by Chris Becker

A mixed start to the week for risk markets outside China as traders prepare for a tumultous week of US earnings, CPI prints and finally the Federal Reserve’s latest take on where the world’s biggest market – government bonds – will turn as it reassesses its interest rate trajectory.

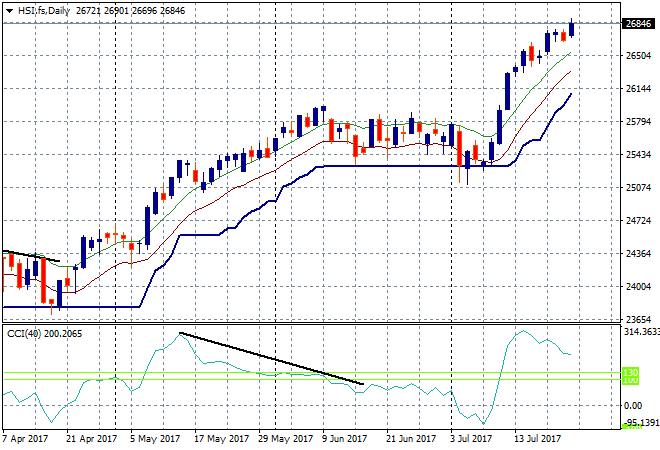

In mainland China the Shanghai Composite had a brighter start than most, lifting nearly 20 points or 0.6% to 3257 to build above previous resistance, now support at 3200 points. The Hong Kong based Hang Seng Index is up about half that, or 0.3% to 26796 points, building on its recent breakout above 26,000 points. There is room here for a retracement as daily momentum is indeed reverting to mean:

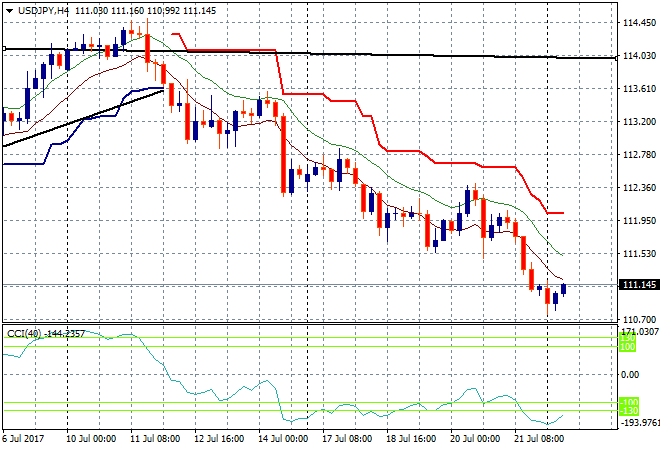

Japanese stocks slipped to start the week even as Yen weakened ever so slightly in the Asian session, it was more about reaction to Friday’s big selloff. The Nikkei finished down 0.5% to be back below its psychological important 20,000 point level. The USDJPY pair lifted back above the 111 handle today but is poised to go lower in the medium term leading into the Thursday FOMC meeting:

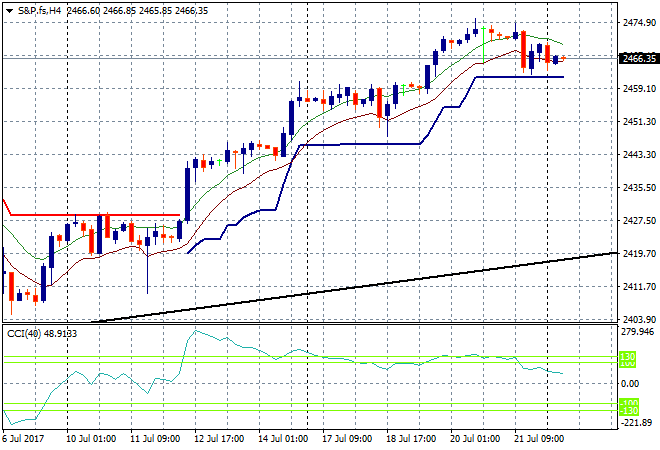

S&P futures are coming off slightly as some big guns report earnings tonight:

The ASX200 has cracked below its closely watched 200 day moving average, down 0.6% down to 5688 points, matching the February low. This was on the back of the higher dollar on Friday and the hawkish mood surrounding the confused RBA with bank stocks off 1% or more.

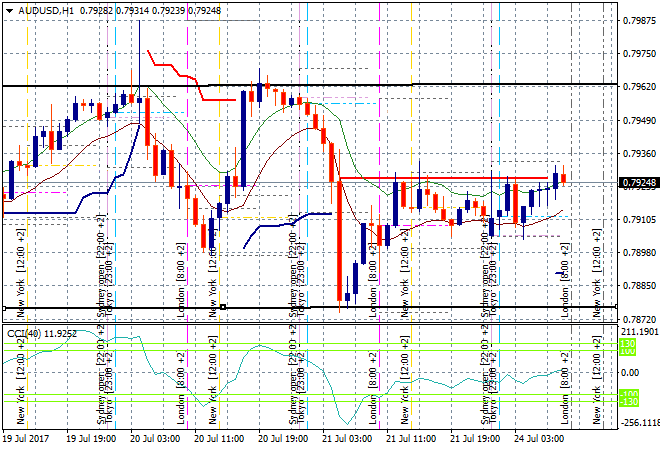

The Aussie dollar is holding at its Friday session highs just above the 79.20 level against USD, starting to accelerate coming into the London open. The level to beat is the upper end of this rectangle pattern on the hourly chart at the 79.60 level:

The data calendar starts its very busy week with a slow Monday night, namely some preliminary PMI prints, but the real focus will be on US earnings.