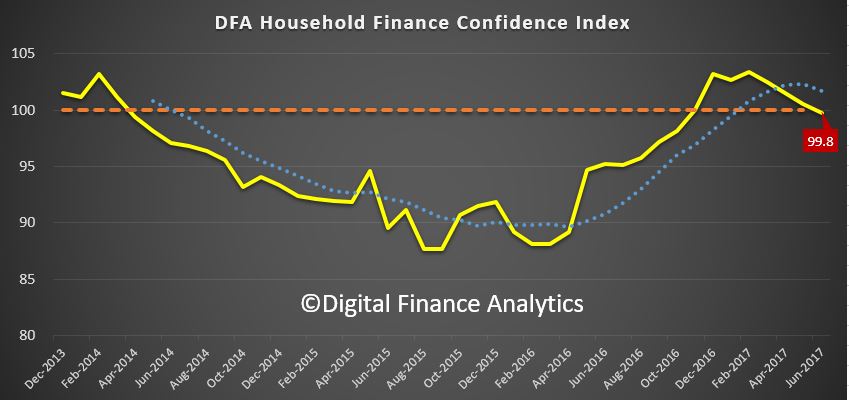

Digital Finance Analytics has today released the Household Finance Confidence index to June 2017, and the news is not good. Overall the index has dropped below the neutral setting and appears to be trending lower. The current reading is 99.8% compared with 100.6 in May.

The fall is being driven by a confluence of issues, none new, but now writ large. Households are seeing the costs of living rising (especially power costs, child care costs and council rates), whilst household income remains depressed and is falling in real terms. Returns on deposits actually fell as well, so mortgage repricing is not being matched by better saving rates. The costs of mortgage repayments rose.

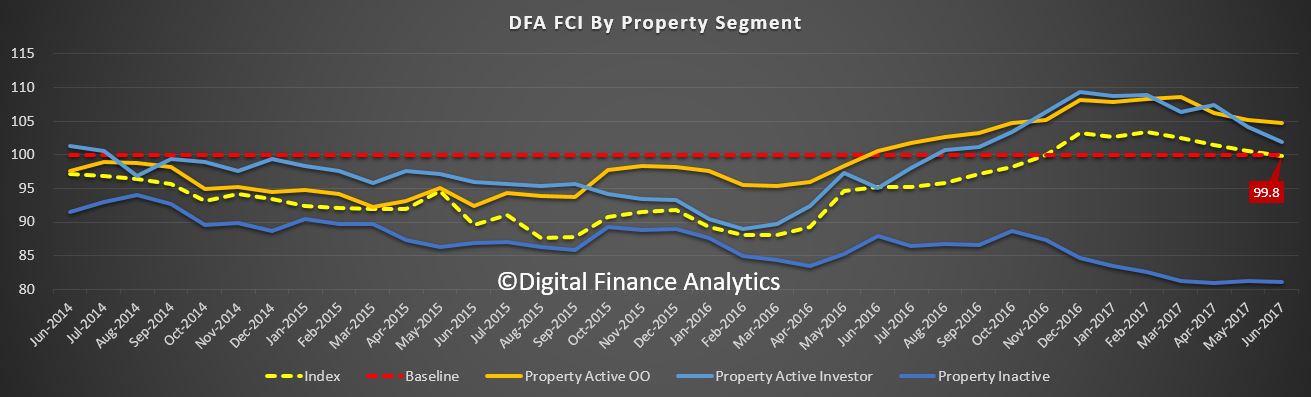

The most significant fall in confidence was in the property investor segment, where loan repricing has been more pronounced, whilst rental incomes are hardly growing. They are also concerned about slowing capital appreciation. However it is still true that property owners have their confidence buttressed relative to property inactive households who are more likely to be renting, and see no rise in their net worth.

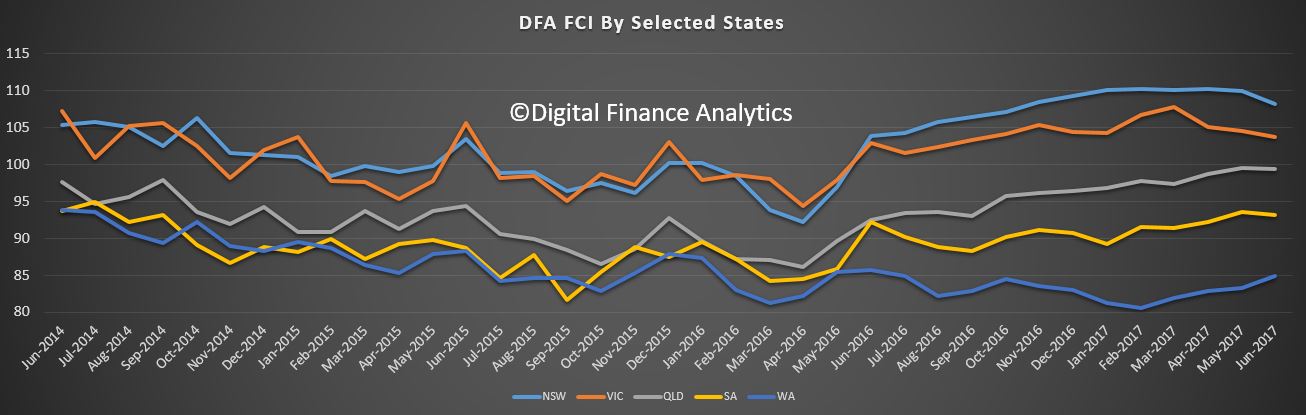

Looking across the states, confidence is still highest in the booming states of NSW and VIC, though down a bit; whilst WA is recovering a little from lows earlier in the year.

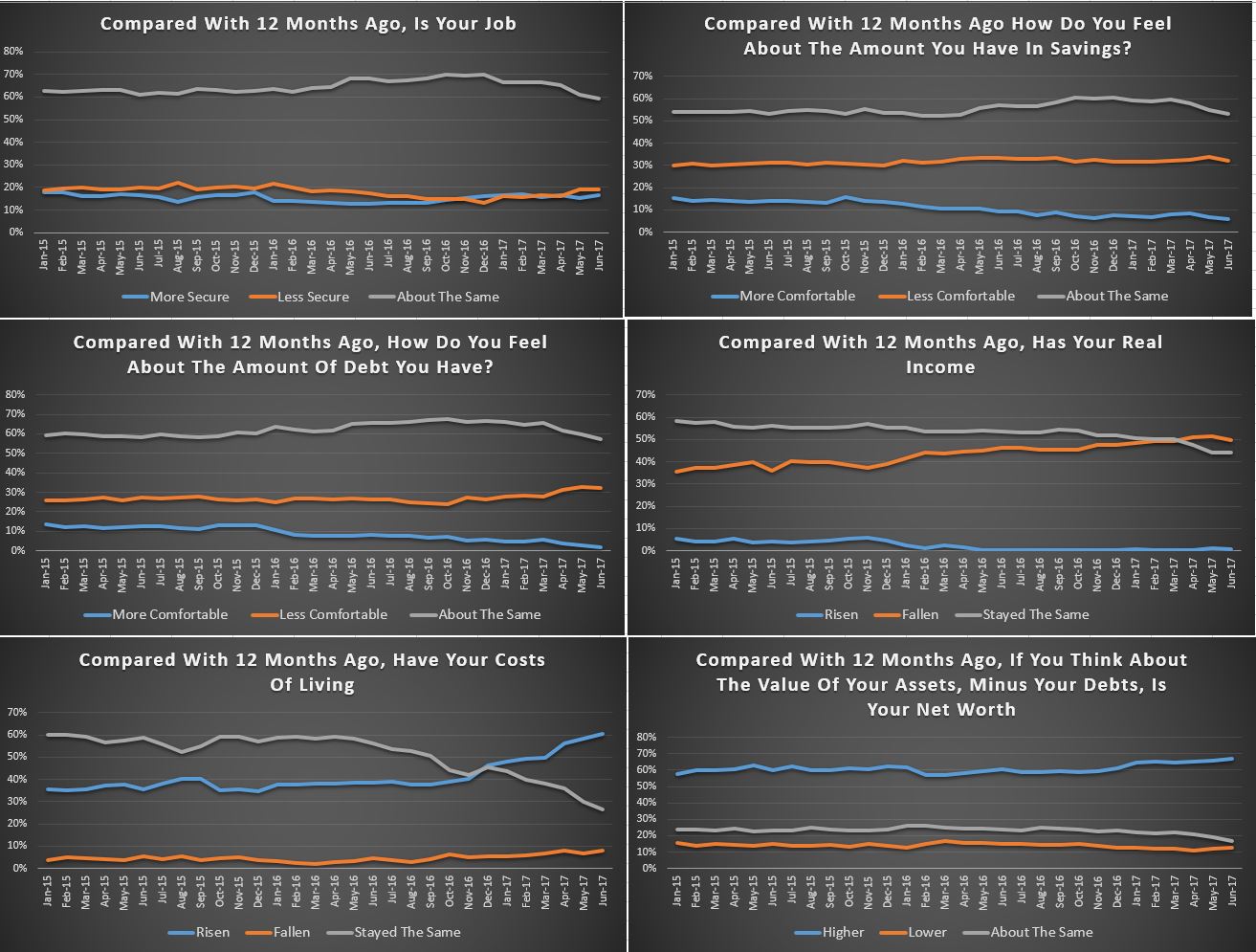

Looking at the scorecard, households are more concerned about the amount of debt they hold, real incomes continue to fall and costs of living continue to rise. This despite job security not being a major concern. Take home pay however is.

We expect to see the index fall further as we move into spring, as more price hikes come though (e.g 20% uplift in electricity for many). The raft of mortgage rate repricing still has to work though and income growth will remain contained. Sentiment in the property sector is clearly a major influence on how households are felling about their finances, but the real dampening force is falling real incomes.

By way of background, these results are derived from our household surveys, averaged across Australia. We have 52,000 households in our sample at any one time. We include detailed questions covering various aspects of a household’s financial footprint. The index measures how households are feeling about their financial health. To calculate the index we ask questions which cover a number of different dimensions. We start by asking households how confident they are feeling about their job security, whether their real income has risen or fallen in the past year, their view on their costs of living over the same period, whether they have increased their loans and other outstanding debts including credit cards and whether they are saving more than last year. Finally we ask about their overall change in net worth over the past 12 months – by net worth we mean net assets less outstanding debts.

{kind=link}