You know my view but try Deutsche’s excellent Adam Boynton:

A funding challenge?

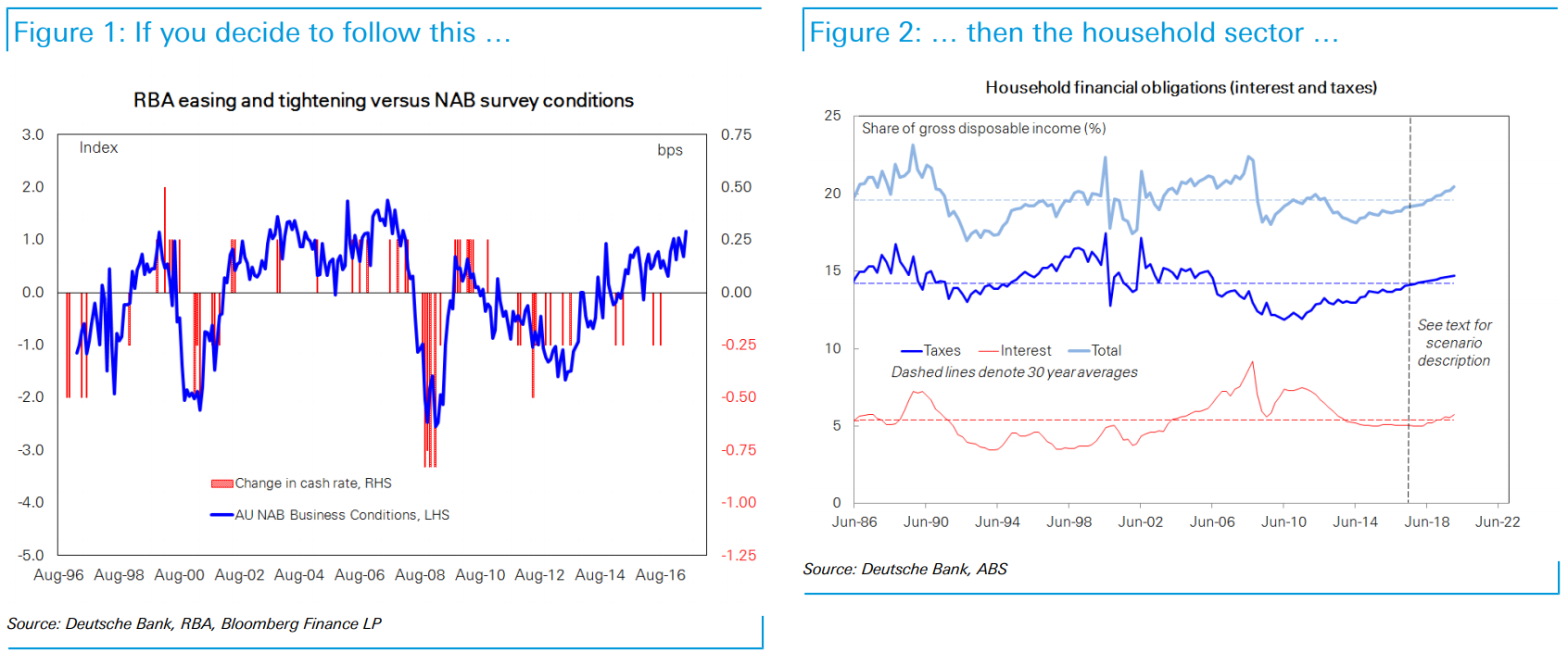

AUD/USD has recently broken out of the top of the range it has traded in for over a year. Despite that, and despite the recent RBA repricing in Australia, the 10-year spread to the US remains below the highs of ~55bp seen in October last year. Surely an appreciating currency and a relatively narrow spread to the US can’t be sustained? After all, who’s going to buy Australia’s issuance with both those prices (namely a high AUD and a narrow spread )? At the same time the most recent batch of Chinese data have come in on the robust side. That should help the recovery seen in iron ore over the past few months and should also keep Australian business conditions at their current high levels. Indeed business conditions are at levels that in the past have been consistent with RBA rate hikes (Figure 1). One could presumably solve the problem in paragraph one with the ‘solution’ presented in paragraph two: RBA rate hikes.

The full text of this article is available to MacroBusiness subscribers

David Llewellyn-Smith is Chief Strategist at the MB Fund and MB Super. David is the founding publisher and editor of MacroBusiness and was the founding publisher and global economy editor of The Diplomat, the Asia Pacific’s leading geo-politics and economics portal.

He is also a former gold trader and economic commentator at The Sydney Morning Herald, The Age, the ABC and Business Spectator. He is the co-author of The Great Crash of 2008 with Ross Garnaut and was the editor of the second Garnaut Climate Change Review.