Via Credit Suisse:

The currency conundrum Whilst the oil price continues to struggle to claw its way back towards US$50/bbl, the A$/US$ has had no such inhibitions in propelling its way through 79c. This presents an interesting conundrum for investors in the Australian Energy sector. The spot A$ oil price is sitting at just under A$62/bbl, yet our CS price and fx deck (US$65/bbl and 70c A$) implies an A$ price of ~A$93/bbl real from 1H18. With the pure E&Ps holding all their debt in US$ (not so for Origin), there is some valuation offset from a high A$. Perversely, the more financial leverage you have the greater the valuation offset, so Santos feels the pain least of a high A$.

■ Valuations on spot oil and fx somewhat alarming Without stating the obvious, all else equal a higher A$ is negative for the A$ valuation of businesses with revenues largely in US$ (Origin aside again). Whilst we are not proponents of oil never rising again to perpetuity (we have less intelligent things to say on the A$), if we ran both spot oil and fx through our models our valuations would be somewhat alarming with Woodside at A$17.50/sh, Oil Search A$4.15/sh, Santos A$1.90/sh and Origin A$4.10/sh. Clearly these numbers are more about the oil side of the equation than the fx part.

■ A$ sensitivities vary considerably Looking at just the A$ side of the spot valuation argument is interesting. Aside from Santos having a decent chunk of revenue in A$ for WA gas business, almost all revenues are in US$ for the pure E&Ps. Financial leverage, with again all debt in US$ for the pure E&Ps, is ironically the valuation offset. The more debt you have the greater the A$ valuation is mitigated from a high A$. Running spot A$ through with the CS oil deck sees valuations drop ~11% for Woodside and Oil Search to A$23.80/sh and A$6.30/sh, respectively, and by ~7.5% to A$3.50/sh for Santos. Origin, of course a different case given the base business and large levels of A$ debt, drops ~10.5% to A$6.90/sh. It is certainly worth noting for Origin that at spot fx APLNG FCF breakeven rises to ~US$46/bbl – not leaving much for shareholders currently.

■ A$ clearly, currently, a headwind to the sector The sector presents a tricky conundrum for us at present. Despite our above consensus oil price deck, the sector doesn’t exactly scream value. Yet, the reality is that if you believe oil is going to rise, it is intuitively unlikely the sector will fall against that. The A$ is a real thorn in the side of the sector, from a valuation perspective, at present though. As we have noted numerous times before, history shows few examples of a rising oil price and falling A$. Yet our macro assumptions, along with most in the market, have oil in contango and the A$ in backwardation. If nothing else, we believe the sector needs to be brought into the investment debate when looking at the A$. Santos continues to boast the most upside to our valuations, but of course remains for the brave given risks. For us, risks around a higher A$ is yet another nail in the valuation coffin for Woodside. So Oil Search for the more risk averse, Santos for the brave. Without flogging a long ago perished horse, Caltex still seems the best place for money in the sector though.

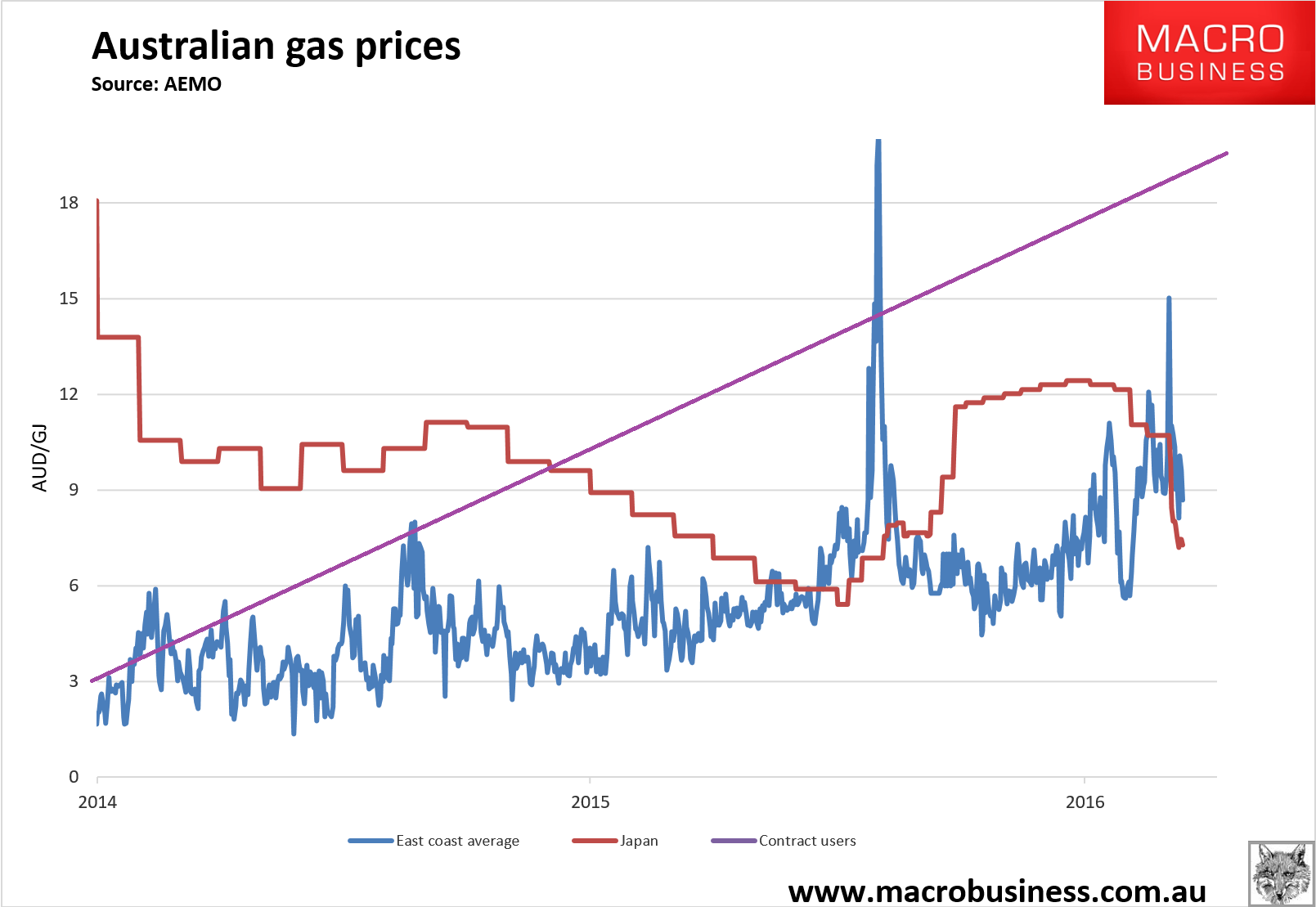

No problem. They can just gouge the locals to make up for it. To wit:

Santos has clocked up further progress on reducing costs and debt, while also upgrading guidance for full-year production and sales.

In its quarterly report released on Thursday, Santos said it now expects to break even on a cash flow basis at an oil price of $US33 a barrel, down from $US36.50 last year.

At the end of the March quarter it had reduced the break-even oil price to $US34 a barrel.

Guidance on production costs has been reduced to $US8-$US8.25 per barrel of oil equivalent, down from $US8.45 last year.

Santos’s large debt burden is slowly falling, down to $US2.9 billion at the end of June, down some $US600 million since the end of December.

Guidance on output for 2017 has been slightly upgraded and is now expected to be between 57 million and 60 million barrels of oil equivalent. Santos was previously stating a lower end of the range of 55 million boe.

Of course guidance is up, right along with local gas prices:

When you can sell gas for $20Gj produced for $2GJ you can even overcome selling most of to Asia at a loss.

Go Straya.