In our H2 Outlook, we highlighted that a sharper-than-expected Chinese slowdown remains one of the major risks to the global economic outlook. Concerns about China’s near-term economic prospects have increased recently, particularly about deteriorating credit dynamics amid regulatory tightening. In this note, we construct a credit impulse indicator for China using different financing measures. We find that the credit impulse based on total social financing (TSF) adjusted for local debt issuance is more highly correlated with activity than other measures of the Chinese credit impulse. We also find a contemporaneous correlation of China’s credit impulse with domestic activity and a few months lead with global activity.

Not all Chinese credit impulses are equal

The credit impulse is defined as the change in the flow of new credit. The economic rationale behind using the credit impulse relies on the assumption that investment is financed by new borrowing, and therefore an increase in investment (and hence economic growth) is related to the change in the flow of credit.

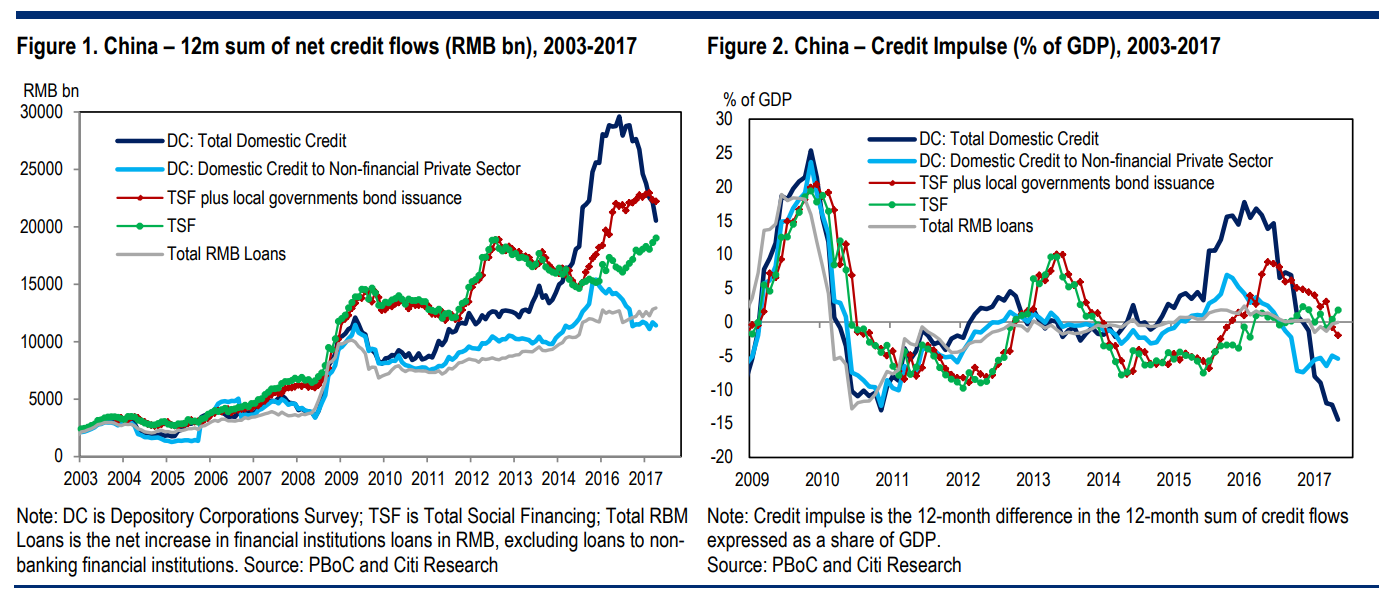

However, one question is which measure of credit to use in China. Our preferred measure is Total Social Financing (TSF) adjusted for local government bond issuance, which includes both bank credit and shadow banking credit to the nonfinancial private sector and local governments and allows for the fact that local governments have switched to more bond issuance over time. Other measures include Total Loans in RMB which tracks credit in local currency by depository and non-depository financial institutions (but not including shadow banking); or Total Domestic Credit from the PBoC’s Depository Corporation survey (DC) which covers credit to the financial and non-financial sectors as well as to the government.

Figure 1 suggests that credit stimulus took place in China in 2009, 2012 and 2015- 16. It also shows that the 12month sum of monthly credit flows captured by TSF was larger than total domestic credit from 2009-2014. In 2015, however, the Domestic Credit measure much exceeded TSF, which suggested a major rise in intra-financial system borrowing and lending, and which as reversed in part since.

The difference between the measures applies in practice and in principle (Figure 2). Our preferred credit impulse measure, the 12M change in the 12M sum of net flows based on TSF adjusted by local governments bond issuance (red line, CI_TSF), turned negative in April for the first time since October 2015 and stands at -2% of GDP as of May. Meanwhile, the credit impulse based on the DC survey data that includes credit to the financial sector (dark blue line, CI_DC) turned negative in November for the first time since October 2014 and is at -14% of GDP as of May.

Credit impulse is highly correlated with Chinese activity

We note that the CI_TSF is more highly correlated with activity data than CI_DC (see Figure 3). The highest contemporaneous correlation (over 2009-May 2017) for CI_TSF was with building sales %YY growth (0.7), fixed asset investment by stateowned enterprises (FAI by SOEs, 0.6) and the manufacturing PMIs (0.5), consistent with the idea that Chinese stimulus in recent years has often been implemented by channeling credit to SOEs. Correlations with GDP, IP, total FAI or (real goods) imports are lower.

Using a cross-correlogram from 2009-2017 (see charts in the Appendix – Credit impulse leading properties), we find that CI_TSF leads the Mfg PMI (by 6 months for NBS and cross-correlation of 0.5). CI_TSF also leads non-manufacturing PMI (14 months, 0.5), total FAI (17 months, 0.4), Industrial production (5 months, 0.4) and imports growth (8 months, 0.5). 2 We note that while CI_DC has a larger lead to these variables, the size of the cross-correlation was smaller than with CI_TSF. For building sales and FAI by SOEs both credit impulse measures correlation is mostly contemporaneous.

Finally, we note that the Granger-causality runs in both directions for the Markit manufacturing PMI, IP and Imports for both credit impulse measures, and building sales for CI_TSF only; while FAI by SOEs granger-causes CI_TSF.

China credit impulse leads global activity

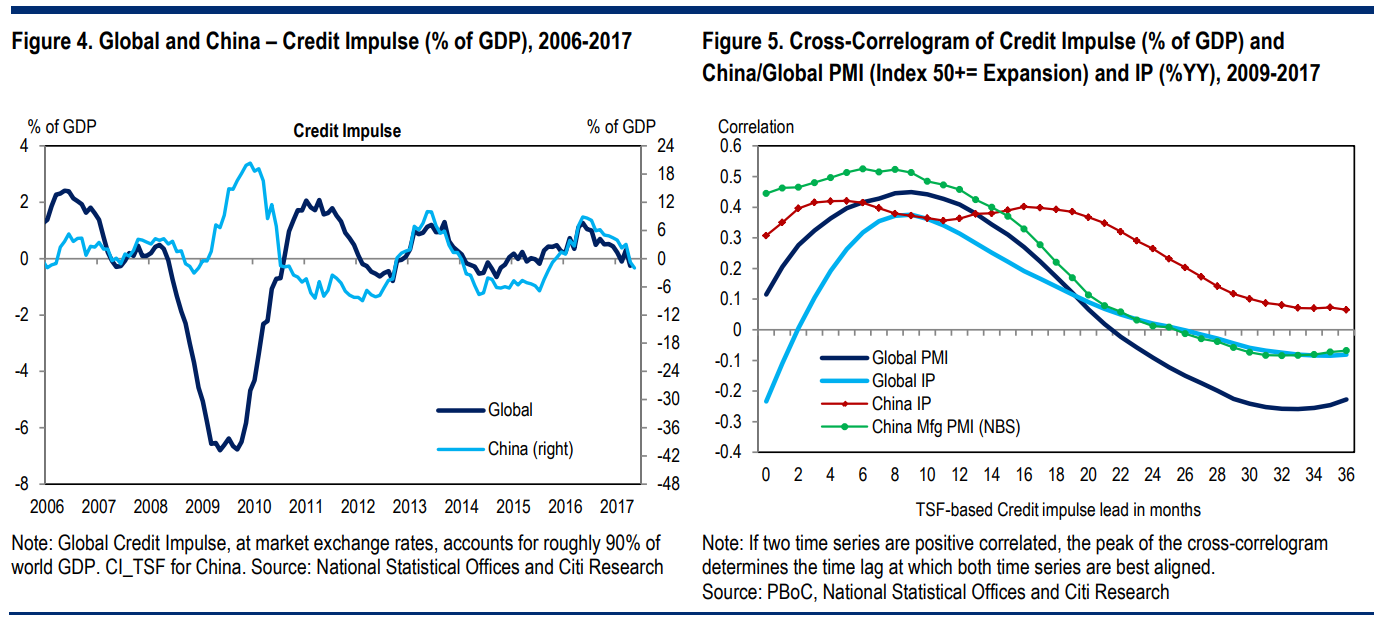

China’s credit impulse has been driving much of the volatility in the global credit impulse (Figure 4), which just turned negative at -0.2% of GDP based on data up to April. Our credit strategy colleagues have argued that the credit impulse has been a major driver of domestic growth & asset prices and has major cross-border effects. While the cross-correlogram between the credit impulse and global GDP growth does not appear to be statistically different from zero, we find that CI_TSF leads global manufacturing PMI by 9 months (cross-correlation of 0.5), global IP growth by 9 months (0.4) and global trade growth by 8 months (0.4, Figure 5).4 It is also worth noting that there are risks that Chinese officials will take more decisive measures to force local governments to deleverage in late 2017 and beyond, including by lowering the amounts of bond issuance allowed. These factors suggest that Chinese credit dynamics could be a drag on Chinese and global activity in the months to come.

However, we stress that the verdict for the global growth outlook is not quite fatal. First, we noted above that the more reliable measure of the Chinese credit impulse is less negative than some alternative measures. Second, we suspect that Chinese policymakers are already veering away from tightening. Third, as economies begin to deleverage – and the Chinese economy may be in the early stages of a corporate deleveraging process – growth and credit become less closely related.

Not fatal for the world, no. But near fatal for Australia…

David Llewellyn-Smith is Chief Strategist at the MB Fund and MB Super. David is the founding publisher and editor of MacroBusiness and was the founding publisher and global economy editor of The Diplomat, the Asia Pacific’s leading geo-politics and economics portal.

He is also a former gold trader and economic commentator at The Sydney Morning Herald, The Age, the ABC and Business Spectator. He is the co-author of The Great Crash of 2008 with Ross Garnaut and was the editor of the second Garnaut Climate Change Review.