by Chris Becker

Asian markets start the week strongly as the Chinese manufacturing PMI contained no surprises even as tensions on the Korean peninsula mount up. Japanese stocks were the only ones to tread water as the Yen remains very strong against USD, while iron ore, copper and other commodities jumped helping Aussie resource stocks.

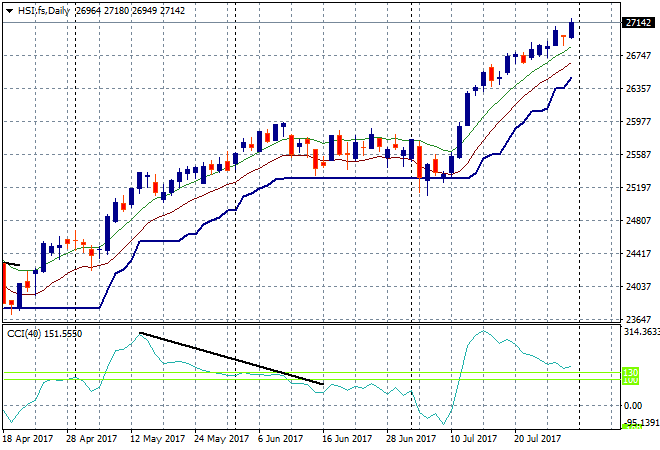

In mainland China the Shanghai Composite has started with a bang, up 0.5% coming into the close, now at 3270 points as it reaches for the next obvious resistance at the 3300 point level. The Hong Kong based Hang Seng Index is doing even better, up 1% after its recent breakout move above 26,000 points and accelerating away!

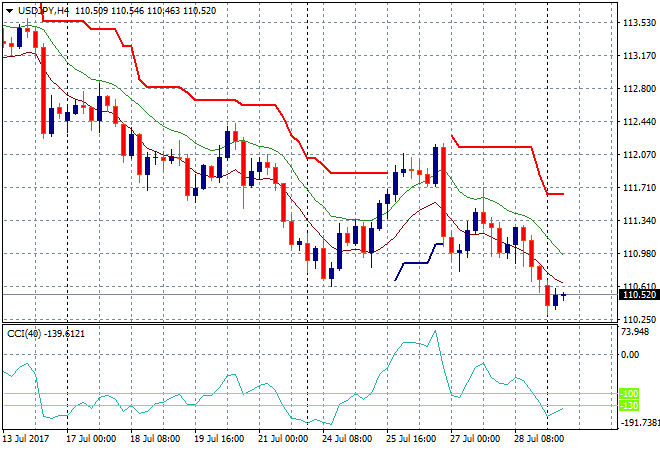

Japanese stocks have closed with scratch sessions after being down earlier. The Nikkei finished at 19959 points, still below the psychological important 20,000 point level which is firming everyday as significant resistance. The USDJPY pair is barely holding here at the 110.50 level after Friday nights late selloff which took out weekly support, so watch out below:

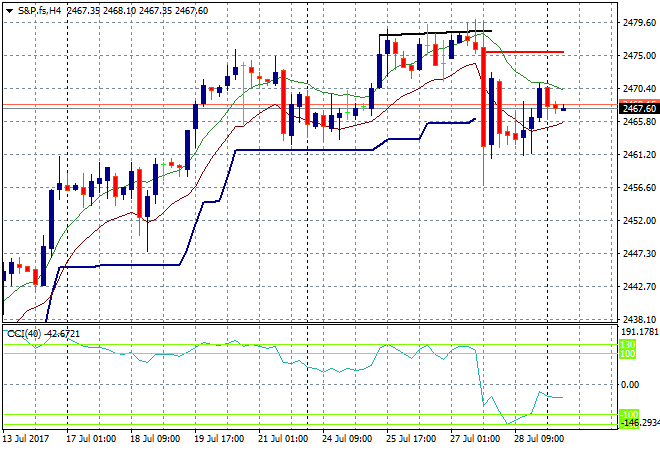

S&P futures are still on low volumes as we head into another week of volatility mainly due to the White House shenanigans and front-stabbing:

The ASX200 closed up 0.3% giving back some of its intrasession gains after being up nearly twice that after the lunch break. The big winners were resource stocks with BHP up 2.4%, RIO up nearly 3% and Fortescue reaching for nearly 6% higher.

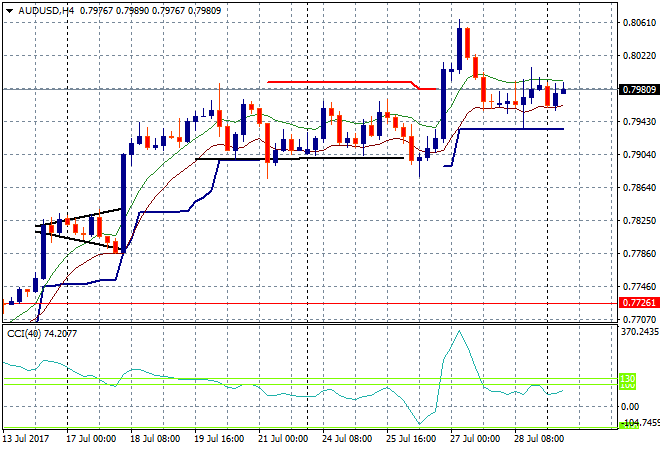

The Aussie dollar was basically unchanged throughout the Asian session, staying below the 80 handle against USD on low volume. The 79 handle remains the short term Uncle Point which looks to be firming up here even as the four hourly and hourly price action sets up for a small retracement:

The data calendar starts the week overseas with German retail sales and EZ wide CPI estimate for July while pending home sales in the US will be the highlight.