As slow wage growth and lacklustre GDP figures weigh on the economy, expectations for sales, profits and capital investment are down for the third quarter of 2017 according to Dun & Bradstreet’s June Business Expectations Survey. Upbeat employment and selling prices expectations provide some positive news, but the forecast is for choppy waters ahead.

According to Dun & Bradstreet Economic Adviser Stephen Koukoulas: “The overall cautious tone of business expectations remains, with the final result consolidating lower confidence for the September quarter. Actual activity also remained soft and lags well behind expectations. The components of the survey are providing a leading indicator on the hard data for the economy, particularly the apparent conflict between a downturn in sales and the rise in employment.”

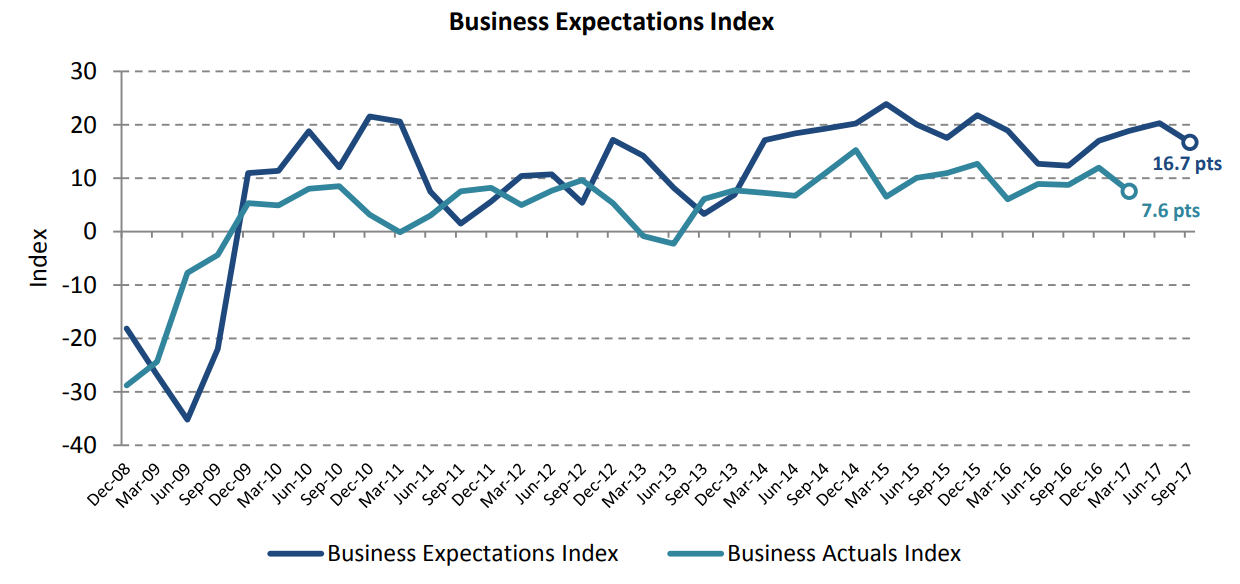

Dun & Bradstreet’s Business Expectations Index, the average of the survey’s measures of sales, profits, employment and capital investment expectations, fell to 16.7 points for the September quarter of 2017, down 17.6 percent from 20.3 points from the June quarter 2017, but up 26.2 percent from 12.4 points in the previous corresponding period. The final Q3 2017 result is 7.5 points above the 10-year average of 9.2 points.

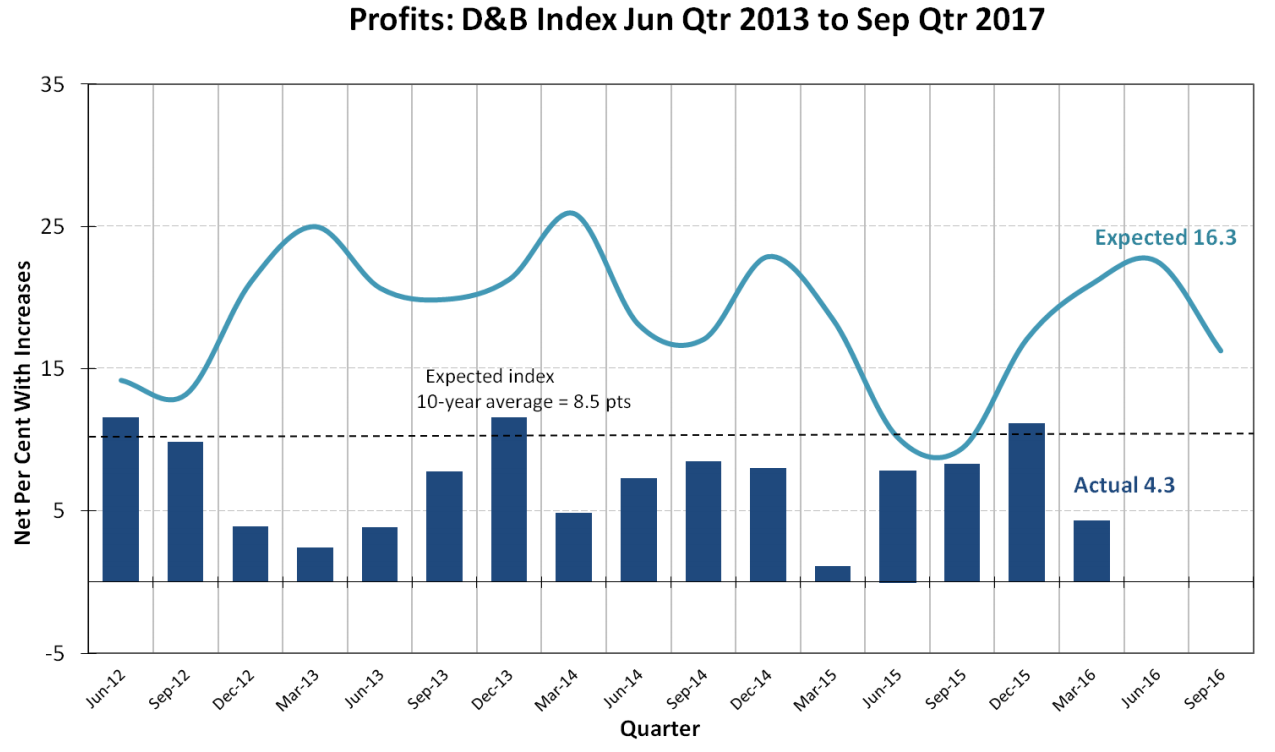

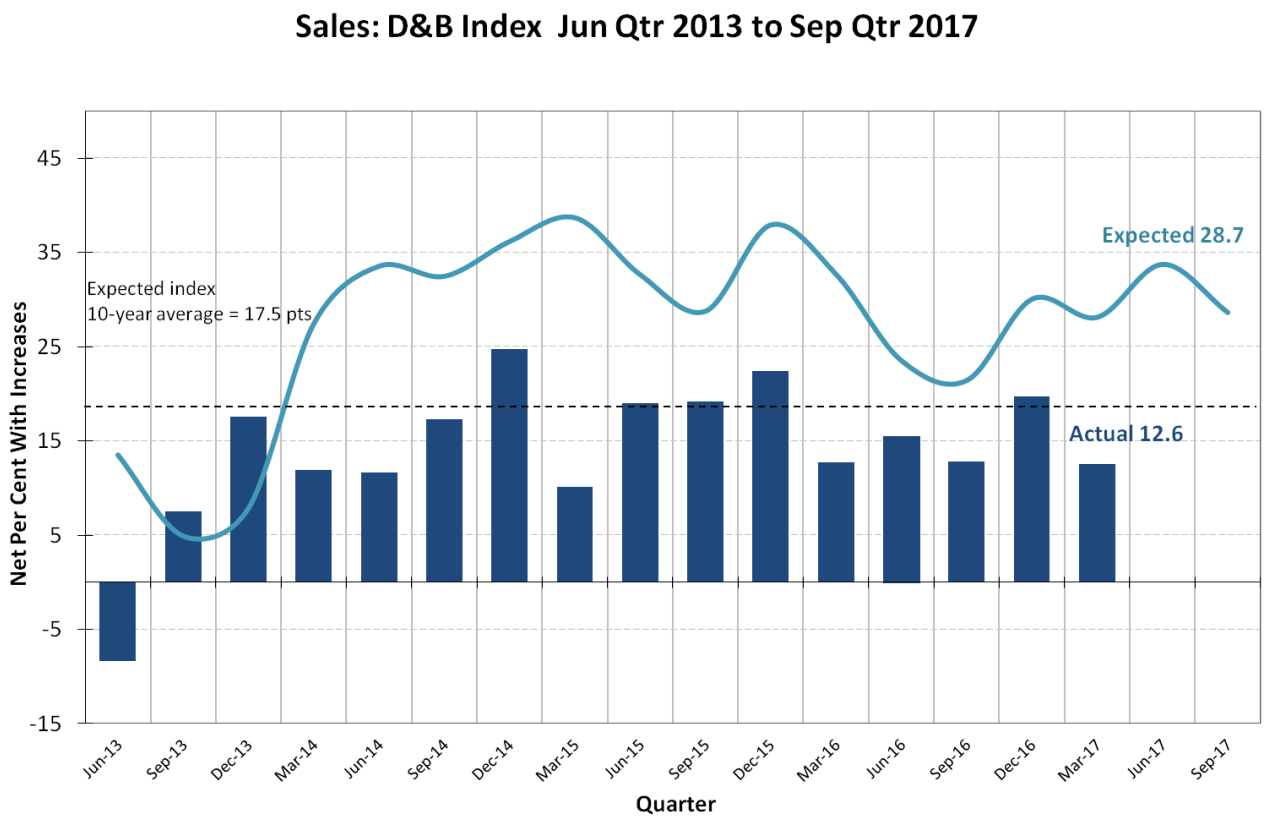

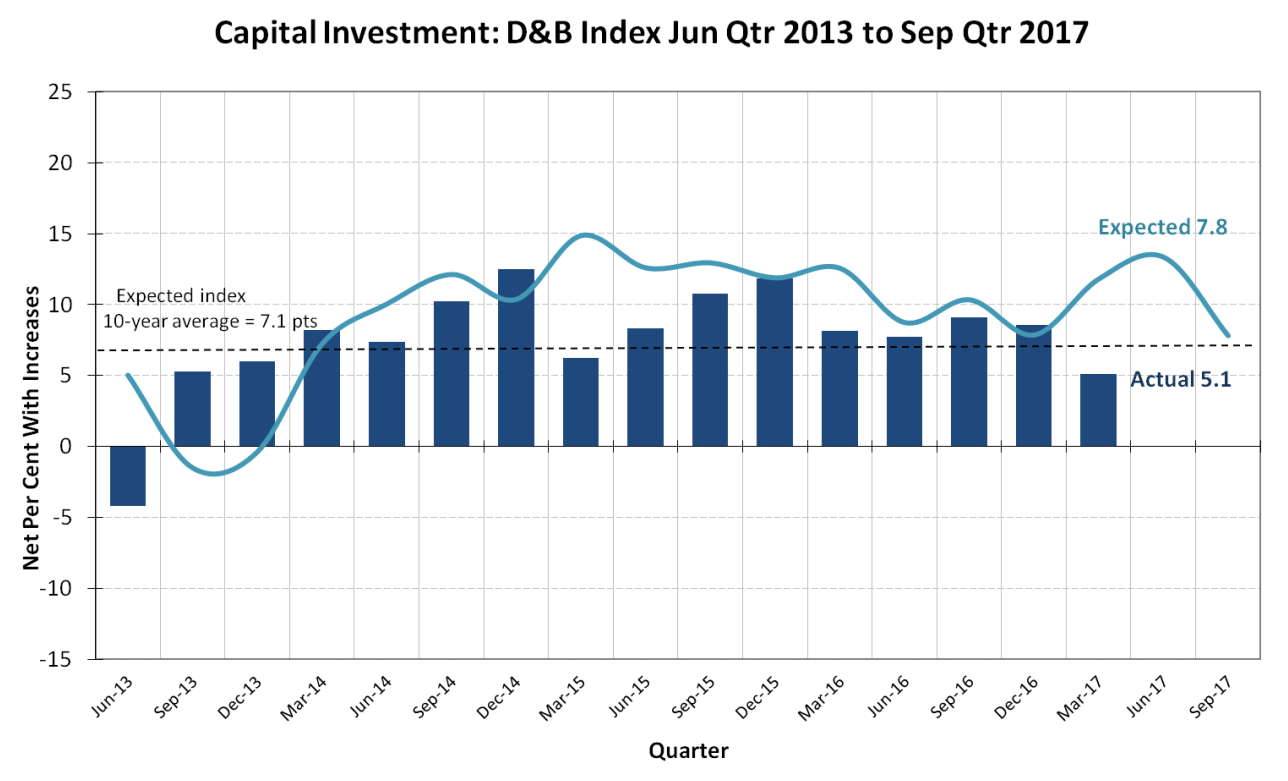

The sales, profits and capital investment expectations indices for Q3 2017 fell 15.1 percent, 27.9 percent and 41.4 percent, respectively, on the previous quarter. However, expectations for profits are up 42.3 percent on Q3 2016.

“The consistent fall in expectations for sales, profits and capital expenditure is concerning. If these trends are reflected in future data, the outlook for the economy will be problematic and it may cause the Reserve Bank of Australia to revisit its upbeat view on future growth. This is especially the case with expected capital expenditure, which has weakened to its lowest level since the March quarter of 2014,” Mr Koukoulas said.

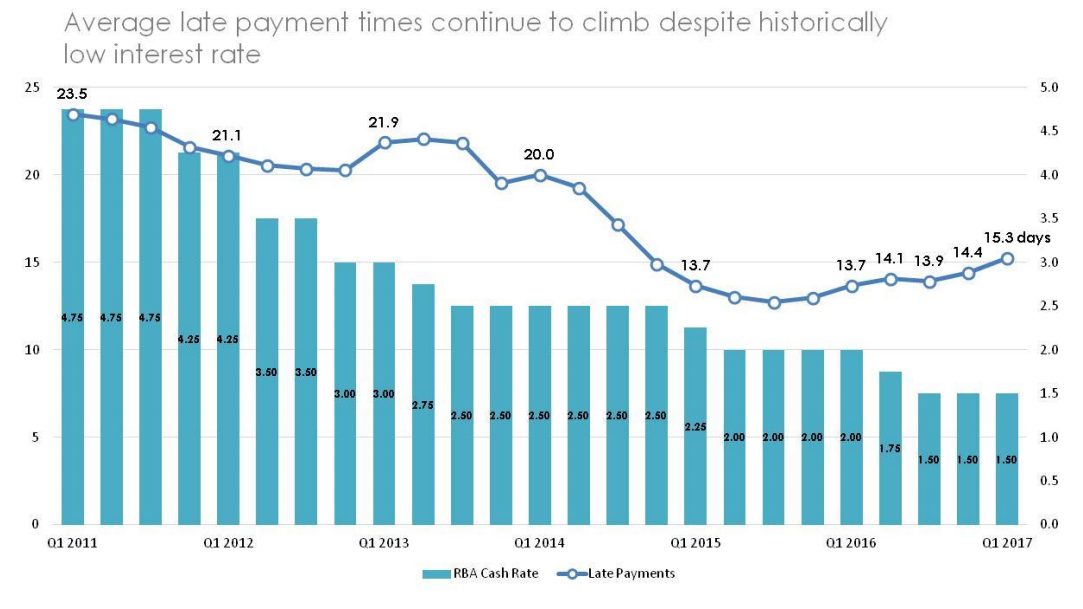

The slide in confidence has also been reflected in Dun & Bradstreet’s Australian Late Payments Analysis, which saw late payments in the first quarter of 2017 rise to their highest level since Q3 2014.

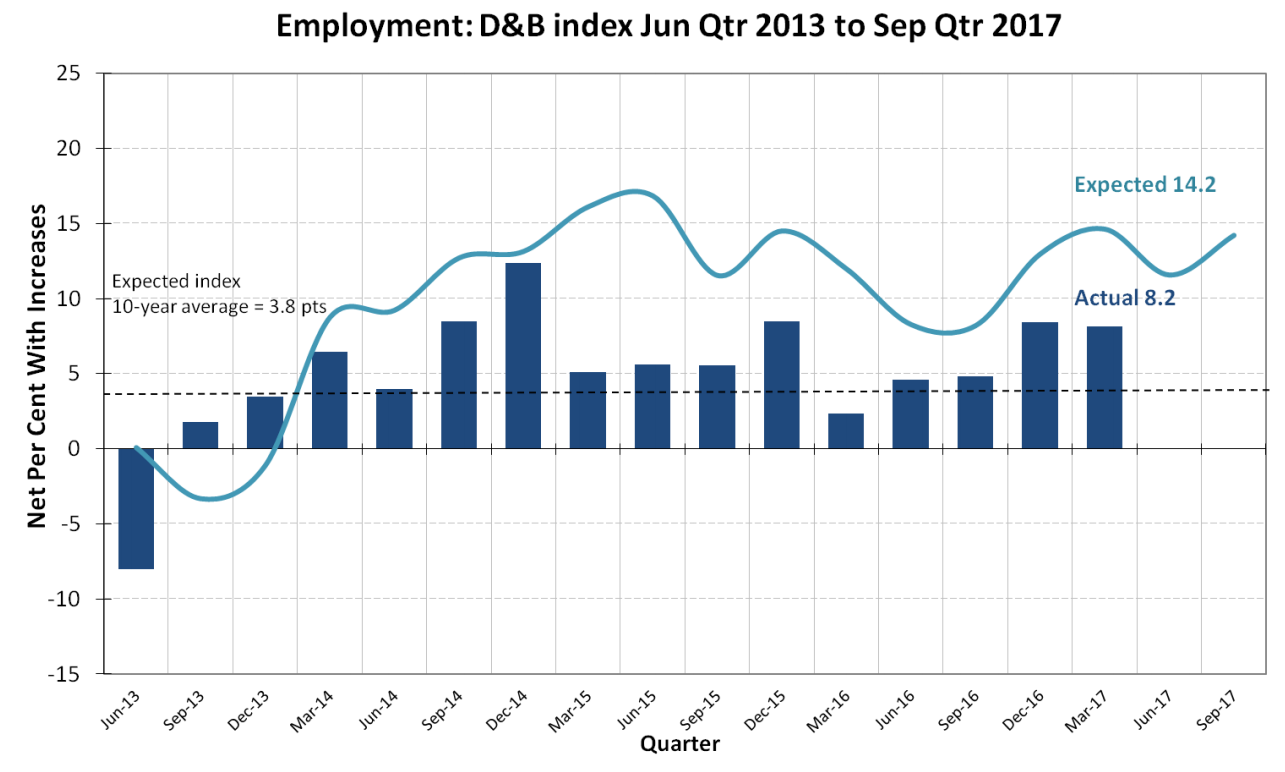

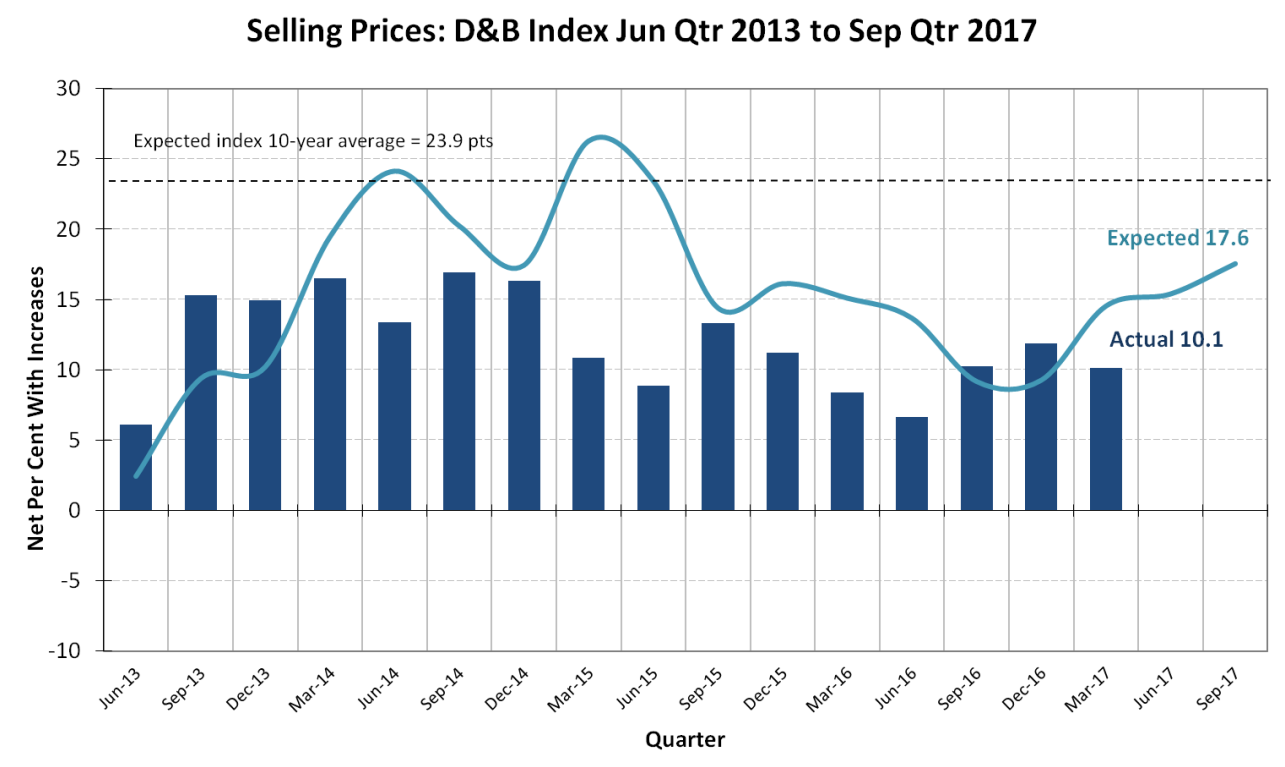

Expectations for employment in the quarter ahead stabilised at 14.2 points following a momentary dip to 11.6 points in the June quarter. Meanwhile, selling prices expectations for the September quarter climbed to a two-year high of 17.6 points, compared to 15.4 points in the June quarter and 9.2 points for the September quarter of 2016.

“The acceleration in expected selling prices is another red flag. As a reliable leading indicator of the official inflation data, the lift in expected selling prices, to a two year high, suggests that inflation will accelerate into the second half of 2017. According to the latest official data, the annual inflation rate has edged higher over the past two quarters but it remains around the bottom of the RBA target range.

If the business expectations are mirrored in the upcoming inflation data, the Australian economy will have to reckon with rising inflation and only moderate economic growth,” Mr Koukoulas noted.

The definitive analysis of the March quarter showed business activity fell 37%, with sales, profit and capital investments down significantly. The Business Actuals Index sunk to 7.6 points, down 4.4 points from the previous quarter, but up 1.5 points on the March quarter of 2016.

The Retail sector, in particular, has fallen on tough times, with its Actuals index entering the red for the first time since Q2 2014. 3

The proportion of retail businesses surveyed which are less optimistic about growing their businesses in 2017 compared to last year has surged to 47.2 percent, compared to just 37.5 percent of businesses interviewed in May. While another 47.2 percent of retail businesses are more optimistic about growth in 2017 compared to the previous year, there is a stark difference to the results of the last 12 months, when retailers were largely more optimistic about growth.

“The retail sector remains weak, in terms of both expectations and actual performance. Weak consumer spending, which is driven by record low wages growth and near record high underemployment, remains one of the major concerns for the economy. Without a solid upswing in retail spending, bottom line GDP growth is unlikely to reach the 3 percent level both Treasury and the RBA are hoping for,” Mr Koukoulas said.

The Business Actuals Index was also dragged down by the Manufacturing sector, which saw its Actual index drop 80.2 percent from the December quarter to 2.6 points, its lowest result since Q3 2015. The Manufacturing industry experienced declines across all indices, in particular its Profits index, which slumped to -1.0 point, indicating that more manufacturers reported losses than profits in the March quarter. However, the sector has reported an improved outlook on employment and selling prices.

This more of a nowcasting than forecasting index but it is what it is. Kouk still has three rate cuts penciled in for 2018 which makes him the most bearish in the country. Yes, even more bearish than MB.

The data is luke warm rather than dire, for profits:

David Llewellyn-Smith is Chief Strategist at the MB Fund and MB Super. David is the founding publisher and editor of MacroBusiness and was the founding publisher and global economy editor of The Diplomat, the Asia Pacific’s leading geo-politics and economics portal.

He is also a former gold trader and economic commentator at The Sydney Morning Herald, The Age, the ABC and Business Spectator. He is the co-author of The Great Crash of 2008 with Ross Garnaut and was the editor of the second Garnaut Climate Change Review.