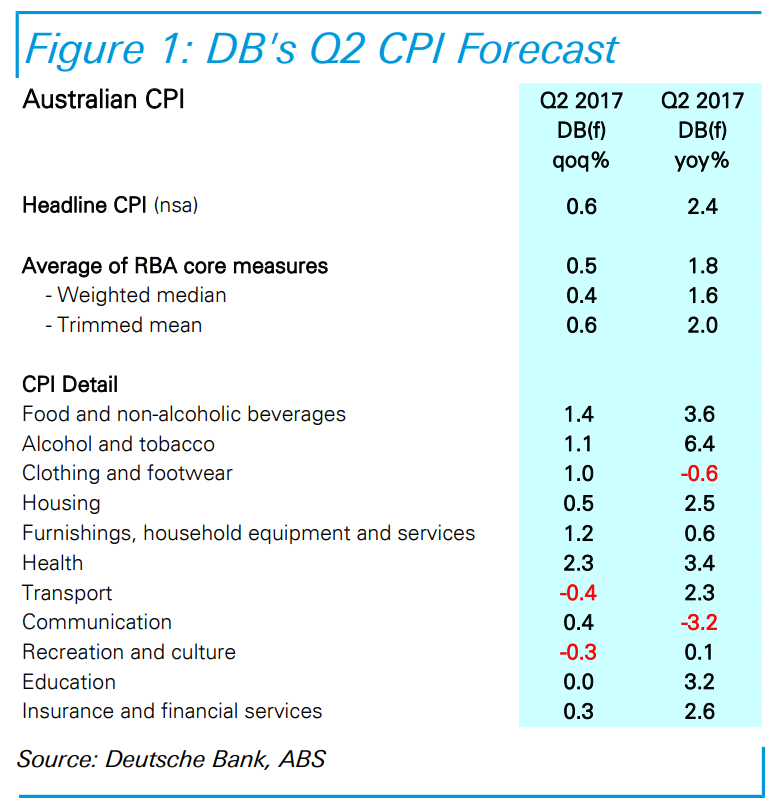

DB’s forecast for Q2-17 headline CPI at 0.6%qoq/2.4%yoy; average of the core measures at 0.5%qoq/1.8%yoy

Our forecast for Q2 headline CPI is for a 0.6%qoq outturn, a touch stronger than the 0.5%qoq the headline prints seen in Q4-16 and Q1-17. This leaves the CPI at 2.4% over the year. We expect underlying inflation to remain subdued, with our estimate for the average of the core measures at 0.5%qoq/1.8%yoy.

Vegetable prices, especially tomatoes, appear to have been impacted by Cyclone Debbie in late March. The scheduled 1 March rise in tobacco excise (reflecting indexation to average weekly ordinary time earnings) is the key driver behind the 1.1%qoq rise in the ‘alcohol and tobacco’ group (note the 1 March excise date has the effect of raising the average tobacco price across Q2 compared to Q1). June tends to be a seasonally strong quarter across a number of expenditure items in the ‘clothing and footwear’ group, though we have been conservative here in line with anecdotal evidence pointing to discounting by retailers. While we expect rents to have remained soft in the quarter, we have factored in another relatively strong rise in ‘new dwelling purchase’ after the 1.0%qoq rise in Q1-17 (strength here reflecting the elevated level of dwelling construction activity at present). Elsewhere, seasonal strength drives our pick for the ‘furnishings, household equipment and services’ and ‘health’ groups, with the latter impacted mainly by rises in annual private health insurance premiums from April 1. Fuel prices look to have fallen a little under 3%qoq, the key factor behind the fall we have factored for the ‘transport’ group. We have factored a further fall in ‘domestic holiday travel and accommodation’, which has weighed on the ‘recreation and culture group’. Finally, the ‘education’ and ‘insurance and financial services’ groups typically show minimal price changes in Q2.

We expect ongoing softness in wages growth to keep core inflation subdued. Our estimate for the average of the two RBA measures is at 0.5%qoq, leaving yearended underlying inflation at 1.8%yoy, this is broadly in line with the forecasts outlined by the RBA in the May Statement on Monetary Policy.

A large rise in utility prices, coupled with tobacco, to see stronger headline inflation in Q3 Our early expectation is for a stronger headline inflation print in Q3 of 0.9%qoq. Underpinned by sharp rises in electricity and gas prices in three states (NSW, Queensland and South Australia), we expect utilities to lift by around 7%qoq in the quarter. Tobacco prices will also be impacted by a 12.5% increase in scheduled excise on September 1, and there is some risk, in our view, that fruit and vegetable prices could strengthen further as the impact of Cyclone Debbie continues to flow through to the retail level. This leaves us with a (very) early pick for headline CPI print for Q3 of around 0.9%qoq. Of course, we will refine this estimate as the quarter progresses (the evolution of relatively highly weighted and volatile items like fruit, vegetables and automotive fuel will obviously be key).

David Llewellyn-Smith is Chief Strategist at the MB Fund and MB Super. David is the founding publisher and editor of MacroBusiness and was the founding publisher and global economy editor of The Diplomat, the Asia Pacific’s leading geo-politics and economics portal.

He is also a former gold trader and economic commentator at The Sydney Morning Herald, The Age, the ABC and Business Spectator. He is the co-author of The Great Crash of 2008 with Ross Garnaut and was the editor of the second Garnaut Climate Change Review.