Last night Canada hikes interest rates into its increasingly troubled housing correction as growth motors along nicely. Zero Hedge used a few charts from Deutsche to declare “Canada is in trouble”:

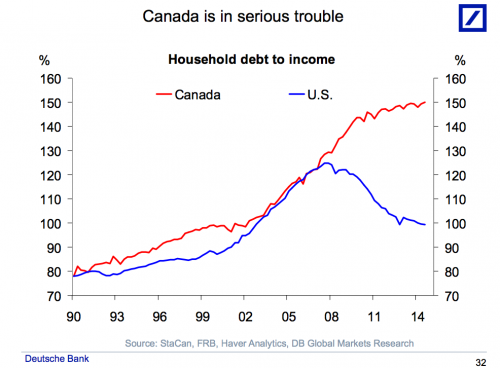

Some time ago, Deutsche Bank’s chief international economist, Torsten Slok, presented several charts which showed that “Canada is in serious trouble” mostly as a result of its overreliance on its frothy, bubbly housing sector, but also due to the fact that unlike the US, the average household had failed to reduce its debt load in time.

Using those four measures, you decide who is in trouble:

Canadian household debt to income is 150% versus Australia’s 190%;

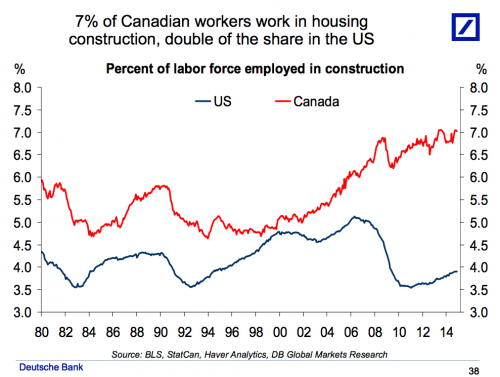

Canada’s 7% of worker’s in dwelling construction versus 9% Aussie workers in construction though it’s debatable how many are in dwellings;

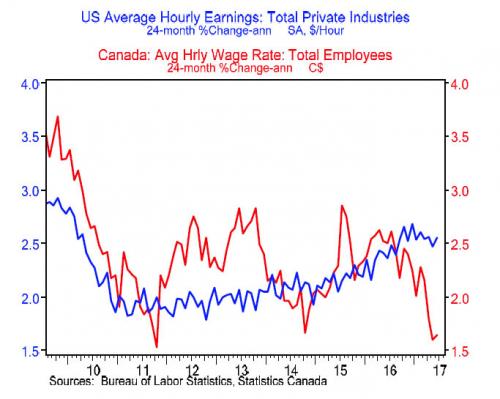

Canadian average hourly earnings are growing 1.5% versus Australia’s average compensation falling outright in nominal terms, and

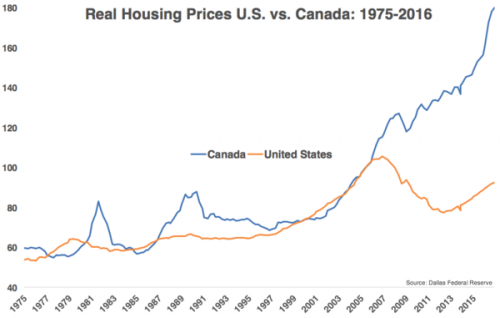

Canadian real house price growth since 1975 at 200% versus Australia’s 230%.

Advertisement

One more thing. Canada is much less dependent upon external financing that Australia with a much more diversified economy and export mix. Australia has less public debt but given it guarantees all of that offshore debt it’s probably more useless.

You may not accept the premise of the argument that Canada is in trouble but if you do then Australia is screwed!

David Llewellyn-Smith is Chief Strategist at the MB Fund and MB Super. David is the founding publisher and editor of MacroBusiness and was the founding publisher and global economy editor of The Diplomat, the Asia Pacific’s leading geo-politics and economics portal.

He is also a former gold trader and economic commentator at The Sydney Morning Herald, The Age, the ABC and Business Spectator. He is the co-author of The Great Crash of 2008 with Ross Garnaut and was the editor of the second Garnaut Climate Change Review.