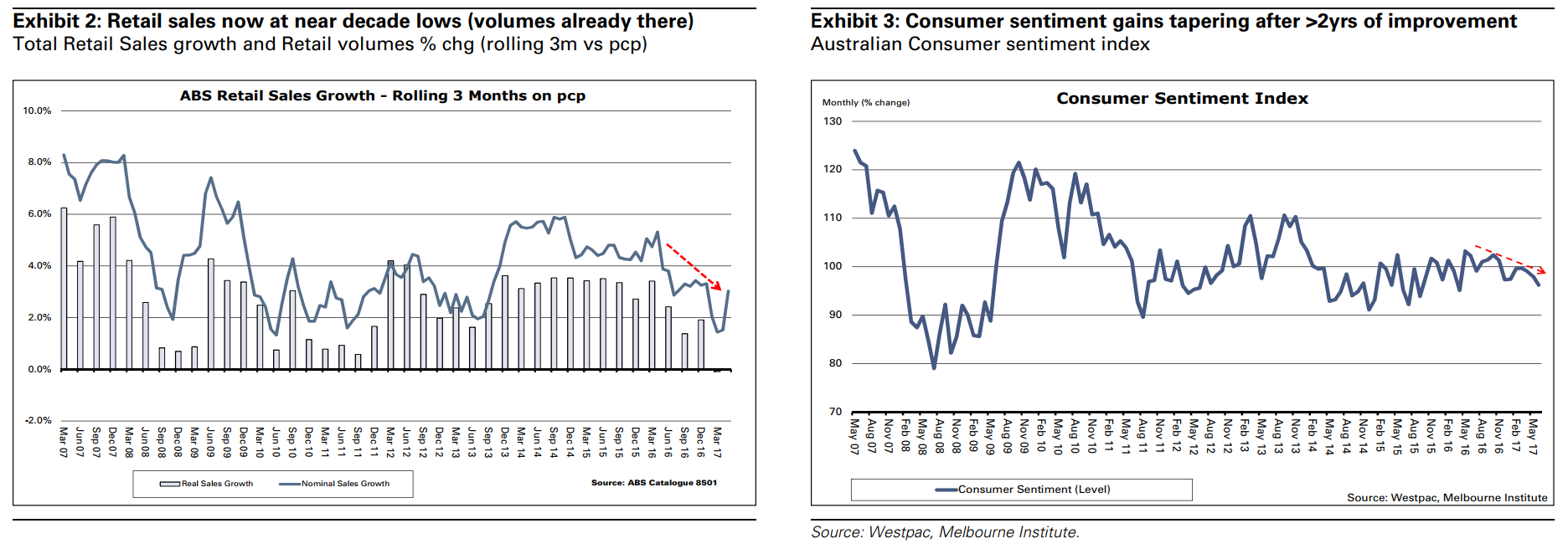

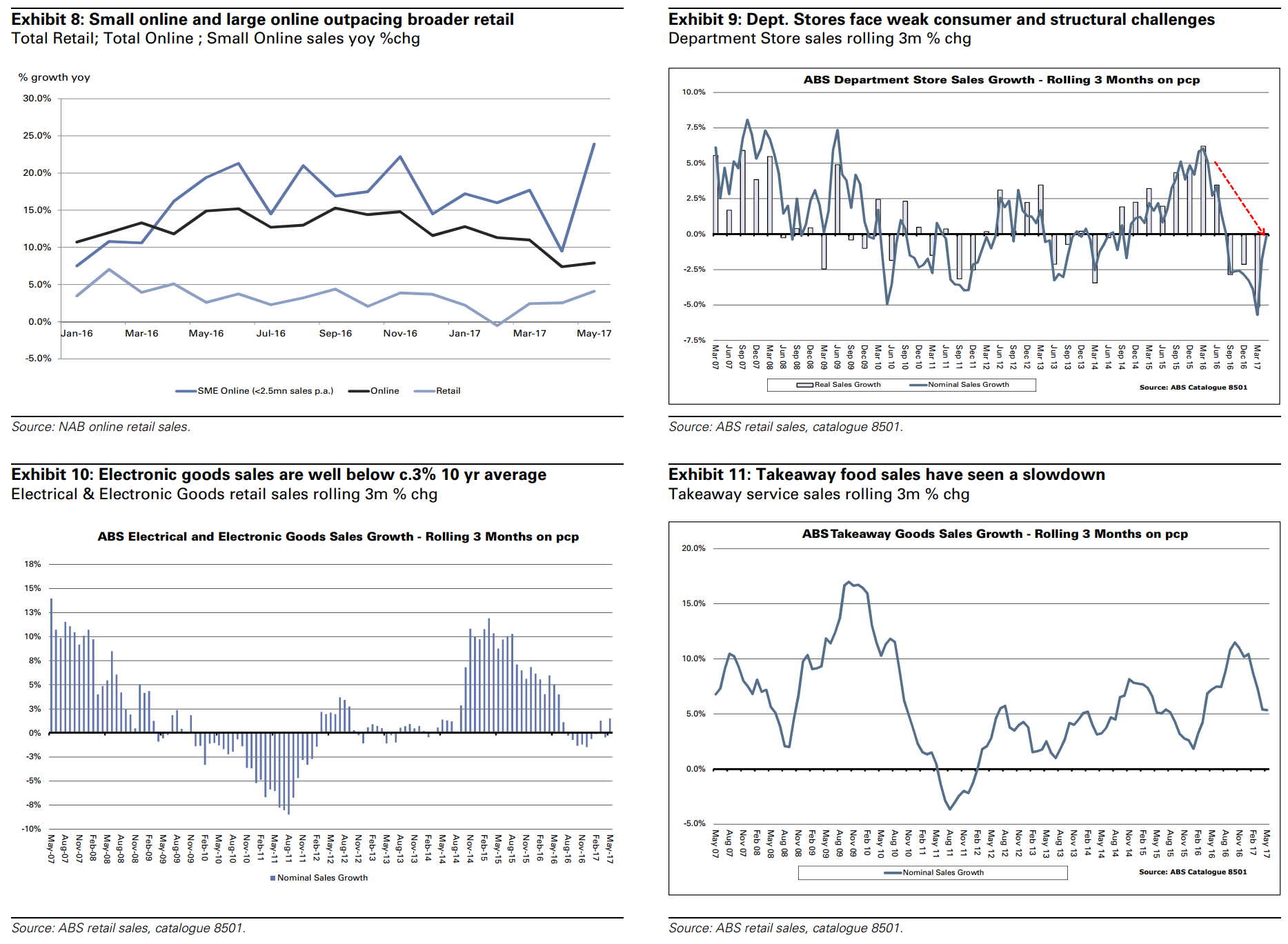

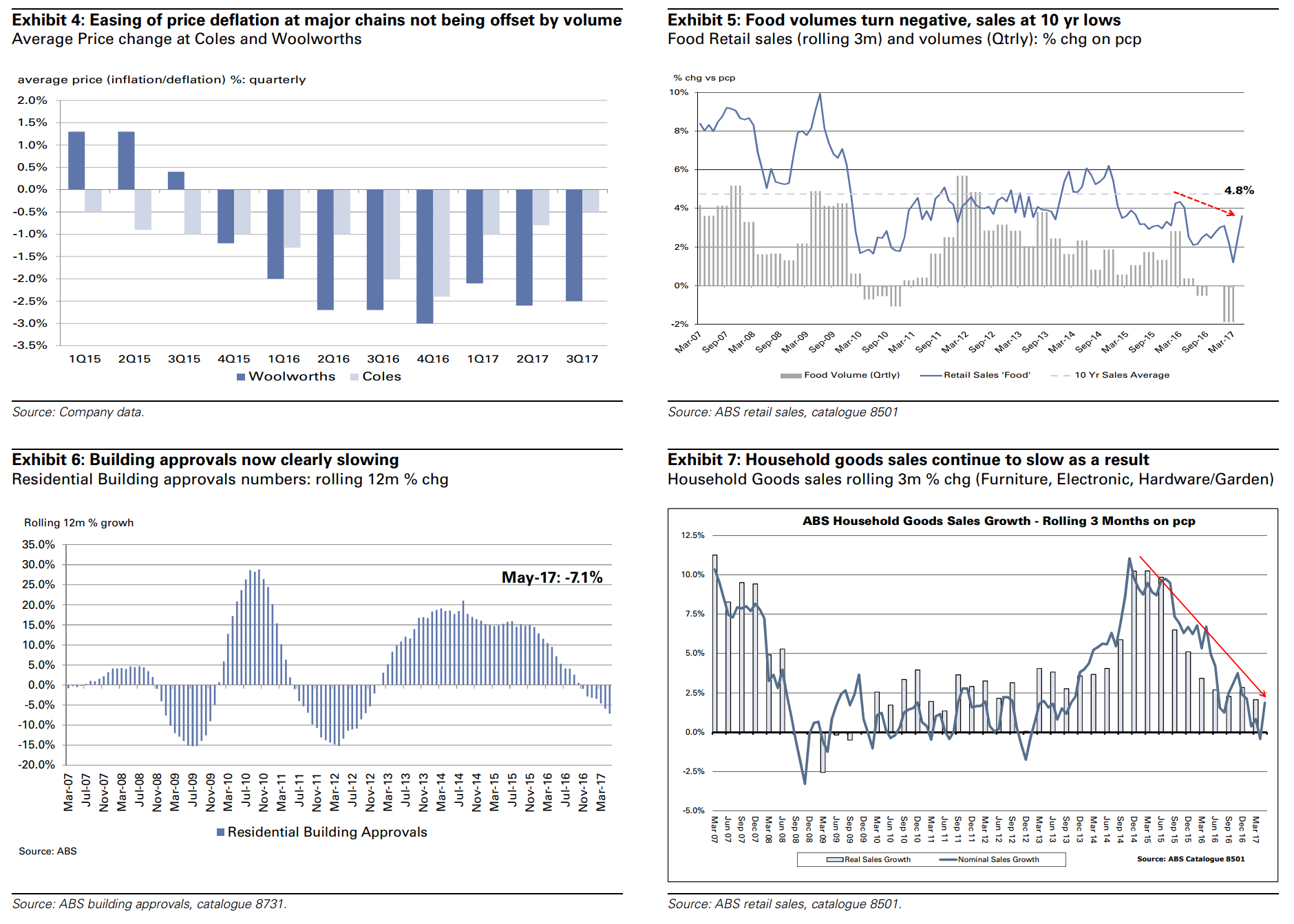

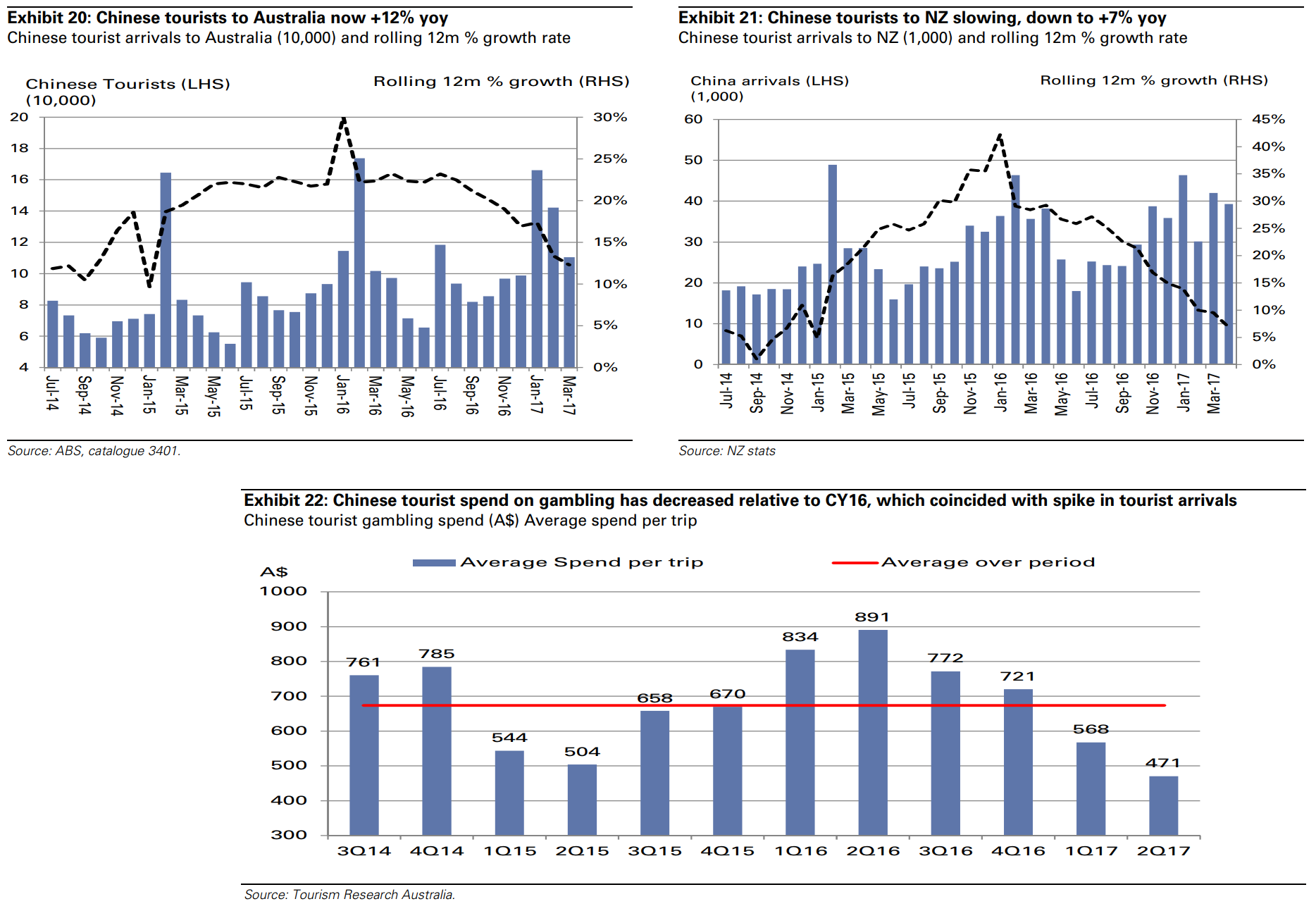

The consumer is under pressure in Australia on multiple fronts including rising power bills, petrol prices and interest rates. On the income side, wage growth is benign and consumer sentiment is waning. Recent data points YTD point to mixed sales and volume growth across all major retail categories, incl. Food, Household goods, and Department stores. Together this makes for a fairly subdued outlook for retail, consumer and entertainment stocks. In addition Electronic Gaming Machine (EGM) turnover growth is the lowest in 5yrs (although volatile month to month), Chinese tourism has slowed and visitors are spending less. NZ is an exception with EGM turnover continuing to report mid single digit growth. We see these data points manifesting in potential downside surprise risks to consensus estimates across the retail and gaming names in the upcoming FY17 reporting season. We trim our earnings estimates to reflect recent data points. (Exhibit 32). The charts below highlight the current state of the Australian consumer.

That’s every major category slowing or falling. Even Chinese visitors are pulling in the purse strings:

The full text of this article is available to MacroBusiness subscribers

David Llewellyn-Smith is Chief Strategist at the MB Fund and MB Super. David is the founding publisher and editor of MacroBusiness and was the founding publisher and global economy editor of The Diplomat, the Asia Pacific’s leading geo-politics and economics portal.

He is also a former gold trader and economic commentator at The Sydney Morning Herald, The Age, the ABC and Business Spectator. He is the co-author of The Great Crash of 2008 with Ross Garnaut and was the editor of the second Garnaut Climate Change Review.