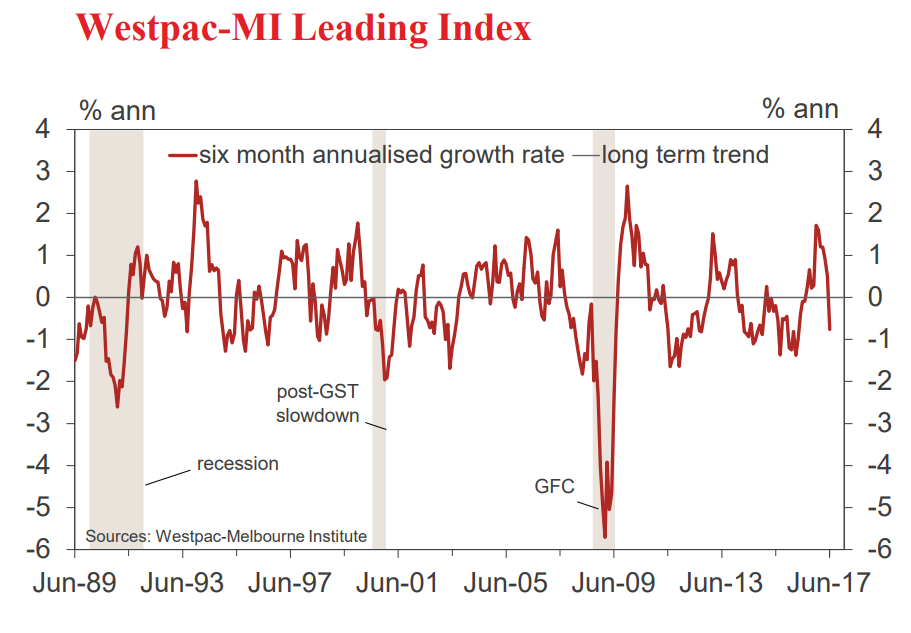

• The six month annualised growth rate in the WestpacMelbourne Institute Leading Index, which indicates the likely pace of economic activity relative to trend three to nine months into the future, fell sharply from 0.51% in May to –0.76% in June.

The index is pointing to a slowdown in momentum in Australia’s growth profile with the first below trend reading since July 2016. The deterioration mainly reflects international factors including a sharp turnaround in Australia’s commodity prices in Australian dollar terms.

The Leading Index growth rate has slowed from 1.61% above trend in January to 0.76% below trend in June (a deterioration of 2.37ppts). Two components account for all of the reversal: commodity prices and the yield spread. After surging 42% over the second half of 2016, Australia’s commodity prices have fallen 17% over the first half of 2017 in AUD terms. The swing has seen this component alone go from adding 1.26ppts to the Leading index growth rate in January to subtracting 0.71pts off in June, a reversal worth 1.97ppts. Some of this reflects the unwinding of temporary policy and weather-related spikes in coal prices. However, a strong rally in iron ore prices through much of last year also moved into reverse from early 2017 through mid-June.

While we have seen a solid recovery in iron ore prices since mid-June in USD terms, the sharp increase in the Australian dollar from USD 0.755 to USD 0.79 will partly offset that adjustment.

The yield spread – the difference between the short and long term interest rates – captures financial market assessments of the economic outlook both locally and abroad (long term rates are heavily influenced by benchmark rates abroad). After widening significantly over the second half of 2016, the yield gap has narrowed sharply in 2017, led by lower 10yr bond rates as markets have pared back expectations for growth stimulus policies in the US and inflation expectations ease. The move has taken 0.64ppts off the Index growth rate since January.

A lift in US industrial production has provided some positive offset, adding 0.23ppts to the Leading Index growth rate between January and June. However the domestic components of the Index have been lacklustre overall. The labour market has been slightly more supportive with aggregate hours worked adding 0.02ppts and the Westpac-MI Unemployment Expectations adding 0.04ppts to the Index growth rate over the last six months. On the other hand, dwellings approvals (0ppts), the Westpac-MI CSI expectations (–0.03ppts) and ASX200 (0ppts) have not worsened over the last six months but continue to exert a steady drag on the Index. 19 July 2017

The Reserve Bank Board next meets on August 1. We expect the Bank to leave rates unchanged at that meeting.

Markets have quickly moved to price in rate hikes in Australia in 2018 partly in response to the Reserve Bank’s July Board minutes which set out the Bank’s revised estimate of ‘neutral’. Since the GFC it has become clear that the new neutral rate will be lower than in previous years due to lower inflation; and lower trend growth particularly reflecting lower productivity growth and high risk aversion associated with excessive household debt. It is helpful that the Bank has finally put on record its assessment that ‘neutral’ has fallen from 5% to 3.5% (1% real and in line with thinking at the US Federal Reserve).

All central banks need to be assessing that target but this does not mean that a Bank is necessarily ready to begin tightening. The timing of that decision will come down to the state of the economy. Westpac expects that growth in 2018 will be a below trend 2.5% with limited prospects of that improving much in 2019. Furthermore that growth rate is unlikely to be associated with much improvement in the labour market with considerable spare capacity likely to remain for some time.

The Reserve Bank has forecast 3.25% growth in 2018 and 2019 (year to June). With that profile they may be ‘expecting’ to begin the tightening process but with inflation below the bottom of the target range; the housing market cooling under the weight of regulators’ macro prudential policies; and benign wages growth they have ample time to assess the reliability of that view.

We expect that as the Bank is forced to revise down its growth and inflation forecasts through the remainder of this year and 2018 the need to raise rates will dissipate.

Yep. Unless house prices don’t slow but they should…

David Llewellyn-Smith is Chief Strategist at the MB Fund and MB Super. David is the founding publisher and editor of MacroBusiness and was the founding publisher and global economy editor of The Diplomat, the Asia Pacific’s leading geo-politics and economics portal.

He is also a former gold trader and economic commentator at The Sydney Morning Herald, The Age, the ABC and Business Spectator. He is the co-author of The Great Crash of 2008 with Ross Garnaut and was the editor of the second Garnaut Climate Change Review.