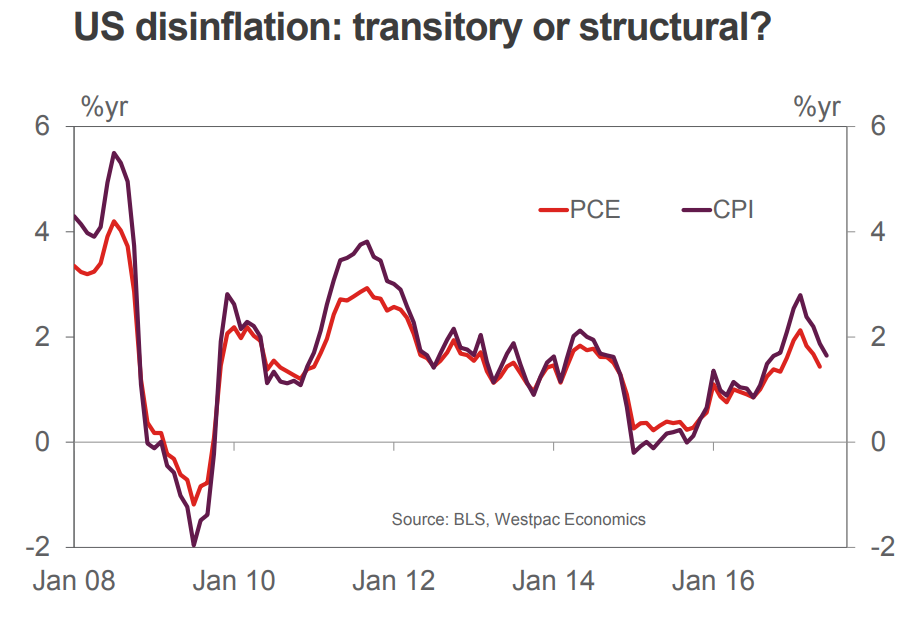

In recent months, uncertainty over the outlook for US inflation has grown. From a peak of 2.8%yr in February, headline CPI inflation abruptly fell back to 1.6%yr in June. Similarly core inflation (which excludes the impact of food and energy) slowed from 2.3%yr in January to 1.7%yr. Albeit only available to May, the FOMC’s preferred PCE measure has also slowed materially.

In their recent communications, the FOMC has continued to hold that this rapid deceleration in the inflationary pulse is a temporary phenomenon, not evidence of emerging economic weakness. Sharp declines in prescription drugs (now reversed) and wireless telephone services have been put forward as the primary causes.

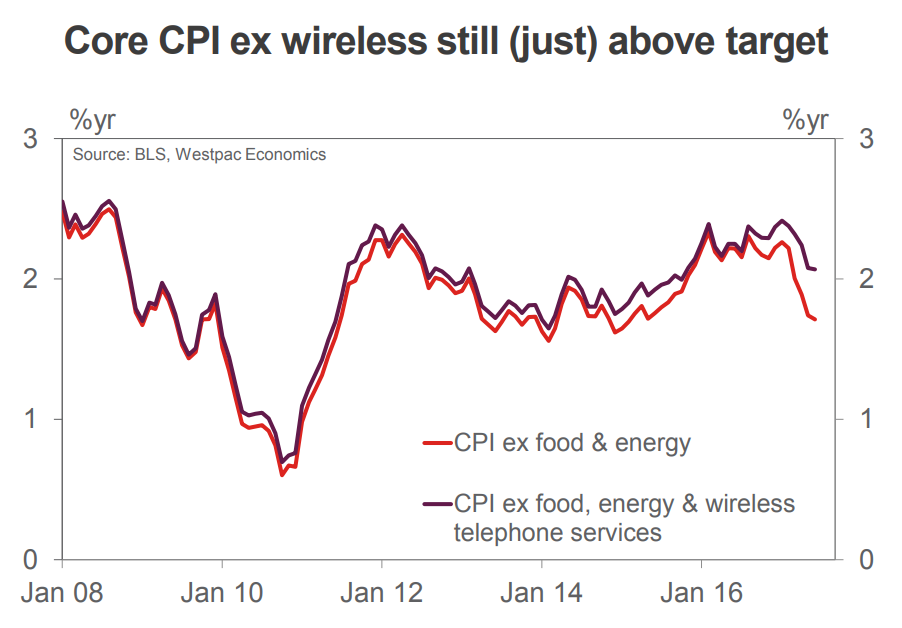

If we dig into the detail of the CPI report, we do indeed find that the unusual weakness in wireless telephone services has had a sizeable impact on headline and core inflation despite its comparatively small weight of less than 2%.

If we omit this component from the annual core inflation calculation, then instead of an annual gain of 1.7%yr at June, an estimate of 2.1%yr is produced – only 0.3ppts below its peak and still above the 2.0%yr medium-term target of the FOMC. Here there is clearly no cause for concern.

Still, to make sure that the ‘unexplained’ 0.3ppt slowdown in core inflation (ex wireless) is also not the beginning of a structural downtrend, it is worth considering its cause. Below all core inflation figures exclude food, energy and wireless services.

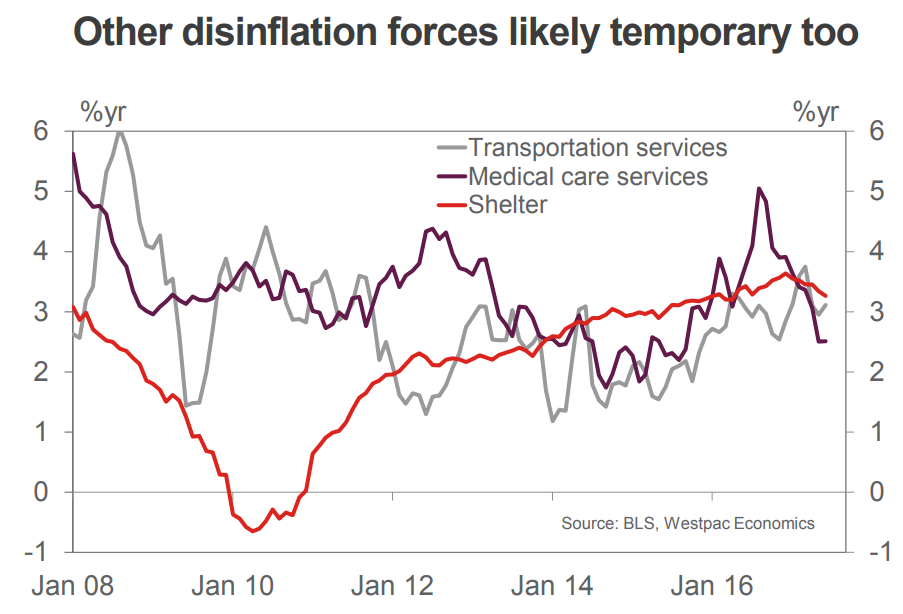

Within the service components, there are two other factors which look to be having a temporary, negative impact on core inflation.

While it only has an 8% weight, medical care inflation has had a material impact on core inflation in 2017, near –0.1ppt. This has occurred as inflation in the sector slowed from 3.4%yr in February to 2.5%yr in June. As it follows a spike to 5.0%yr in mid-2016 and is entirely concentrated in one sub sector (physician services, which are flat over the year versus a 2.5%yr 10-year average), disinflation in this component also looks transitory.

Transportation services is another area of the service economy that has seen slower inflation of late, but again this looks to be temporary. Through late-2016 and early-2017, the stronger US dollar looks to have weighed heavily on the cost of airline fares. Together with slightly softer vehicle maintenance charges, transportation services have edged annual core inflation down 0.03ppts since February. To the extent that the US dollar has since reversed its post-Trump gains, a reversal of this trend is likely; that would add to the inflationary pulse in late-2017. (Note, apparel and new cars have similarly subtracted from inflation.)

There is however one sub component for which the recent moderation could be structural: the slowdown in rent inflation. Housing (shelter) is the most important component of core inflation, having a weight of 43%. Because of this, the 0.2ppt fall in annual inflation since February has reduced core inflation by 0.1ppts – a third of the total fall in core inflation (ex wireless) since February. Given modest wage inflation and the ramp-up of housing supply, a sustained moderation in this key category would not be surprising. However, to the extent that the current annual pace for shelter inflation is more than a percentage point above its 10-year average, it is most likely the case that it will remain a robust support for total core inflation through 2017 and 2018.

The take home from this analysis is that the vast majority of the 2017 deceleration in core inflation has come from transitory factors as the FOMC have asserted. Further, the deceleration in shelter inflation, which may be structural, is from a high level, meaning it will likely still provide solid support for core inflation. We therefore see no need to alter our forecast of core inflation near the FOMC’s target in 2017 and 2018, 1.7%yr and 1.8%yr.

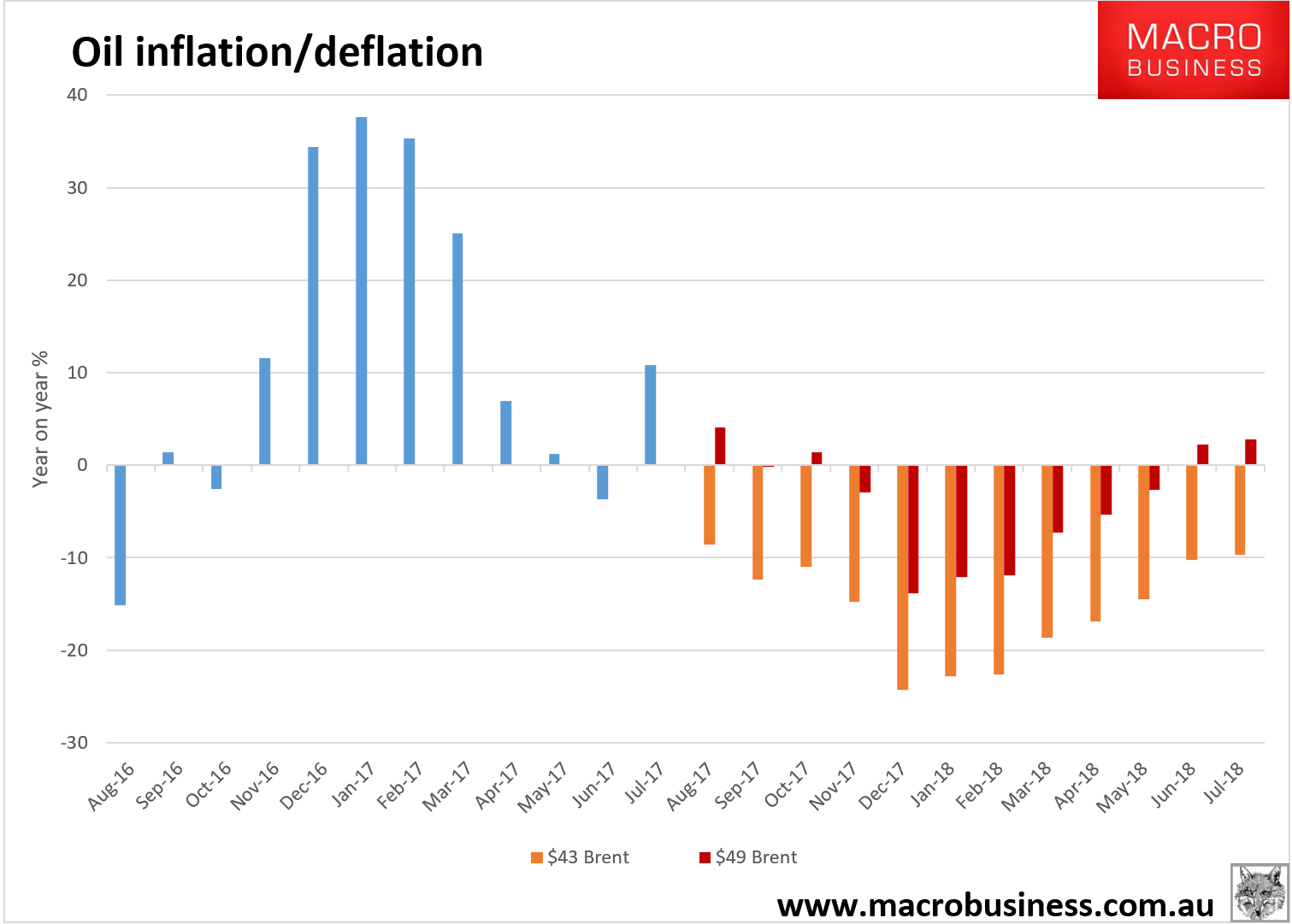

All good but about to be overtaken by one overriding factor, oil:

The Fed will have to hike into a deflationary gale by December.

David Llewellyn-Smith is Chief Strategist at the MB Fund and MB Super. David is the founding publisher and editor of MacroBusiness and was the founding publisher and global economy editor of The Diplomat, the Asia Pacific’s leading geo-politics and economics portal.

He is also a former gold trader and economic commentator at The Sydney Morning Herald, The Age, the ABC and Business Spectator. He is the co-author of The Great Crash of 2008 with Ross Garnaut and was the editor of the second Garnaut Climate Change Review.