Very little clarity today still on the embarrassing Domainfax debacle. UBS fingers just that:

Post the conference call, we still do not have a definitive reason as to why TPG walked away. FXJ’s interpretation was TPG did not want to bid for 100% of the company. With respect to H&F: they notified FXJ that were not able to form a bid by last Friday’s deadline, and FXJ have terminated discussions with H&F. To re-iterate, we think the keys to hitting PE return hurdles (UBSe c15-20% equity IRR) are: i) aggressive gearing in an unlisted environment, and ii) organic earnings growth (e.g. c$115m Domain EBITDA today potentially lifting to c$200m in the medium term). It remains unclear whether TPG found reasons to doubt the latter in the due diligence process.

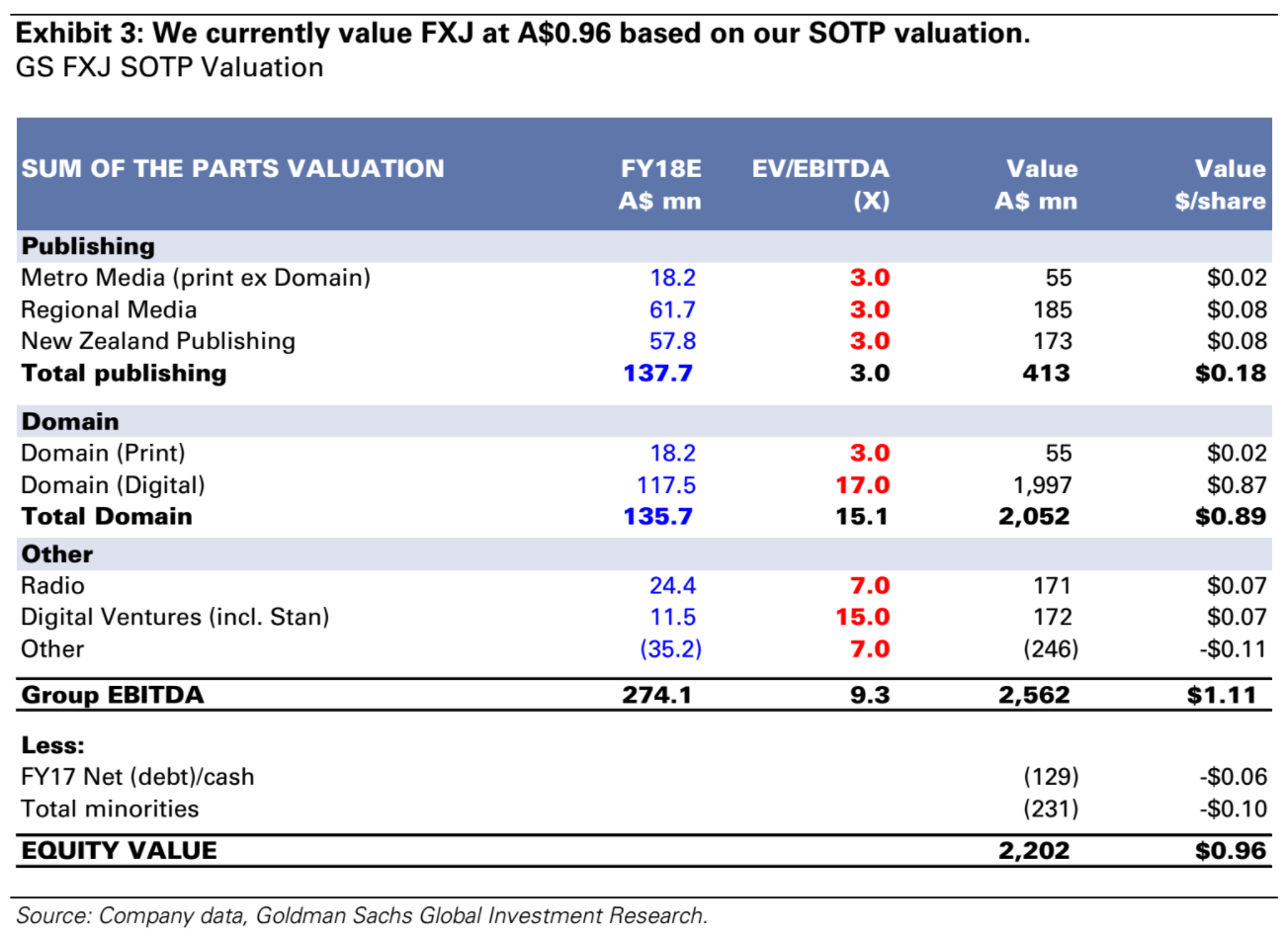

Goldman shows what that looks like in a spread sheet:

Papers worth two cents. Ouch.

Citi touches on the problem:

Domain was the prize, the newspapers are the problem — After six weeks of due diligence, TPG has officially informed FXJ that it will not proceed with a binding bid. Hellman & Friedman have not completely terminated the process but were unable to make a bid by FXJ’s deadline. While no specific reasons were given, FXJ management’s interpretation was that TPG did not want to proceed with buying the entire company. In our view, it is the rapidly declining earnings profile and the potential restructuring and redundancy charges needed to keep media (newspaper) EBITDA in positive territory, which are likely to be the key issue.

Print revenue trends are likely to get worse from here — We have upgraded our revenue growth forecasts for Domain, and downgraded media revenue estimates in line with FXJ’s trading update. Management are guiding for FY17 EBITDA of $262- 266m. We expect media revenue trends to continue to deteriorate, and while group revenue declines are large, this is partly offset by Domain growth and higher margins. We have cut FY18-19E EPS by -3%.

FXJ will need to work hard to keep Metro Media positive — We forecast EBITDA of $31m for Metro Media in FY17, off revenue of $517m. Cost savings of $30m for FY18 should keep the division in positive territory next year despite double digit revenue declines. However, after restructuring charges ($15m this year), net cash flow is negligible, and FXJ will need to repeat those same cost savings every year and, in our view, FXJ is unlikely to stabilize revenue in the next few years. We also see ACM and NZ Media following a similar trajectory although both are a few years behind Metro Media.

As the paper’s fall and Domain rises, the necessity to cut costs in the former and raise revenue in the latter shreds editorial quality as journos are substituted with mindless property spruikbots.

In short, private equity read The Pascometer’s realty porn and sagely concluded that $2.5bn could be better spent elsewhere…