yields are unchanged at a reasonably healthy 5.2%. The most substantial decline in rental yields has been in Sydney, where dwelling values are up 77.3% compared with a 15.5% rise in weekly rents.

Advertisement

Why did we ever let the Chinese loose in our housing market?

David Llewellyn-Smith is Chief Strategist at the MB Fund and MB Super. David is the founding publisher and editor of MacroBusiness and was the founding publisher and global economy editor of The Diplomat, the Asia Pacific's leading geo-politics and economics portal.

He is also a former gold trader and economic commentator at The Sydney Morning Herald, The Age, the ABC and Business Spectator. He is the co-author of The Great Crash of 2008 with Ross Garnaut and was the editor of the second Garnaut Climate Change Review.