If there is a Hell for bankers, Anna Bligh is going there

Anna Bligh, Fake Premier of the Australian Banking Association, appeared yesterday at the Press Club and, boy, is her soul hurtling towards Hades:

To hold trust in someone or something, one must have reliance on their integrity, their strength and their ability. For the major institutions that have been the foundation of western democracies, this reliance is eroding and public trust is in increasingly short supply.

In my first public comments on this subject at a banking conference in April, I placed a consideration of the decline of trust in Australian banks in a broader global context and I want to start there again today.

The Edelman Global Trust Barometer measures public trust in government, business, media and the non-government sector. It has done so in 28 countries for 17 years and has chartered a steady decline in the barometer since the new century began. But this decline has begun to accelerate markedly in recent years.

In 2017, the Barometer recorded the largest ever drop in trust across business, government and media.

Globally:

Trust in business fell from 53% to 52%.

Trust in media fell from 48% to 43% (at an all-time low in 17 countries).

Trust levels in government fell from 42% to 41% (this dropped in 14 markets and is the least trusted institution in half of the 28 countries surveyed).

In Australia:

Trust in business declined from 52% to 48% – a 4% drop.

Trust in media declined from 42% to 32% (all time low).

Trust in government declined from 45% to 37% – lower than the global average.

In two thirds of the countries surveyed, less than 50% of people trust the mainstream institutions measured.

The trust gap is not uniform. It is widening between what Edelman calls the “informed public” (those with high incomes, a university education and high engagement with the news) and what it calls the “mass public”, that is those who do not share these characteristics.

Against this backdrop, it is little wonder that Australian banks are experiencing a problem in community and consumer trust.

Banks, after all, are large, prominent examples of corporate Australia. When people think “big business”, banks come quickly to mind. Banks are successful, profitable and have a huge customer base that they interact with every day.

Banks touch everyone and everyone has an experience and an opinion.

In some respects, banking is no different to politics or media; trust is essential. But, distinct from Government or media, banking is intensely personal.

Banks deal with people’s money, their savings, their livelihoods, their homes and businesses, their prospects, their dreams for the future and their retirement.

An individual’s financial well-being and the well-being of their families is about as personal as it gets.

As a result, banks are rightly held to higher standards and expectations than those that apply elsewhere. That’s fair enough. Australians respect, and rightly expect fairness.

Edelman has called the 2017 results an “implosion of trust”.

With an implosion of trust comes an explosion of scrutiny and nothing could be more true in Australia’s banks.

Australian banks have been the subject of some 37 reviews, inquiries and investigations since the GFC – 17 of them in the last 18 months, with more to come. Some of the most significant inquiries – which I will touch on, have been initiated by the banks.

Such is the venomous attention that banks now attract in the public arena that unregulated, unsupervised non-bank lenders, and other pay day lenders, have flourished with almost no scrutiny or public acrimony.

With an implosion of trust comes an inexorable move to populism in politics.

As more and more people form the view that mainstream institutions have failed to protect them from the impacts of globalisation and technological change, the more distrustful they have become. The more they have sought the comfort and simplicity of populist ideas and movements.

In this context, let’s talk about banks.

Banks

The general view of banks as the ultimate signifier of big business – and the erosion of trust that this has brought with it – has been compounded by a number of factors.

Firstly, the global financial crisis. Yes, Australian banks survived this crisis, no Australian banks failed and none needed taxpayer bailouts.

As noted in a recent Monthly essay, historically, periods of populism haven’t occurred at random.

Populism flares up predictably during vacuums, those tumultuous gaps after an old regime has collapsed and before the new order is born. The interwar turmoil of the Depression spawned the nationalism, racism and extremism of the European populists, including Germany’s National Socialists.

A University of Munich study examined the political fallout from economic crises over the past 140 years across more than 800 general elections in 20 countries.

It found that populism surges after systemic financial crises.

While our banks survived the GFC financially, what they have not avoided is the global reputational fallout from that crisis and the populist banking politics it brought with it.

As other countries held post GFC inquiries, the revelations of corrupt behaviour and unacceptable corporate culture in some banks found their way into our collective view of all banks.

The Occupy Wall Street movement started in Wall Street for a reason.

The financial system in general, and banks specifically, became the rallying point for a cry for a more equal distribution of wealth and opportunity.

The ripple effect of that cry is still being felt and heard.

Here in Australia, this has been compounded by a number of serious instances of poor bank culture and poor customer outcomes that have hit the headlines and resonated with a sceptical public, regardless of their own personal experience with their own bank.

Banks do not resile from the need to improve both their culture and conduct. Indeed, they have embarked on an industry led program of reform and have cooperated with the changes imposed by Government and regulators.

Yes, there is more to do and, in my view, more to do at a faster pace than banks are used to, but the leadership of our banks are intensely focused on the challenge.

Real change in big institutions always starts at the top and just over 100 days in, I believe that the leadership of our major banks are up for the task.

In my first hundred days I have been encouraged that the industry is serious about delivering change.

I am utterly convinced that the industry’s reform agenda today is as ambitious as at any time in its history. There’s a lot of work to do but if the implementation is as good as the intent, then I think great things can be achieved.

And that will be good for customers and the community, so let me turn to people.

People

We are living through the single biggest transfer of power from institutions into the hands of consumers and constituents in human history. The digital world has empowered consumers to quickly and easily contact others with similar experiences and views and to turn a complaint into a movement in the matter of hours.

So what does ABA research tell us about what these newly empowered Australians are thinking about banks?

Some interesting insights:

Firstly, customers have a relatively positive view of their own banks and report stronger levels of trust with their own personal banking experience.

When it comes to trust, 53% of those surveyed reported they trust their own bank, while only 31% trust the banking industry.

Those who do report trusting the industry say they do so because they believe in its stability, regulations and reliability.

Those who don’t, say it’s because they believe it is profit-driven and self-serving.

Further, at this stage, people have relatively low awareness of the reforms that are sweeping across the banking industry. But when they are taken through the reforms, step by step, they have a very positive view of any initiatives designed to improve standards and integrity, such as the new Code of Banking Practice.

Perhaps unsurprisingly, bank customers think that bank shareholders are someone else, someone other than themselves.

At a rational level, many people think the banks make big profits and keep them locked away for the benefit of a small band of faceless bigwigs.

At an emotional level, many people obviously don’t think of themselves as among this band of bigwigs, they think of themselves as outsiders, somehow excluded from the profits banks generate.

In a recent survey, respondents were asked what proportion of bank profits they think are returned to shareholders. 41% said less than 10% and further 31% said less than 25%. So almost 3 in 4 people believe that banks return less than a quarter of their profits to their shareholders.

The fact is that 80% of bank profits are returned to shareholders.

And 75% of these shareholders are Australian. They are the millions of Australians who own bank shares directly in their own name, and any Australian with a superannuation account – almost 12 million people – who own bank shares indirectly through their super fund.

This view of profits, and where they go, shows a yawning gap between perception and reality and helps to explain the declining level of trust.

It also points to both the communication challenge faced by Australian banks and to an opportunity for them to unlock a change in perceptions by helping Australians understand they are the beneficiaries of the success, and profitability, of banks.

This research is being conducted as part of a benchmarking exercise against which the ABA and the banking industry can measure progress on the project to rebuild trust with customers and the broader community.

It represents my determination and that of the industry to make real change and to hold ourselves accountable for that change.

When finalised, the benchmarks will be made public.

So, let me turn to the politics of banking. The politics of banking is now more real than the reality of banking and has put banks at the top of the charts.

Politics

On the 16th August, it will be 70 years since Ben Chifley announced his intention to nationalise Australia’s commercial banks. Not since that debate have banks so occupied the political class.

From calls for a royal commission on one side to an ever-increasing raft of intervention and regulation of banks on the other, parties, major and minor, are now climbing over each other to be, and to be seen to be, tough on banks.

In this context, there is an ever diminishing appetite for thoughtful and sensible public policy making. Any appetite there may once have been to explain the complexity and importance of banking to the Australian economy has been all but extinguished.

It is now permissible in public life to say anything about and do anything to banks – this puts our banking system into an ever-more precarious position.

The public arena is littered with recent examples of an escalating public debate.

The Federal Treasurer told us recently that Australian banks determine interest rates using a “voodoo black box” and that the new Banking Executive Accountability Regime would “crack down on high flying executives who take drugs.”

The Leader of the Opposition tells us that “there are tens of thousands of Australians on an annual basis being ripped off.”

And the Federal Member for Leichardt told us that “They (banks) could literally shoot you – take you out to the back of the shed and literally shoot you and they could argue successfully that it’s within their terms of agreement.”

This rhetoric is dangerous for Australia’s financial stability.

In this political landscape, it is not surprising that persistent myths and criticisms about banks flourish.

Let me deal with some of the myths and criticisms.

The first is that banks aren’t paying their way, banks don’t pay their fair share of tax, banks should do their bit to fix the Federal Budget, and in the case of South Australia, pay GST and fix their budget too. The fact is that Australia’s banks are Australia’s largest tax payers – the industry paid more than $14 billion in tax last year alone.

Five of Australia’s six largest taxpayers are banks. As the largest companies in the country that’s as it should be.

But what is not widely understood is that Australia’s banks pay more tax than the rest of the ASX200 combined. That’s right, banks pay 55% of the tax paid by the country’s 200 largest listed enterprises.

And, Australia’s banks pay tax at the full corporate rate of 30%.

Many companies don’t.

Australia’s banks are not just our largest taxpayers, they belong to an industry which is the biggest contributor to Australia’s GDP.

Another criticism is that banks are too profitable.

The average return on equity of Australia’s big banks is around 14%. That puts banks in the middle not at the top of the pack, when compared with Australia’s 50 largest companies.

There are plenty of Australian, and certainly foreign companies, making big profits in Australia, making higher returns on equity than the big banks, that aren’t paying anything like the same rate of tax as banks. In some cases, they pay next to no tax at all.

A related perception is that banks not only make a lot of money, they somehow, mysteriously, keep it to themselves or share the spoils with an elite few.

Looking at the main retail banks in the past financial year:

$25 billion was paid in wages and salaries

As I mentioned earlier, banks pay more tax than anyone, else, last year it was more than $14 billion

And then there were dividends of $26 billion – largely returned to Australians The banks retained 20% to reinvest in their businesses – into new ways of banking that create a better experience for customers

That reinvestment gives us things like mobile and online banking, things customers really value.

In total, banks distributed more than $65 billion to people across our economy, including you and me. It is a massive contribution to the federal budget, the national economy and the financial wellbeing of every Australian.

Challenge for Banks

Against this economic and political backdrop, the challenge for Australia’s banks is to make the changes necessary and communicate them well.

To change culture, adapt practice and be ready for the future. To work harder to turn Us and Them into You and Me.

So, what’s happening on this front?

Short answer is more than most people realise.

If you work in a bank, every nook and cranny of your job is being scrutinised and overhauled. Banks are literally living change and doing so at an unprecedented rate.

Let me talk in a little more detail about just some of the important shifts.

Decoupling Remuneration Incentives from Sales Targets

The banking industry commissioned Stephen Sedgwick, the former head of the Commonwealth Public Service, to review sales and commissions. His report provides a blueprint for a new remuneration system in our banks. One that rewards good customer service and shifts dramatically away from incentives that encourage the up-selling or cross-selling of products.

All banks have signed up to implement this blueprint, lock, stock and barrel, over the next 18 months. It will require large-scale cultural change deep inside every part of each bank’s operations.

It represents a significant move away from a sales driven culture and it is happening right now.

Customer Advocates

Last year all retail banks committed to introduce a new senior position – a Customer Advocate. Today, these 22 banks have appointed these Advocates and they are beginning to have a significant impact.

Customer advocates and the teams they lead are charged with making things easier for customers helping them navigate the system if they have a complaint.

But more importantly, they are charged with the responsibility to work across the bank to proactively improve customer experience and put customers at the centre of decision-making.

This means they are sitting in with product design teams as new financial products are developed.

They are working with data analytics teams to develop red flags that indicate a vulnerable customer is in financial distress so that hardship teams can make contact before that customer is in real financial strife.

A New Code of Practice

Again, the industry itself commissioned a review of the Code of Banking Practice. As a result, the Code is now being completely overhauled.

The new code is on track for completion by the end of this year. The Code will require ASIC approval. It will be enforceable and will clearly spell out high standards of conduct.

Add to these initiatives, the plethora of other industry and Government reforms including:

Stronger whistle blower protections

The introduction of real time banking and open data

A new executive accountability regime

A new one stop shop for customer complaints, and

New product intervention powers to the regulator.

And you can see profound change is afoot and that it’s all heading in the right direction.

As I said earlier, 20% of bank profits are ploughed back into better banking services.

In 2017, this reinvestment is critical.

These funds are driving innovation and better services for customers, services that are adaptable, mobile and convenient. And importantly, services that will enable banks to compete in a rapidly changing environment.

Let’s think about that future for a moment.

Like so many other industries, banking is facing rapid and seismic forces of technological change that will mean that in just a few years, banking could look very different than it does today.

Online banking, electronic payments and paywave have already changed our relationship with our bank. They have driven a revolution in ease and convenience and there is more to come.

Automation and robotics are already improving banks’ systems and processes and enhancing risk management. Robotics can accurately and systematically identify when a customer has made a mistake on a loan application form. The bank can then use that insight to enhance customer protection and meet their obligations under responsible lending laws.

One of the more immediate developments is called “open data”. Put simply, open data looks at how customers can use all the data that is being collected about them or their business to get the most appropriate and lowest cost deal for them, or use this dataset to make their life easier.

One very tangible case of the benefits of open data we can see today is SMEs asking their banks to directly share their data with accounting software like Xero and MYOB. This greatly improves the life of small business people by reducing the time they spend on paperwork and the money they spend on their accountant.

Open data will mean customers can use the rich picture their financial transactions reveal to ensure they get the right mortgage or the right credit card that gives them what they need when they want it.

It will also facilitate fast and easy switching between banks as customers can simply access all their recurring automatic payments and take them with them. All good stuff, but not hard to see the importance of getting it right to avoid serious security and privacy problems.

But open data is just the beginning. Think about the implications of:

A cashless society

The advent of cyber currency

An increase in peer to peer lending, and

The rise and influence of new, non-bank players such as Apple Pay and Alipay.

All of these are disruptive. All can have both positive and negative outcomes for customers. All can play havoc with our strong and stable banking system.

In times of major disruption, trust becomes an even more critical ingredient. As Australians and their banks navigate these radical changes, trust will be imperative to getting the mix right.

It’s an intriguing challenge. It’s a challenge I relish.

Imagine if Australia was able to lead the way in turning around a global trend and delivering something that both surprised and delighted bank customers, the broader public and their political masters?

Make no mistake, like the journalists in this room, Australia’s banks understand that their world has changed forever, that they are living in a new normal and that more, better and different is being demanded of them. They are rising to that challenge in meaningful ways that customers can see, feel and touch.

In five years’ time, what I want to see is Australia’s banking sector leading the world, not just because it is strong, stable, safe and well regulated – because a case can be made that we already lead the world on these measures – but because banks are ready for the future and customers have high levels of trust and confidence in banks to appropriately balance their interests with those of bank shareholders. Where it is self-evident that these things are indivisible.

That is one long breath of complete sophistry. The entire argument is based on the single fallacious premise that two wrongs make right:

- global trust has collapsed so it’s not so bad for banks;

- global banks were evil for being bailed out, so ours are not so bad;

- banks pay lot’s of tax even while other’s do not;

- banks returns on equity are less greedy than some others;

- populism is wrong so banks should walk free.

An outpouring of pure moral relativism designed to do just one thing: protect banking rents.

Let’s get a few facts straight:

- Australian banks were truly, madly and deeply bailed out during the GFC via virtually free wholesale guarantees, actually free deposit guarantees, massive fiscal stimulus especially for houses, public purchase of RMBS, cash for coconuts at the RBA, and I could go on, and on, and on…

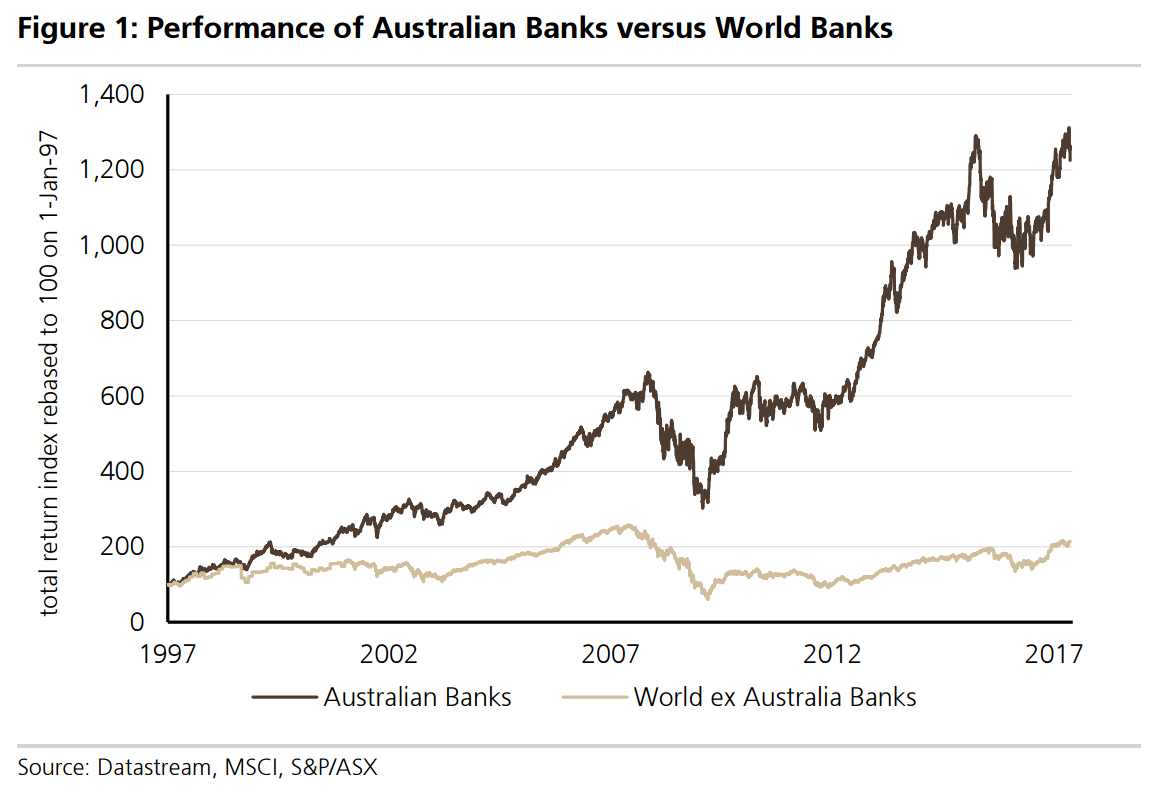

- Thanks to these epic subsidies, Australian banks have enjoyed magnificent returns, especially post-GFC. Far, far above global benchmarks:

- Banks may pay a lot of tax because of huge profits. But they do not pay for the free public support services dished out during the GFC bailout. The RBA calculates these subsidies at 18bps of liabilities but in truth they are much higher.

- Populism by definition is not ‘popular policy’. Populism is the rise of oligarchs that stick their faces into the public trough while pretending to be interested in it. Populism is the pretense of being ‘of the people’ so that the public mistake selfish behaviour as being ‘for the people’.

Anna Bligh is the Fake Premier of Australia’s fake banking government, with its fake bureaucrats, fake reform, fake policy objectives and fake public policy ethos. Just about the only thing that is real is the undoubtedly enormous pay packet that she draws even as she doubles-down on a fat public pension.

She is the living, breathing, walking, speaking and profiteering embodiment of Australia’s need for a banking royal commission.